Due to the combination of elevated rates, slowing growth in travel demand and worries a global recession is about to play out in 2024 or 2025, the current operating environment for commercial aerospace does not look all that favorable.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

However, Stifel analyst Bert Subin thinks that when taking into account current production rates, capacity headwinds from GTF engine inspections and still healthy travel demand, the setup “starts to look better than feared” with the analyst seeing “greater potential for positive than negative surprises going forward.”

The above is particularly relevant to Boeing (NYSE:BA), with Subin counting three reasons to back the investment case for the A&D giant.

For one, once a mid-cycle is in view, Boeing tends to do well. “Boeing’s business relies on a well‐ functioning supply chain that can take quite a while to reboot after a downturn,” explains the analyst. “Now that we are getting to the point where the supply chain is improving and air travel demand visibility is better, we think there’s more upside than downside for Boeing as production re‐ramps.”

Secondly, narrowbody orders could get a boost from the problems with the Airbus A320 engine with hundreds of Pratt & Whitney PW1100G geared turbofan (GTF) engines taken out for inspection between now and 2026. But that, says Subin, could open up an opportunity for Boeing to reclaim some lost narrowbody share. “That would compliment strong demand on the widebody side and aid Boeing’s path back to sustainable FCF generation,” notes Subin.

Lastly, there’s the prospect of the 787 transitioning from a problem to an “FCF Driver.” When it comes to recent orders on the widebody side, and compared to Airbus’ A350 and A330, the 787 has been “the big winner.” If Boeing can exceed more than 10 builds a month, the company stands to gain a “material tailwind,” and with the new orders, Subin expects pricing power will begin to improve.

Summing up the investment thesis, Subin said, “BA is on track to see build rates improve, which, when paired with BGS strength and modest BDS improvement, should position the company to see material FCF growth over the next 2+ years that we think will drive upside for shares.”

So, where does this all leave investors? Subin initiated coverage of BA with a Buy rating to go alongside a $265 price target, suggesting shares will climb 14% higher over the coming months. (To watch Subin’s track record, click here)

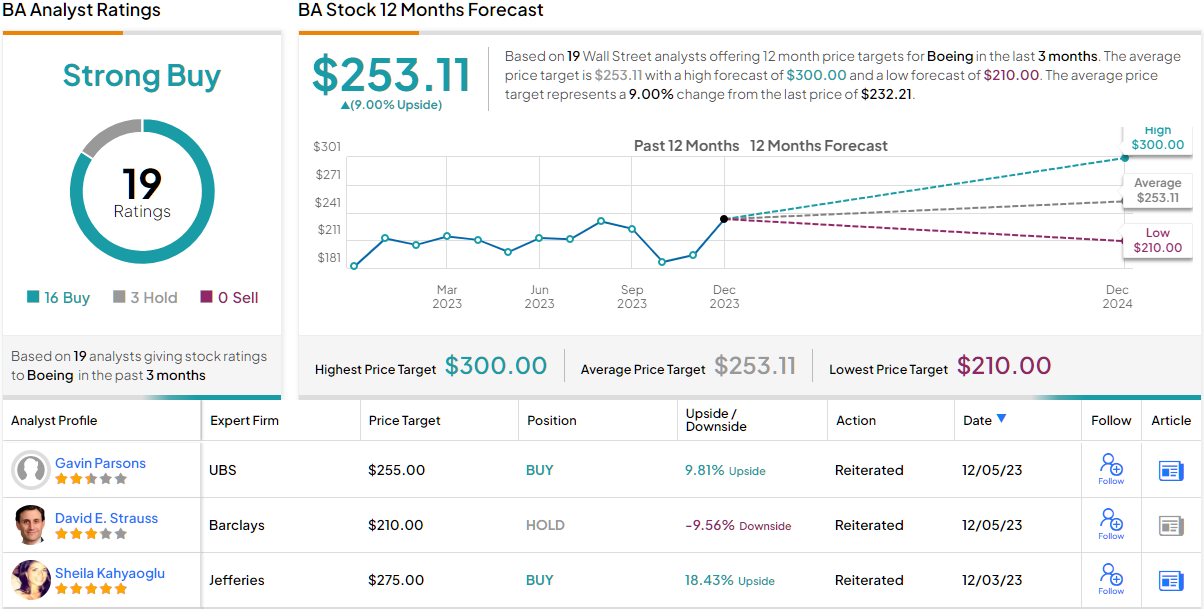

Subin’s take gets plenty of support on Wall Street. Based on a total of 16 Buys vs. 3 Holds, the stock claims a Strong Buy consensus rating. However, the upside appears somewhat capped; going by the $253.11 average target, the shares will post growth of 9% over the one-year timeframe. (See Boeing stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.