The savvy investor knows that the best time to buy is when a stock is priced low – it’s just the old game of ‘buy low and sell high,’ the age-old advice on how to make money. But markets have been rising lately, even taking some recent fluctuations into account. But with the S&P and the NASDAQ near record levels, it’s hard to tell when a stock is priced low.

The key is just to take them as individuals. The stock market is the world’s greatest real-time experiment in averaging over large mass numbers. The market as a whole can go up, while a few individual stocks are slipping to the bottom. And when a stock hits bottom, as long its basics are sound, it becomes a buying opportunity.

Wall Street’s analysts make their reputations by finding these opportunities, and bringing them to our attention. Prices fall for reasons, but not all of those reasons bode ill for the stock. We used the TipRanks database and pulled up the analyst commentary on three low-priced stocks that have attracted attention for the right reasons.

QuinStreet (QNST)

We’ll start in digital marketing, where QuinStreet, founded in 1999, was a pioneer in performance marketing. The company leverages technology and the direct measurability of digital media to create better marketing and branding solutions for its customers. QuinStreet works with customers in the insurance, personal loan, credit card, banking , and home services industries.

QuinStreet wrapped up its fiscal year 2021 on June 30, and a look at the numbers will show the company’s position ahead of its November 3 release of fiscal 1Q22 numbers. The company reported $151 million in quarterly revenue for 4Q21, up 29% from the $117 million reported in the year-ago quarter. The full-year revenue of $578.5 million was up 17% from FY20’s $490.3 million top line. EPS also grew year-over-year, from 14 cents to 17 cents. On the negative side, the EPS was down from Q3’s 20 cent print. And looking ahead, the company’s Q1 EPS is expected at 16 cents.

While the company’s revenues have shown steady growth, the earnings have not – and that has been the key point for investors recently. The stock is down 31% year-to-date, and down 40% from its February peak value.

5-star analyst John Campbell, of Stephens, takes an upbeat look at QuinStreet, based on the whole picture, writing: “We continue to believe that QNST sits in an attractive buying window given the valuation (~12x forward EBITDA vs. peers ~25x and its past TTM avg. of ~13x), given low expectations/ongoing fears of a pullback in client spend from frothy marketing appetites last year and given our belief that the deck is set for outperformance with the Company just recently posting, what we feel as conservative, new fiscal year guidance. In addition, we continue to like the added optionality tied to QNST’s QRP offering and ongoing takeout optionality.”

In line with his bullish comments, Campbell rates QNST an Overweight (i.e. Buy), and his $26 target price implies an upside of 76% in the next 12 months. (To watch Campbell’s track record, click here)

It’s clear that Wall Street is in general agreement with Campbell’s assessment here, as the stock has a unanimous Strong Buy consensus rating based on 3 positive reviews. The shares are priced at $14.80 and their $25.50 average target suggests a 73% one-year upside. (See QNST stock analysis on TipRanks)

Chegg (CHGG)

Next up is Chegg, an education technology company that saw strong gains in share price in 2020, during the corona pandemic. The company specializes in online study aides and textbook rentals, offering students access to texts, flash cards, study guides, writing guides, and even online tutors. These services are essential for home schooling – or for regular schooling via remote – and Chegg has been able to expand as the needs for its services grew more urgent.

As schools reopened in 2021, Chegg saw its share price decline, and the stock is now down 35% so far this year. However, even as the stock price has fallen, revenues have grown. The company reported $198.48 million for 2Q21, flat from Q1 but up 30% yoy. The company’s earnings beat the estimates, with EPS coming in at 43 cents, up from 37 cents in the year-ago quarter. It addition to sound revenues and earnings, Chegg reported $2.5 billion in liquid assets as of the end of Q2.

The company reported Q3 earnings on November 1, and is predicting revenue between $170 and million and $175 million. The falloff from the Q2 number is to be expected, as Chegg typically reports its best top-line numbers in Q2 and Q4. At the predicted range, the revenue will achieve 12% yoy growth.

Covering Chegg for Barrington, 5-star analyst Alexander Paris believes the stock is currently undervalued, and he explains: “Chegg’s shares, which are down 48% from their 52-week high primarily on growth concerns (tough COVID comps), are currently trading at 10.1x and 8.3x our 2021 and 2022 revenue estimates, respectively, a premium to its Ed Tech peers… We feel a premium valuation is justified, however, given Chegg’s sustainable, superior revenue growth rate and high and rising profitability, combined with a balance sheet including nearly $2.6 billion in cash to finance further growth initiatives including strategic acquisitions.”

In line with his optimistic approach, Paris gives CHGG shares a Buy rating and his $100 price target suggests ~67% potential upside for the coming year. (To watch Paris’s track record, click here)

With 9 recent reviews on file, including 8 Buys and just a single Hold, it’s clear that a majority of the analysts are behind the Strong Buy consensus rating. The stock has an average price target of $102, slightly more bullish than Paris’s, and implying a 70% upside potential from the $59.88 current trading price. (See CHGG stock analysis on TipRanks)

Tactile Systems Technology (TCMD)

We’ll wrap up our list today with Tactile Systems Technology, a medical tech company that focuses on creating new medical devices for the treatment of chronic disease. Specifically, the company is developing pneumatic pressure systems and clothing for the treatment of lymphedema, or chronic swelling. This is a dangerous condition with a potential patient base of 20 million in the US alone.

Tactile offers a range of products to treat swelling in various parts of the body, including the legs, arms, torso, and head and neck. The company’s Flexitouch system has been shown effective in 88% of patients who have used it, and has an impressive 96% patient satisfaction rate. Use of the pressure system has led 85% of patients to report improvement in quality of life. From the perspective of health plans, the technology can reduce treatment costs by 37%.

In September of this year, Tactile Systems announced that it had acquired AffloVest, a wearable respiratory therapy device used to treat patients with chronic breathing problems through management of airway clearance. The wearable pressure technology was a sound match for Tactile Systems, which borrowed $55 million of the $80 million up-front cost of the transaction. Tactile Systems expects the AffloVest product to generate up to $17 million in annual revenues.

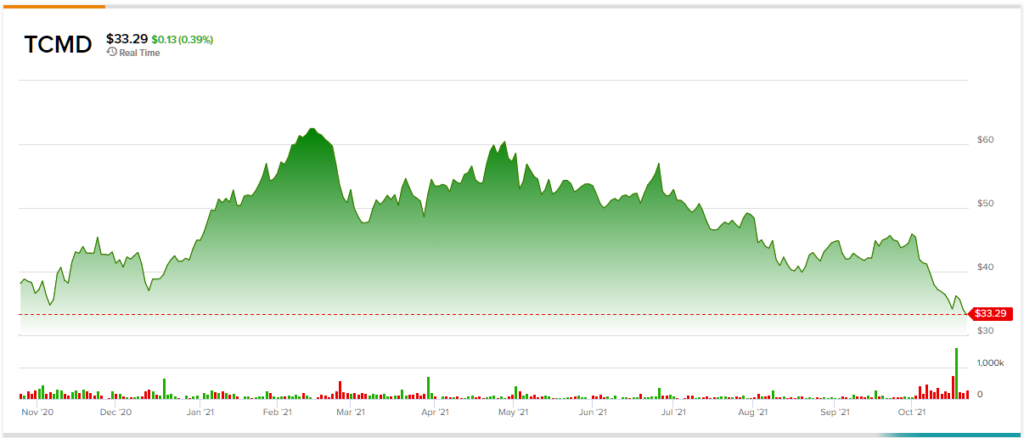

Despite these clear strengths, Tactile Systems’ stock price has fallen 26% so far this year, and is currently trading near their 52-week lows.

In his review of TCMD shares for Piper Sandler, Adam Maeder, rated 5-stars by TipRanks, describes Tactile Systems as his one of his ‘favorite SMID-Cap ideas.’ He provided several points why, including, “[An] attractive combination of above-average top-line medtech growth, solid gross margin profile, profitable business [and that] Lymphedema and Bronchiectasis are under-appreciated end-markets and we see TCMD as well-positioned in both.”

“We see the set-up over the next 12-24 months as quite favorable as the lymphedema business gains additional momentum coming out of the depths of the pandemic, the Qui Tam lawsuit reaches resolution, AffloVest provides incremental growth, and valuation levels remains quite attractive,” the analyst added.

Maeder’s upbeat outlook leads him to put a Buy rating on the stock, and his price target, of $70, implies a robust one-year upside potential of 110%. (To watch Maeder’s track record, click here)

Once again, we’re looking at a stock whose Strong Buy consensus view is based on 3 unanimously positive ratings. TCMD shares are trading for $33.29 and their $67.33 average price target suggests a 12-month upside of 102%. (See TCMD stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.