Shares of Lucid Group (NASDAQ:LCID) went on an almighty tear last Friday, after rumors began circulating that Saudi Arabia’s Public Investment Fund (PIF) is getting ready to buy the remaining LCID shares it does not already own (roughly 30%).

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investors obviously liked the idea, but does it alter the game for Morgan Stanley’s Adam Jonas? No, is the short answer, although Jonas elaborates over several reasons why he remains a fully-fledged bear.

For one, on the aspect of fundamentals, rather than getting better, Jonas thinks the fundamental outlook is “more likely deteriorating than improving.” Into 3Q, Lucid showed a drop in net reservations and Q4 deliveries reached 1,932 units against production of 3,493 units. “In the wake of Tesla’s price cuts,” says Jonas, “we would be prepared for potentially further declines in reservations, assuming they are still reported.” While Jonas thinks production snags will likely only improve, considering the backdrop of rising rates and a slowing economy, he worries about the demand for ultra-premium priced cars.

Then there is the issue surrounding dilution. Jonas expects the company to turn free cash flow breakeven in FY26. To have the levels of liquidity needed to keep the business running, Jonas thinks another $500 million of equity issuance is in the cards this year and assumes an additional capital infusion of $3 billion will be required in FY24 (split 50/50 debt and equity). “Taken together with SBC impact,” Jonas explains, “we have forecasted a further 25% increase in LCID diluted shares outstanding through FY26.”

Another element to consider revolves around strategy. In the near future, Lucid’s game plan involves pivoting to international markets (Europe, China, Middle East), but what happens should the macro backdrop further deteriorate? Changing circumstances might call for “more austere or slower execution” of numerous strategic targets regarding further expansion.

And this is where the presence of EV giant Tesla makes itself felt. “Specifically,” Jonas sums up, “we are concerned that forthcoming manufacturing innovation at rival Tesla could drive a step-change in EV deflation that could be a detriment to competitors such as Lucid.”

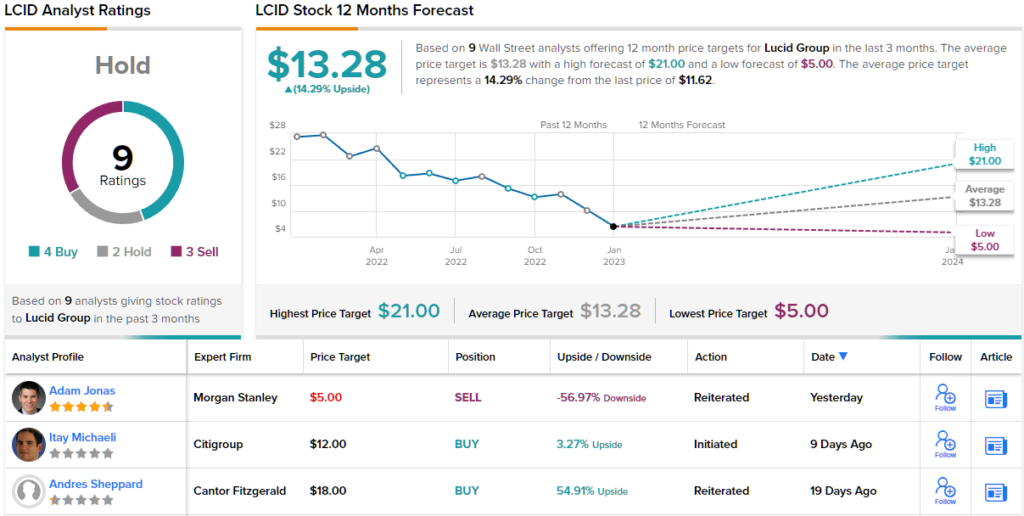

What all this talk boils down to as far as Jonas is concerned is “Really nice car, large cap valuation, niche market, continued cash needs.” The result of that assessment is an Underweight (i.e., Sell) rating, backed by a $5 price target. The implication for investors? Downside of a depressing 57% from current levels, at least according to Morgan Stanley. (To watch Jonas’ track record, click here)

Jonas remains the Street’s biggest LCID bear; elsewhere, the stock claims an additional 4 Buys, 2 Holds, and 3 Sells, for a Hold consensus rating. The average target stands at $13.28, suggesting investors are in for gains of 14% over the coming months. (See Lucid stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.