Although fossil fuel prices have cooled off in recent weeks, stocks in this space continue to offer lucrative potential. Let us take a look at three promising names in the energy storage and transport space that have robust fundamentals and offer high dividend yields as well.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

The energy industry has been a major beneficiary of macro developments this year, with names such as Occidental Petroleum (OXY) popping brightly on the radar of the Oracle of Omaha. Simultaneously, ETFs in the energy sector, ProShares Ultra Oil & Gas (DIG) and Vanguard Energy ETF (VDE), are also up 102% and 46.6%, respectively, over the past year.

Kinder Morgan (KMI)

KMI shares have gained around 7.5% over the past five days, and the Street sees a further 14.8% potential upside. KMI is one of the biggest energy infrastructure names in North America with a presence of over 83,000 miles of pipelines, 141 terminals, and a natural gas storage capability of 700 billion cubic feet (bcf).

Revenues have increased from $11.7 billion in 2020 to $16.6 billion in 2021. Concurrently, earnings have expanded from $0.88 per share in 2020 to $1.32 per share in 2021.

In its most recent Q2, KMI continued to outperform across its segments, with higher commodity prices giving a boost to its CO2 segment. Additionally, the company’s natural gas pipelines segment continues to benefit from robust demand for transport and storage services.

Further, KMI is also investing in the global energy transition via pipeline and terminal support for renewable diesel, sustainable aviation fuel, and related feedstocks.

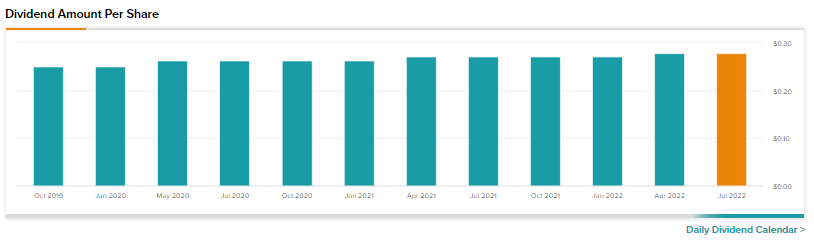

During the second quarter, KMI saw its earnings per share (EPS) balloon by nearly 182% and its discounted cash flow (DCF) per share grow by 16%. This robust performance is also helping the company provide a dividend yield of 6.16% with a payout ratio of 100.65%.

The Williams Companies (WMB)

WMB shares have gained nearly 6% over the past five days, and the Street sees a 16.9% potential upside in the stock, with an average price target of $39.22 and a Strong Buy consensus rating.

This Oklahoma-headquartered company operates across the natural gas value chain with transportation, storage, processing, and trading in natural gas as well as NGLs. Its pipelines span over 30,000 miles, and the company handles around 30% of natural gas in the U.S.

Revenues have expanded from $7.7 billion in 2020 to $10.8 billion in 2021, while EPS has expanded from $1.1 in 2020 to $1.36 in 2021. Most importantly, this bottom line is further expected to improve to $1.61 in 2023, indicating anticipation of an improved margin structure.

WMB’s Louisiana Energy Gateway clean energy project is expected to enter service in the latter half of 2024 and will create additional avenues for carbon capture as well as storage.

The company’s robust cash flow generation capacity is visible in a price to cash flow ratio of 9.6 and a price to free cash flow ratio of 31.5.

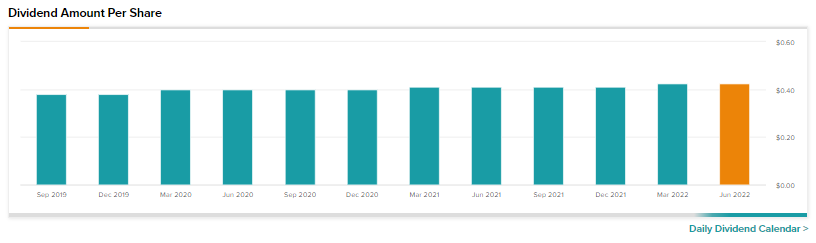

A beta of 0.46 implies the stock is more stable in the face of wild market gyrations. Finally, with a dividend yield of 5.16% at a payout ratio of 118.30%, WMB remains a consistent dividend distributor, having undertaken four dividend increases in the past five years.

Energy Transfer (ET)

The final name on our list has gained 3.5% in the past five days but offers the maximum upside according to Wall Street. Analysts have a Strong Buy consensus rating on ET alongside an average price target of $15.57, implying a massive 46.2% potential upside.

ET has a well-diversified energy asset portfolio in North America with a footprint across natural gas, transportation, storage, crude oil, NGLs, terminals, as well as NGL fractionation.

Of all the names on our list, only ET has seen accelerating fundamentals with revenue increasing from $38.9 billion in 2020 to $67.4 billion in 2021 and an EPS of $1.89 in 2021, compared to a net loss per share of $0.24 in 2020.

Furthermore, in its upcoming second-quarter numbers on August 3, the company is expected to report an EPS of $0.35 compared to $0.20 for the year-ago period, which is a 75% gain.

ET has been a beneficiary of soaring oil and gas prices, and shareholders have been benefitting with a dividend yield of 6.63% at a payout ratio of 63.96%. Furthermore, yesterday, the company boosted its dividend by 15% sequentially to $0.23, which is payable on August 19.

On top of the expected near 50% upside and the robust dividend yield, the stock is available at a reasonable price-to-earnings ratio of 10 and a price-to-sales ratio of 0.57.

This implies investors have to shell out 57 cents to buy each dollar the company generates in revenue. Finally, a price-to-cash flow ratio of 3.50 and a price-to-free cash flow ratio of 17.30 continue to point towards robust cash flow generation capacity.

Closing Note

In a gold rush, it pays to sell picks and shovels. These three energy infra names have established robust asset footprint across the value chain and may be expected to continue to reap the benefits of the world’s insatiable and ever-growing thirst for energy.

Read full Disclosure