The last decade has seen the rapid expansion of the digital world. Social media boomed, combined with internet search and e-commerce, and added video. The result was an explosion of content, a rapid increase in both the user and audience bases, and the creation of an enormous well of data – online records, personal data, purchase histories, entertainment preferences – that advertisers and marketers quickly moved to exploit. We all know about the automated advertising algorithms that curate the ads we see in social media.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

All of this isn’t just big business, it’s huge. Of the ‘Magnificent 7’ stocks that powered last year’s bullish stock market, three – Amazon, Alphabet (Google), and Meta (Facebook) – are directly connected to online advertising and AdTech generally, and their combined market cap exceeds $4 trillion. The world of AdTech is awash in money, coming in from multiple channels – direct digital advertising and marketing, pay-per-click, content creation and curation, AI-driven data mining.

For Brian Pitz, BMO’s internet & interactive entertainment analyst, these facts point to 2024 as a ‘breakout year for AdTech.’ The sector expert explains, “We forecast the global digital advertising market will grow from ~$500 million in 2022 to $668 million in 2024, when ~69% of all advertising dollars will be transacted digitally. These estimates could prove conservative given our expectation for robust digital ad spending around major events like the US presidential election and Paris 2024 Summer Olympics. GroupM projects that the ad dollars spent on the US elections and associated advocacy issues will reach $16 billion in 2024 (+31% since the last election)…”

Pitz wants investors to take advantage of this opportunity, and has initiated coverage on several AdTech stocks. According to the TipRanks data, Wall Street sees each as a Strong Buy choice; here are the details, and Pitz’s comments.

The Trade Desk (TTD)

We’ll start with a California-based firm, The Trade Desk. This is a technology and software company offering marketers, advertisers, and branding experts the tools they need to get the most bang for their AdTech bucks. The Trade Desk puts all of its Ad Tech tools into a single platform, making the product ‘home’ for its users. The company’s tools allow digital advertisers to optimize their ad spending and targeting, put their databases to work, and to increase the reach of their marketing efforts.

This company describes its mission as ‘making digital advertising better,’ a task it accomplishes through several steps. These include improving the reach of customers’ ad campaigns, improving the choices available to users and advertisers, and improving the return-on-investment of customers’ ad spends. Taken together, these will all power advertisers’ growth in the digital world.

Getting to the financial results, The Trade Desk sees a predictable pattern in its quarterly revenues. Q1 of a year starts low, and sales increase through Q4. This makes year-over-year comparisons more informative than quarter-over-quarter.

In the last quarter reported, 3Q23, the company reported a top line of nearly $493.3 million, up 25% year-over-year and beating the forecast by just over $6 million. At the bottom line, adj. earnings came to 33 cents per share, up from 26 cents in the prior year quarter and 4 cents per share better than had been expected. The Trade Desk finished Q3 with $1.07 billion in cash and liquid assets on hand, up from $1.03 billion one year previously.

On the negative side, the company disappointed investors somewhat with its lower-than-expected Q4 revenue guidance. Management predicted 4Q23’s top line to come in at $580 million, ‘at least,’ while the Street had been looking for $611 million or better. We’ll find out next month how the company’s Q4 results measure up.

For BMO’s Pitz, however, the key point here is that TTD has its fingers in a rapidly growing pot, offering an enormous field for opportunity – and the company is skilled at making the best of that. Pitz writes, “TTD is staring down a massive, growing TAM that is also mix-shifting towards ads bought and sold digitally. The global online ad market is forecast to exceed $1 trillion by 2027 (~4.5% CAGR), with ~75% transacted digitally. Over time, all ads should be bought and sold digitally, even offline ads. This mix-shift is a powerful tailwind for TTD, which would benefit even if the ad market stagnates.”

For forward-looking investors, Pitz adds, “Heading into 2024, we expect robust ad revenues driven by the US Presidential Election and Paris Olympics. Also in 2024, Google is expected to begin blocking third-party cookies in its Chrome browser, although this could be delayed (again). The Trade Desk seems well prepared with its open-source identify framework, ‘cookie replacement’ technology called Unified ID 2.0 (UID2).”

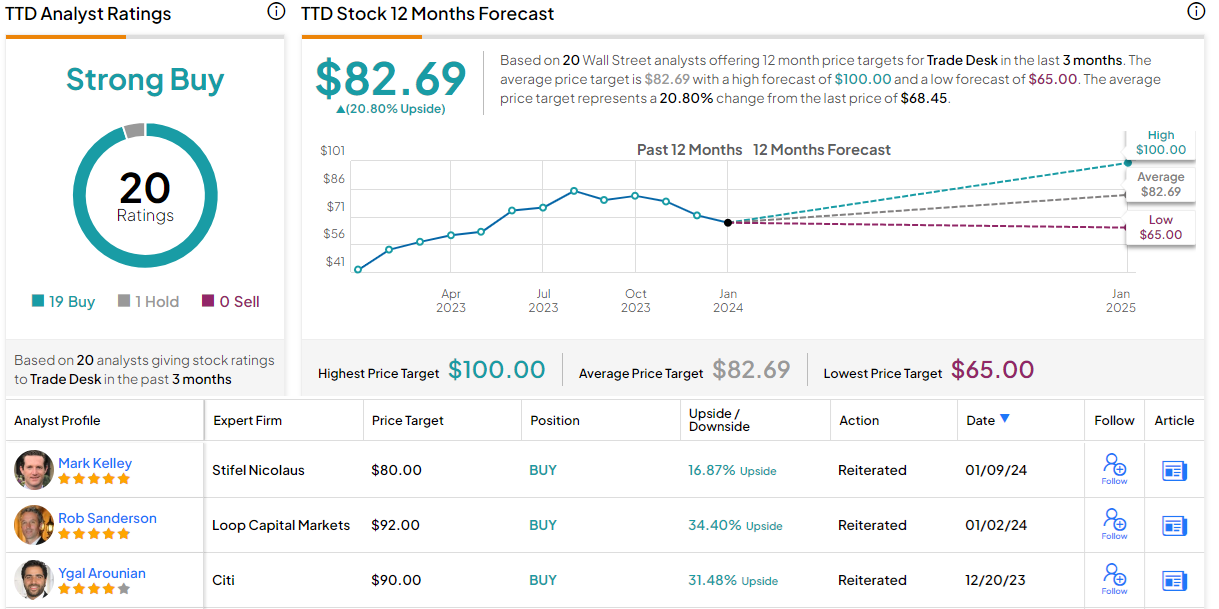

Taken all together, Pitz’s comments provide context for his Outperform (Buy) rating on this stock, and his $88 price target implies a gain of 28% in the next 12 months. (To watch Pitz’s track record, click here)

This AdTech leader has picked up 20 recent analyst reviews from Wall Street, including 19 to Buy against just 1 to Hold – for a Strong Buy consensus rating. The shares are priced at $68.45 and the $82.69 average target price points toward a 21% increase this year. (See TTD stock forecast)

DoubleVerify Holdings (DV)

Next on our BMO-backed list is DoubleVerify, a firm specializing in data measurement and analytic tools optimized for digital advertisers. The company’s software platform lets users optimize their digital ad spends, support multiple brand messaging, and bring a solid return on investment. The company describes its own business as trust – building trust with its customers, so that they can build trust with theirs – because when the digital world is trustworthy, providers and consumers alike will gain.

Building trust in the digital world, for DoubleVerify, means properly aligning its enterprise clients’ teams, missions, and customers. This requires a combination of transparency and authenticity, to ensure that digital advertisers are taking the right actions at the right time for the right reasons. In short, it needs accurate data analysis and measurement, that DoubleVerify provides.

The company’s stock was rising fast in the first half of last year, and then hit a stumbling block in August, falling almost 15% from July 31 to August 1. The share price drop came despite an upbeat 2Q23; at the same time as that earnings release, the company also announced its agreement to acquire Scibids, a leading company in the field of AI-powered digital campaign optimization.

While the acquisition was seen to be accretive for DoubleVerify, it was also seen as expensive. The move was said to cost $125 million, in a stock-and-cash transaction. DV paid half the price in cash, and has been funding the remainder through secondary stock offerings – which did dilute the shares somewhat. The deal closed in September of last year.

On the other hand, the 3Q23 report came in ahead of the forecasts all around. DV realized $144 million in revenue for the third quarter, up 28% y/y and $5 million better than had been estimated. Bottom line earnings, the GAAP EPS of 8 cents per share, were 2 cents per share over expectations.

Brian Pitz sees this company’s strong presence in fraud detection as a boon, given both the fast spread of undesirable online content and DV’s ability to screen that out. Pitz says of the company’s prospects, “Digital ad fraud is set to double to $172 billion by 2028. This fraud and waste comes in many forms, including bots, click fraud, made-for-advertising websites, disinformation, unsuitable or adult content, user-generated short-form video, bait-and-switch ad bidding techniques, and much more. DV seems best positioned with its platform, given our expectation that AI will only intensify these challenges for advertisers.”

In particular, the analyst sees an interesting opportunity for DV in the current US election cycle: “In 2024, we also note the US presidential election could be a meaningful catalyst for DV’s suitability solutions, which are designed to identify videos and UGC (user-generated content) that contains disinformation, misinformation, and fake news.”

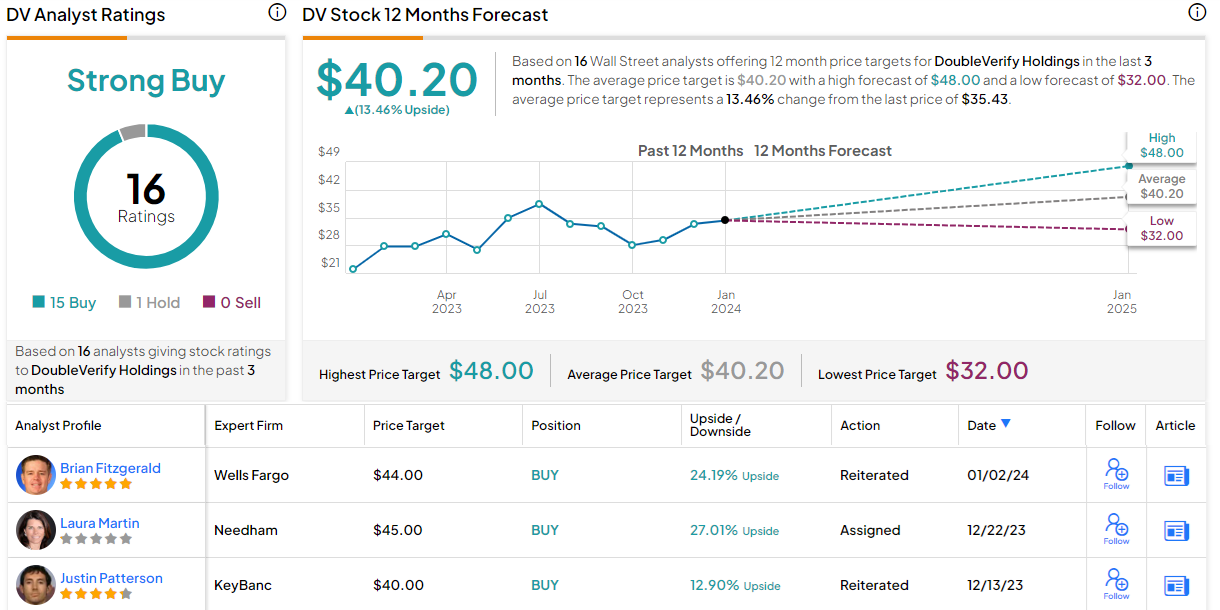

Pitz initiates his coverage here at Outperform (i.e. Buy), with a $44 price target implying a one-year upside potential of 24% for the shares.

DoubleVerify has a total of 16 recent reviews on record, and these include 15 Buys against a single Hold – to back up the Strong Buy consensus rating. These shares have a current selling price of $35.43, and their average price target of $40.20, indicates a potential to gain 13.5% in the year ahead. (See DoubleVerify’s stock forecast)

Integral Ad Science (IAS)

We’ll wrap up with a New York-based AdTech firm, Integral Ad Science. Like most AdTechs, IAS starts by focusing on the combination of data analysis with digital marketing, ensuring that ads and media are effectively and efficiently targeted for the maximum ROI. The company aims to create actionable fraud-free data solutions, to deliver superior results for its customers.

IAS gives its customers a platform for online advertising and media content optimization, with tools to give real-time data and performance insights, quality publication inventories to eliminate wasted impressions, and fraud detection and prevention to maintain online security. The company’s products are able to work across media platforms, offering a wide range of AI-based solutions to the complexities of modern digital advertising.

In the 14 years since its founding, Integral Ad Science has expanded to have a global footprint. The company employs more than 800 people, bringing services to customers around the world. The company boasts that its platform and solutions are in use in 111 countries.

IAS started out the new year with a new product announcement, for Quality Attention. This is the first data analysis product designed to unify media quality, eye tracking, and machine learning – a combination that provides direct measurement of an ad campaign’s quality, based on audience attention. Bringing these metrics together offers new ways to increase the advertising ROI, improve brand awareness, and boost conversion rates.

In its latest quarterly update, for 3Q23, IAS reported $120.3 million in revenues, beating the forecast by $7.11 million and growing 19% year-over-year. The bottom line did not fare as well; IAS saw a net loss for the quarter, of 9 cents per share by GAAP measures. This EPS was 9 cents below the expected break-even.

Analyst Pitz, an expert on online advertising, sees plenty of room for IAS to grow going forward, with solid opportunities in the expanding world of short-from video. He says of the company, “We see a meaningful opportunity for IAS on social media, particularly around monetization of short-form video platforms like TikTok, Instagram Reels, YouTube Shorts, and Facebook Stories. eMarketer forecasts video ads on social media will grow 17% Y/Y to $42 billion in 2024 (excluding YouTube), generating over half of total social network revenue. This could drive step-function growth for IAS in F2024, given Meta is already IAS’s largest social platform. Short-form, user-generated video can be unsuitable for brands given the significant amounts of unsuitable content on short-form video platforms.”

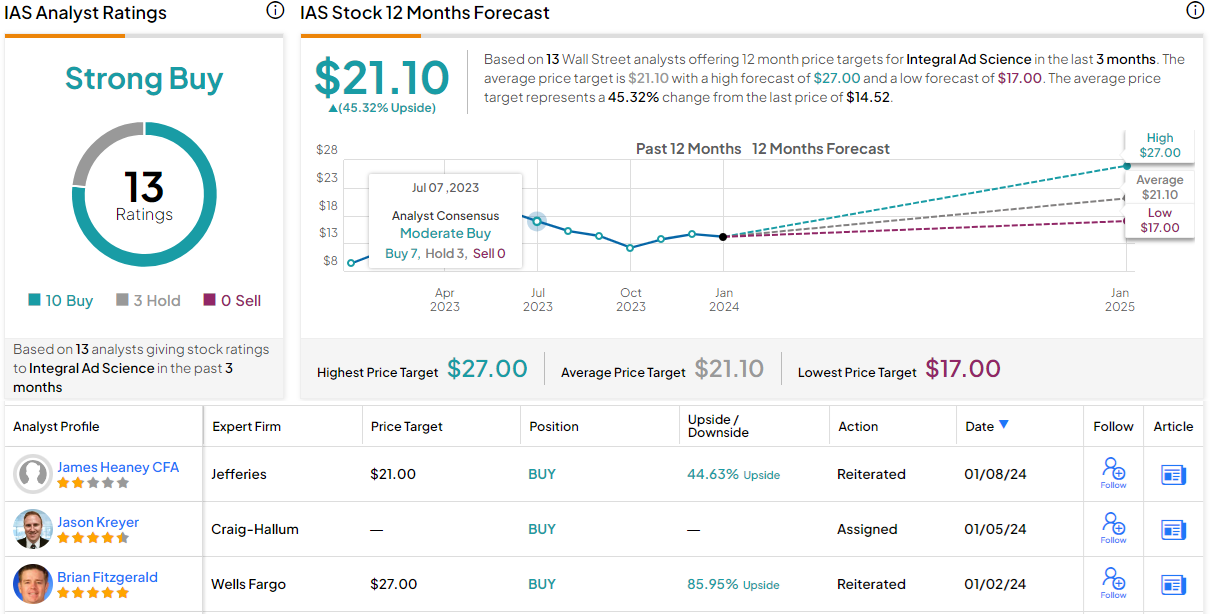

Once again, Pitz is initiating his coverage at Outperform (i.e. Buy), and he gives this stock a price target of $18 to suggest a 24% upside on the one-year horizon.

The Strong Buy consensus rating on this stock is supported by 13 recent analyst reviews, including 10 Buys to 3 Holds. Shares here are priced at $14.52, and the $21.10 average price target implies that IAS stock will appreciate some 45% over the next year. (See IAS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.