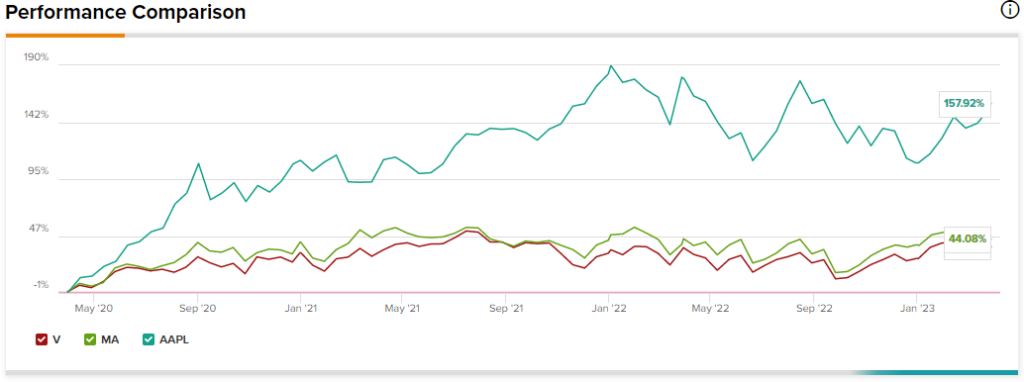

Payment tech stocks have been doing a relatively good job of holding up recently. Undoubtedly, a recession hasn’t yet begun, but many headwinds facing consumer spending may have already been priced in.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Looking ahead, it’ll all be about how the actual earnings results stack up against the now modest estimates.

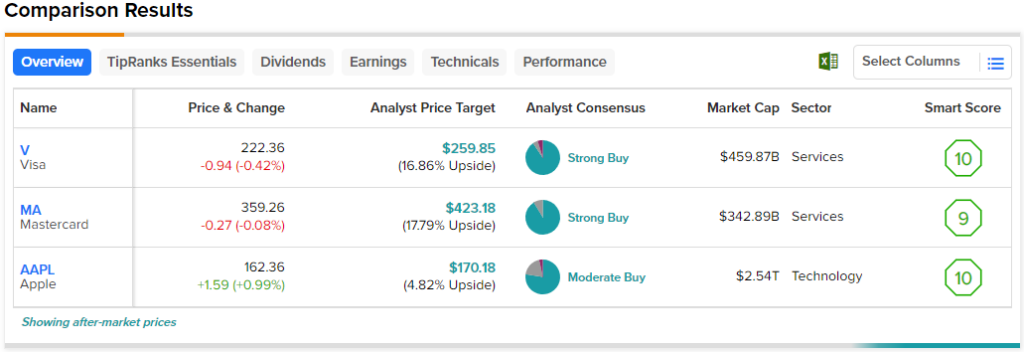

Currently, the analyst community seems bullish on the three payment-related tech stocks outlined in this piece — V, MA, and AAPL. Therefore, let’s use TipRanks’ Comparison Tool and analyze them.

Visa (NYSE:V)

Visa is a behemoth of a payments firm that has been rangebound in recent years. At $220 and change per share, Visa is only marginally higher than its pre-pandemic peak. Still, even with a recession considered, the company seems well-equipped to continue benefiting from several tailwinds that could help offset the macro headwinds on everyone’s mind. Therefore, I remain bullish.

There’s no question that payment volumes could fade as we all begin to feel the pain that recessions bring. Still, the recovery in international travel, which helped power strong results, may have legs as we move on from the COVID-19 pandemic to more “normal” conditions.

Apart from the ongoing travel recovery, Visa also stands to benefit from strong secular tailwinds. The shift to digital payments could help power many years’ worth of growth. In 2014, Visa highlighted the $25 trillion (yes, trillion) global spending market that payments firms seek to digitize. The market opportunity is likely even bigger now.

In the meantime, headwinds from a recession would offset the long-lasting tailwinds. After a recession, though, Visa will be in a fantastic spot. Still, don’t expect Visa to sit around waiting for the bad times to end. The company is investing across all fronts to maintain the width of its moat. The value-added services segment, in particular, is a corner where Visa can flex its muscles as it seeks to grow and diversify.

At writing, Visa stock trades at 31.9 times trailing earnings, well below its five-year historical average of 35.8 times. The historical discount, I believe, overplays recession headwinds and downplays longer-term secular tailwinds and the firm’s tech capabilities.

What is the Price Target for V Stock?

Wall Street loves Visa, with a Strong Buy rating composed of 19 Buys, one Hold, and one Sell rating. The average V stock price target of $259.85 implies 16.9% upside potential.

Mastercard (NYSE:MA)

Like Visa, Mastercard has a lot to gain as it does its best to digitize the massive global payments market. At writing, Mastercard stock is pricier than Visa at 35.2 times trailing earnings. However, despite the premium multiple, Wall Street expects more gains for the year ahead (17.8% versus Visa’s 16.9%). Indeed, Mastercard is more of a fintech-flavored credit card firm with digital know-how and the means to catch up to the likes of Visa, the market leader. I am bullish.

Undoubtedly, Visa is also innovating on the payment tech front. However, I’m more impressed by Mastercard and its tech capabilities. Just over a week ago, Mastercard acquired Sweden-based Baffin Bay Networks, a cloud cybersecurity firm. The Swedish cyber firm is behind AI-based “Cyber Shield.”

AI is at a pivotal moment. The Baffin Ban deal gives Mastercard a magnificent cybersecurity offering that should excite investors. As Mastercard amps up its cyber defenses, I find it tough to pass up on the stock even in the face of a rough recession.

What is the Price Target for MA Stock?

Wall Street loves Mastercard, with a Strong Buy composed of 21 Buys and two Holds. The average MA stock price target of $423.18 implies 17.8% gains.

Apple (NASDAQ:AAPL)

The iPhone maker made headlines on March 28 as it launched its Apple Pay Later service in the U.S. Indeed, Apple has been in the fintech field for quite a while with Apple Pay, Apple Wallet, and the gorgeous titanium Apple Card. The latest offering opens doors in the BNPL (buy now, pay later) space and could help the tech titan take its disruption in payment tech to the next level. I’m bullish on Apple stock.

Undoubtedly, Apple’s a tad late to the American BNPL game. The Apple Pay Later service landed later than expected, and with a recession closing in, it’s time that consumers trim away at their debt rather than raise any more of it. In any case, I see an opportunity for Apple to take significant market share away from incumbent BNPL providers.

At 27.3 times trailing earnings, Apple stock is too cheap to ignore. Its BNPL product should have investors excited over the share-taking opportunities. Further, there’s always the not-so-secret mixed-reality headset to look forward to this year. All catalysts considered, Apple stock looks worthy of a higher premium on its stock.

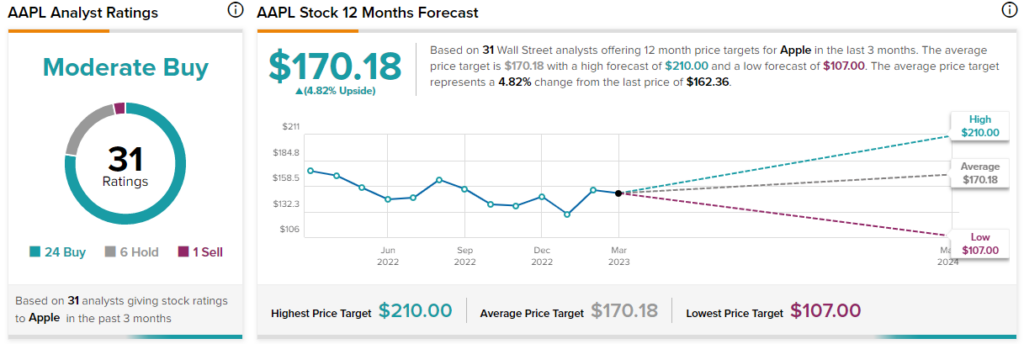

What is the Price Target for AAPL Stock?

Wall Street views Apple favorably, giving it a Moderate Buy consensus rating based on 24 Buys, six Holds, and one Sell. The average AAPL stock price target of $170.18 implies 4.8% upside potential.

Conclusion

Visa, Mastercard, and Apple are excellent payment tech stocks to consider. Of the three names, analysts expect the most upside from Mastercard.