Real Estate provides an excellent hedge against inflation because rental income and property appraisals correlate with rising prices. However, the asset class isn’t liquid and often unaffordable to many.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Real Estate Investment Trusts (REITs) present a solution by offering investors real estate-backed listed securities at affordable prices. With inflation running at multi-decade highs, it’s evident that investors need to seek hedging products, and REITs provide just that.

Here are three REITs that I’m bullish on.

Power REIT (PW)

Power REIT is a progressive concept that invests in renewable agriculture properties with the aim of providing a modern illiquid concept to everyday market participants.

Tremendous intrinsic value has been added to this REIT lately. Power has scaled its intrinsic book value by 4.5x during the past year, while raking in a 1.36x growth in earnings from continuing operations.

Furthermore, the company’s acquisition pipeline provides promise. Power has more than $100 million in acquisitions on the cards, which comes on the back of an acquisition yield track record of more than 19%.

Power REIT holds satisfactory style factors and an attractive valuation. First of all, its price-to-earnings ratio is trading at a 50.2% sector discount, suggesting that the market underprices its earnings per share.

Additionally, Power REIT’s price-to-funds from operations ratio of 14.55x bestows an 18.8% sector-relative value gap.

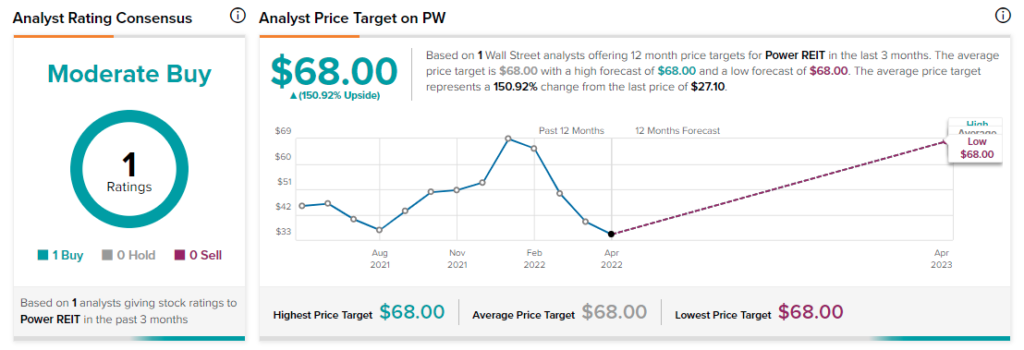

Turning to Wall Street, Power REIT earns a Moderate Buy consensus rating based on one Buy assigned in the past three months. The average Power REIT price target of $68 implies 150.9% upside potential.

Alpine Income Property Trust (PINE)

Alpine Income Property Trust is a retail-geared REIT situated in the United States. The company’s strategy is to use an anchor approach, whereby it targets high-end tenants to occupy their properties, which causes a pull on smaller tenants to pay higher rental premiums.

This REIT’s occupancy has been 100% since its listing as a publicly traded entity in 2019. Furthermore, Alpine’s success has seen it expand from 116 properties last year to 139 this year, which has proliferated its year-over-year cash flows by 72.9%.

Another attraction to this asset is its high rollover. Alpine’s lease rollover of 29% for the next decade hands it tremendous security, thus, improving the REIT’s risk-return profile.

Retail REITs are attractive because of their ability to charge a percentage of sales to their lessees, in addition to base rent. Although Alpine doesn’t provide a breakdown of such arrangements, it does work on a net lease basis, which causes its tenants to be responsible for most operating costs.

This asset provides value in abundance and is a lucrative income-generating option. To elaborate, Alpine exhibits a price-to-funds from operations ratio of only 11.76x, and carries a 5.53% dividend yield with it.

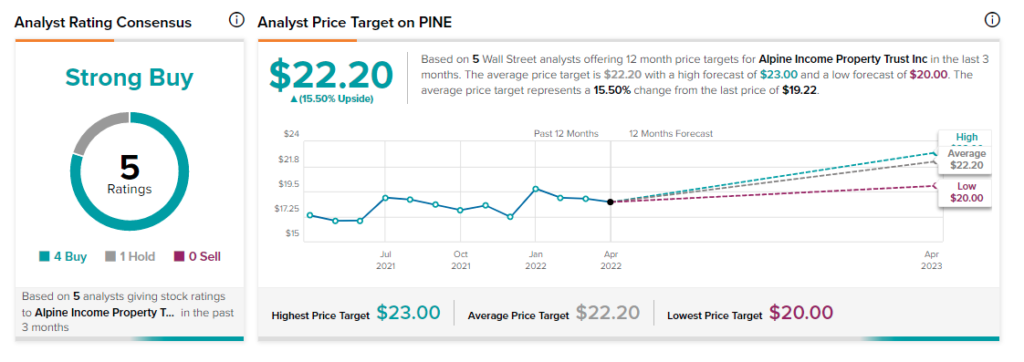

Turning to Wall Street, PINE earns a Strong Buy consensus rating based on four Buys and one Hold assigned in the past three months. The average Alpine price target of $22.20 implies 15.5% upside potential.

New Residential Investment Corp. (NRZ)

This REIT provides a debt-based opportunity to investors. New Residential Investment Corporation operates a mortgage-backed securities vehicle in the United States. The fund holds additional loan assets in consumer loans and opportunistic investments.

Debt REITs are ideal for investors who are betting on rising mortgage rates. Although mortality rates may rise with higher debt costs, REITs diversify the idiosyncratic risk away, thus delivering investors with a lucrative risk-return profile amid rising rates.

New Residential blasted past its fourth-quarter financial reporting estimate with a revenue beat of $112.65 million, and an earnings beat of one cent per share.

The company’s core earnings came in at $191.9 million, and its net income at $160.4 million. Furthermore, New Residential declared a quarterly dividend of 40 cents per share at a yield of 9.2%.

The asset’s full-year returns were bright, presenting a 17.3% return to its shareholders at a beta coefficient of 1.84. New Residential also illustrated solid growth in tangible book value with 15.1% growth during the year.

Furthermore, New Residential is undervalued with its price-to-earnings and price-to-sales ratios trading at sector discounts of 32.6% and 49.1%, respectively.

Turning to Wall Street, New Residential earns a Strong Buy consensus rating based on four Buys assigned in the past three months. The average NRZ price target of $12.75 implies 26.5% upside potential.

Bottom Line

There’s no guarantee that REITs will prevent an investment portfolio from suffering from inflation, but historical correlations suggest that they’re a prudent way to ride the inflation wave.

The companies in the article all possess robust portfolios, and solid fundamentals. Power and Alpine are lucrative growth REITs, and New Residential is a debt option for those looking to ride the recent surge in mortgage rates.

Discover new investment ideas with data you can trust.

Read full Disclaimer & Disclosure