The S&P 500 has spent the month of May bouncing in the range between 2,800 and 3,000. While the index remains 11% below its all-time high, there is a cautious sense of optimism, that the worst of the bear market is behind us.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investors may be feeling upbeat, and anticipating a recovery in 2H20, but times are still volatile. To make sense of them, TipRanks offers the Smart Score, a comprehensive tool which analyzes every stock in the TipRanks database according to 8 interrelated factors. The data is measured and collated by sophisticated AI algorithms, and used to generate a single score for each stock. Shown on a 1 to 10 scale, the Smart Score is based on analyst, blogger, and investor sentiment, and collective indicators such as hedge activity and insider trading.

Today, we’ll look at three high-yield dividend stocks that have earned a ‘perfect 10’ from the Smart Score. For investors seeking a clear forward path, the data shows that these are the picks most likely to bring solid returns. Each of these stocks combines its perfect Smart Score with a reliable dividend history, giving investors a secure income stream. Let’s dive in.

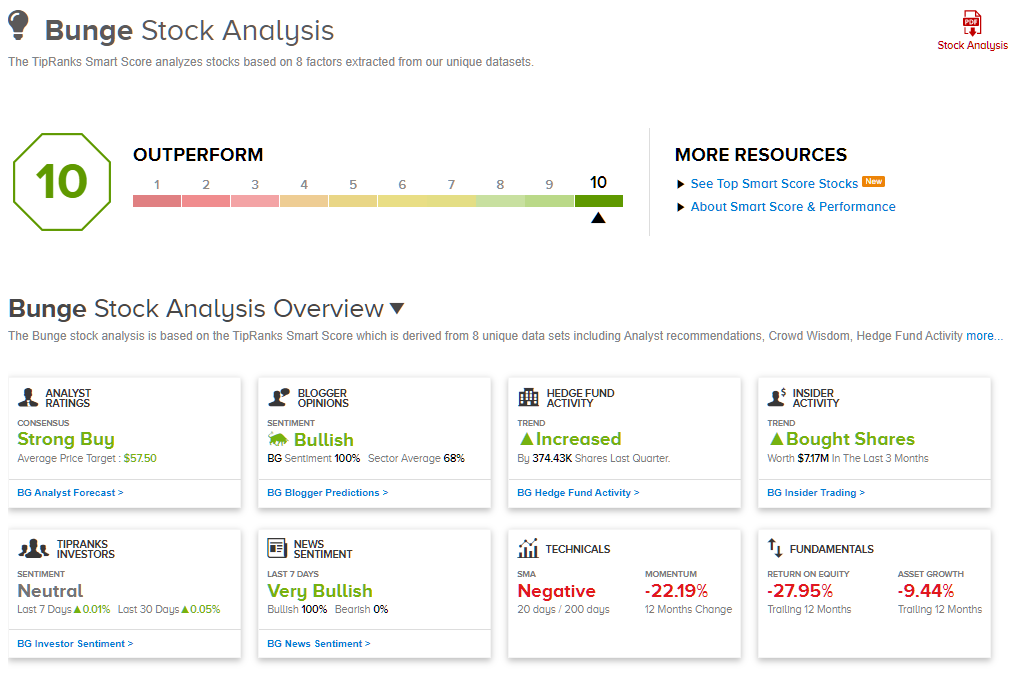

Bunge, Ltd. (BG)

First up is Bunge, an important company in the world’s food and agriculture food chain. Chances are, the food you eat depends on Bunge. The company specializes in oils and milled grains used by commercial brands and restaurants around the world. Bunge also deals in storage, transport, and processing of raw materials for end products in high-protein livestock feed. Other operations include corn, sugarcane, and wheat growing and processing.

Since we all need to eat, Bunge benefits from occupying an essential niche. Even so, the coronavirus pandemic found ways to hit the company. The various lockdown and shutdown policies enacted globally in Q1 slowed restaurant and commercial food businesses almost to a halt. BG saw reported income swing from a $1.27 per share profit in Q4 to a $1.34 per share net loss in Q1. BG shares have underperformed in recent months, and are still down 31% from February levels.

Despite the earnings slide, Bunge’s management has chosen to maintain the company’s dividend – a dividend that has been paid out regularly since 2001. At 50 cents quarterly, the current payment annualizes to $2.00, and gives an impressive yield of 5.65%. This is almost triple the 2% average yield found among peer companies in the industrial good sector.

The Smart Score on BG shares gets its boost from the ‘sentiment’ factors. As may be expected in a difficult market environment, the technical and fundamental analysis factors are negative – but insiders have purchased $9.9 million worth of BG shares in recent months, and hedge fund activity has also increased. The professional stock watchers, both analysts and bloggers, are also strongly positive on this stock. These upbeat indicators outweigh the negatives in this case.

Covering BG shares for BMO Capital, 5-star analyst Kenneth Zaslow writes, “BG remains our “Top Pick” for 2020, as BG’s underlying business fundamentals relative to its value appear to be largely misunderstood… BG’s internal operational improvements, nimble risk management framework, and underlying fundamentals enable BG to maintain its Agribusiness outlook… Despite BG’s stock reaction, BG’s economic earnings reduction represents less than 5% on EBITDA (i.e., majority is non-cash) and likely is temporary.”

In line with his position that this stock has a fundamentally sound foundation, Zaslow gives it a Buy rating. His $72 price target indicates his confidence, suggesting a 91% upside in the coming year. (To watch Zaslow’s track record, click here)

Wall Street is in general agreement that Bunge represents a buying opportunity. The Strong Buy analyst consensus rating is based on 4 reviews, including 3 Buys and a single Hold. Shares are priced at $35.53, while the average price target of $57.50 implies a health upside of 61%. (See Bunge stock analysis at TipRanks)

Hudson Pacific Properties (HPP)

Next up, Hudson Pacific, is a real estate investment trust, a type of company well-known for offering high-yield dividends. REITs operate by buying, managing, and leasing a range of residential and commercial properties, or by offering and investing in mortgages and mortgage-backed securities. HPP focuses on office space, in the lucrative Los Angeles, San Francisco, Seattle, and Vancouver markets. The company’s assets include 15 million square feet of leasable office space, located in prime high-tech development areas. Among Hudson’s clients are Alphabet and Netflix.

Q1 has been difficult for the REIT sector. With economic activity mainly shut down, business income streams have slowed to a trickle – which trickles down, as no income makes expenses, like rent, hard to meet. HPP reported EPS of 54 cents in Q1, down 2% from Q4, and Q2 is forecast at 50 cents. The company has maintained its dividend during the downturn – but this is no surprise, as the payout ratio is only 46% and REITs are required by tax code to return a high proportion of profits directly to shareholders. The 25-cent quarterly dividend represents a yield of 4.7%, more than double that found among peer companies.

Hudson shares many of the same Smart Score advantages as Bunge, above. Analyst and blogger sentiment are both positive, and hedge and insider purchases are both increasing. While most of the technical and fundamentals are in the red, one of them – asset growth – is highly positive. Asset growth is up 6.39% over the past 12 months. All of this adds up to a perfect 10 on the Smart Score.

Piper Sandler analyst Alexander Goldfarb is deeply impressed by HPP’s potential looking forward. He sees the company as uniquely well-positioned to benefit as the economy reopens: “We are even more bulled up by the prospects of increased demand for HPP’s studio and media-oriented assets coupled with its ability to re-imagine space for the gaming and entertainment industries. HPP stands alone in its material exposure to these industries (17% ABR to media and entertainment), which have a pressing need to return to production for new content in the wake of the binge consumption occurring during COVID… With talent hesitant to travel, car-loving LA makes HPP well positioned to not only re-open soon but also with the office product in high demand.”

Goldfarb puts a Buy rating on HPP, and his $28 price target implies a healthy upside potential of 21% for the coming 12 months. (To watch Goldfarb’s track record, click here)

The Street’s consensus on HPP is a Strong Buy, based on 5 Buy ratings and 1 Hold set in recent weeks. Hudson’s shares are selling for $23.14, and the average price target is slightly more bullish than Goldfarb’s; at $28.20, it indicates a 22% upside potential. (See Hudson Pacific stock analysis on TipRanks)

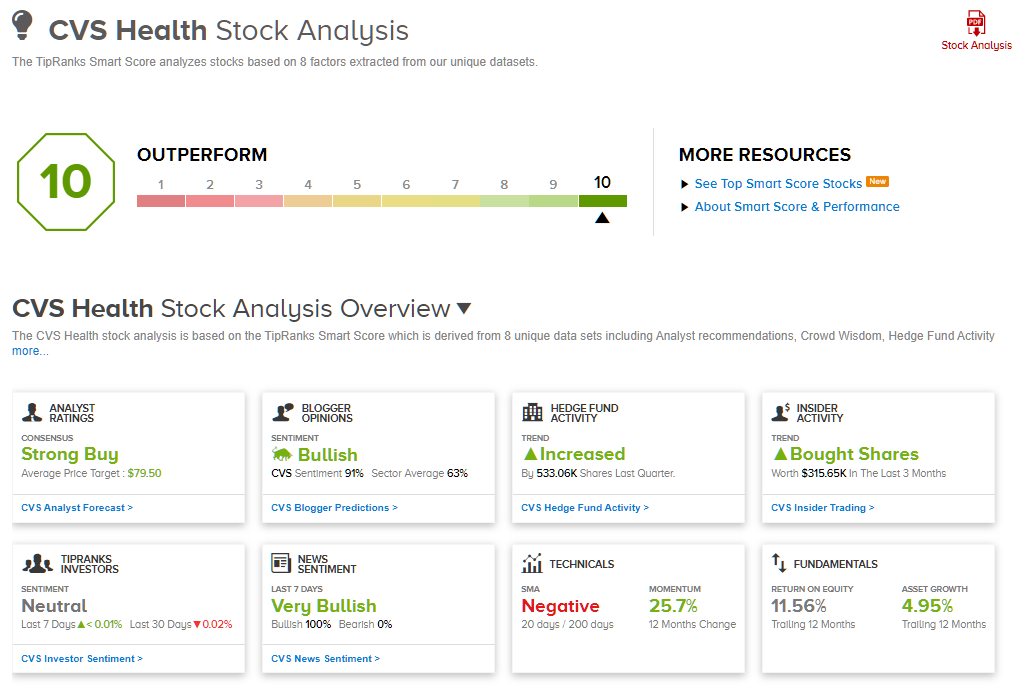

CVS Health Corporation (CVS)

Last on our list is a company you’re likely familiar with. CVS is well-known for its pharmacy chain, an asset that has proven especially valuable in the current climate. Unlike most companies – and the overall market – which saw declines in Q1 2020, CVS actually reported a quarterly earnings sequential gain. While the company had been expected to show a decline to $1.62 per share, EPS was reported at $1.91. This was up 10% from Q4, and an even stronger 19% year-over-year. The demand for pharmacy goods and service should be obvious to all.

Solid earnings support a solid dividend. CVS is paying out 50 cents quarterly, or $2 per year, on each share. The company has kept its dividend payments reliable for the last 15 years, in good times or bad, adding to the dividend’s allure. The current yield is 3.2%, which beats the 2.5% average yield found among peers in the consumer goods sector.

The Smart Score for CVS includes favorable views from analysts and bloggers, and heavy purchase activity from insiders and hedges.

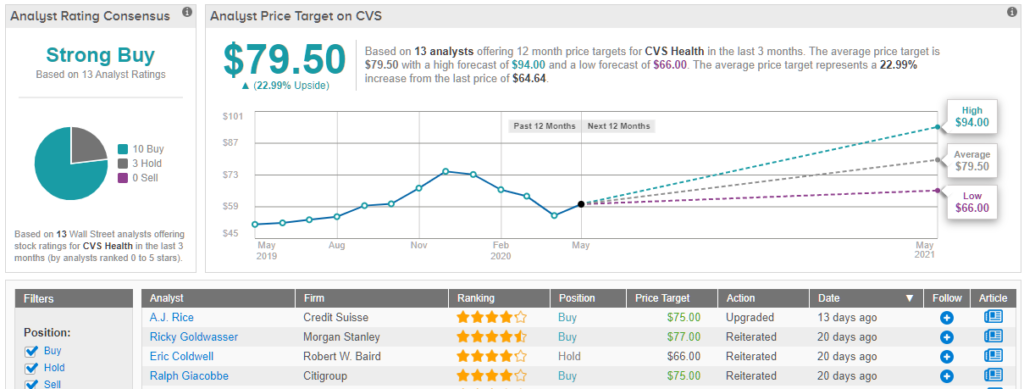

A good example of the positive analyst sentiment comes from Credit Suisse analyst A.J. Rice. Rice has upgraded his stance on this stock, raising his view from Neutral to Buy. His $75 price target suggests room for a solid 17% upside this year. (To watch Rice’s track record, click here)

Backing his view on CVS, Rice writes, “CVS’ Pharmacy Services Segment is Outperforming Expectations, as PBM Selling Season Shaping up Nicely. CVS is seeing an easing of rebate guarantee pressures which it saw peak in 2019, become less of a headwind in 2020, and are expected to be de minimis in 2021… CVS has remained on track-to-ahead of its synergies, modernization, and transformation initiatives, which could provide future upside.”

CVS shares have 13 recent reviews, breaking down to 10 Buys and 3 Holds and making the analyst consensus rating a Strong Buy. Shares are trading for $64.64, and the average price target of $79.50 implies a strong 23% upside potential for the stock over the next one year. (See CVS stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.