It seems like investors have moved on from the slate of risks that weighed down the broader markets at the end of last year. As impressive as the S&P 500’s (SPX) run is, numerous Strong-Buy-rated stocks haven’t really picked up as much traction. However, these three names may be able to sweeten up your portfolio for what could be a choppier second half that follows what has been a bountiful first half.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Though a potential recession, more rate hikes, and geopolitical jitters are still very much on the table, such risks now seem to be taking a backseat to the rise of AI and other hot tech trends, like AR. Of course, tech stocks were due for a relief bounce at some point after the Nasdaq 100’s (NDX) grueling bear market moment last year. In any case, investors seeking to add exposure to more defensive areas have come to the right place.

In this piece, we’ll use TipRanks’ Comparison Tool to examine three Strong Buys in the defensive consumer staple space.

Coca-Cola (NASDAQ:KO)

Coca-Cola is a sweet stock to hold for all sorts of different economic environments. Arguably, Coke stock becomes sweeter when the times get rougher. Despite the S&P 500’s hot start, KO stock is actually down around 3% year-to-date. If volatility makes a return (specifically to the tech scene), I think KO may be in a spot to outperform on a relative basis. As such, I’m staying bullish on the $266 billion beverage juggernaut.

Shares of KO are sitting on a relatively strong level of support at around $60 per share. It’s where the stock peaked before the 2020 stock market plunge and where it’s spent quite some time in the last year and a half.

At 27 times GAAP trailing price-to-earnings (P/E), Coca-Cola shares are trading well below their five-year historical average P/E of around 33.6. Though the 3% dividend yield (on a forward basis) isn’t nearly as impressive as the likes of some of the ailing telecoms with yields closer to 7%, I do view the payout as much safer and higher growth, even if the economy were to stay stuck in a funk for longer than expected.

As Coke looks to expand its footprint into other beverage categories (think sports and energy drinks), I’d look for sales to grow in the low-to-mid single-digit range, regardless of what the broader economy and the tech trade will do from here. That’s defensive growth that’s pretty sweet, in my books!

What is the Price Target for KO Stock?

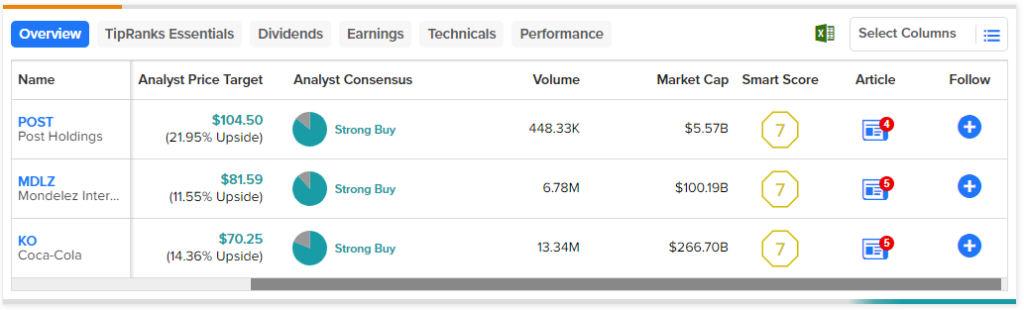

KO stock comes in as a Strong Buy, with 13 Buys and three Holds assigned in the past three months. The average KO stock price target of $70.25 entails 14.4% upside potential from here.

Mondelez (NASDAQ:MDLZ)

Mondelez is a top confectionary company that’s feeding the sweet tooth of many consumers. Oreos and other sweet treats are pretty cheap, given the utility (or happiness) they provide users. Even with higher prices amid inflation, consumers have shown they’re willing to open their wallets to satisfy their cravings. As “sticky” inflation sticks around for a while longer, I view Mondelez as a defensive staple stock that could continue to win big for investors. For that reason, I am bullish.

Mondelez stock is fresh off a 7% pullback after hitting a new high near $79 back in May 2023. At around 25.6 times trailing P/E (a tad cheaper than Coke), I believe MDLZ stock and its 2% dividend yield are worth snacking on right here.

Consumers are being more selective with how they spend, but they don’t seem ready to shift from Oreo to a lower-cost, off-brand alternative. Personally, I think it’s harder to switch from Mondelez snacks to generic alternatives than it is to switch from Coke to a private-label, off-brand cola. In that regard, I believe MDLZ stock ought to trade at a slight premium to KO shares.

At this juncture, MDLZ stock looks like a better deal, and many analysts seem to agree.

What is the Price Target for MDLZ Stock?

Mondelez is also a Strong Buy, with 15 Buys and two Holds. The average MDLZ stock price target of $81.59 suggests 11.55% upside over the year ahead.

Post Holdings (NYSE:POST)

Post Holdings is a St. Louis-based consumer-packaged goods firm behind popular cereal brands such as Pebbles, Raisin Bran, and Shredded Wheat. POST stock is down about 5% year-to-date but could be in a spot to gain ground as the market rally broadens out to some of the more defensive value names out there. At writing, Post stock looks the cheapest of the trio mentioned in this article, with a mere 13.4 times trailing P/E multiple, well below KO and MDLZ. This modest multiple has me bullish.

Post may have a tough time growing organically from here. Still, it always has the option to pursue inorganic growth. According to Barclays, Post could be in a spot to make more deals on the M&A front to jolt growth with a “buy-and-build” type of strategy. Such a strategy could be a major needle-mover on the stock, which trades at a discount to the packaged foods industry average of around 21.8 times P/E.

What is the Price Target for POST Stock?

Post Holdings sports a Strong Buy, with six Buys and one Hold. The average POST stock price target of $104.50 implies an impressive 21.95% upside from today’s prices.

Conclusion

Defensive stocks look pretty sweet if you’re looking to play a market pivot back to traditional value names. Currently, analysts expect the most gains from POST stock over the next year or so.