For return-minded investors, dividend stocks are the closest thing the market offers to a sure bet. They pay out a regular income stream on every share, and they pay it out whether the market moves up or down. It’s a feature that makes dividend stocks the classic defensive play.

There are two main attributes that define the high-quality div stocks; reliability and yield. The best dividend stocks will combine both attributes. For a patient investor, willing to take the dividends and reinvest them, these stocks are the closest thing the market offers to ‘sure thing.’

Wall Street’s analysts like dividend champs, too, so we’ve dipped into the TipRanks database to find two ‘Strong Buy’ dividend payers that are currently yielding at least 7% and have a reputation for maintaining steady payments. Here are the details.

Genco Shipping (GNK)

First up is Genco Shipping, a bulk carrier operator. The bulk trade is the workhorse segment of the world’s ocean trading network, and a vital part of the global supply chain. Bulk carriers haul a wide range of cargos, called drybulk, including grains, iron and other ores, coal, and steel and other metals. Genco’s fleet consists of 44 vessels, ranging in size from 55K dry weight tonnage Supramax ships to the giant 180K Capesize carriers.

While the supply chain crisis has been rough on national economies, Genco, with its focus on dry bulk shipping, has benefited from a jump in carrier charter rates. The company has seen its stock rise ~40% since the start of this year.

The company’s earnings and revenue have also reflected the pricing advantage. Genco reported $1.99 in earnings per diluted share for 4Q21, and a top line of $183.3 million. Both these numbers were the company’s best performance in over two years.

This strong performance led Genco’s management to implement a value strategy starting in 4Q21, and their first step was to increase the quarterly dividend. The new payment was set at 67 cents per common share, up a whopping 350% from the previous quarter, and the tenth consecutive quarterly dividend payment Genco has made. At the current rate, the dividend annualizes to $2.68 and gives a yield of 12.4%.

In his coverage of Genco, H.C. Wainwright analyst Magnus Fyhr sees the company is a solid position to both continue increasing the dividend and to continue updating its carrier fleet. He writes: “We believe GNK has ample liquidity to execute its new dividend strategy while meeting minimum annual debt amortization of $35 million…. Based on our 2022 average GNK fleet charter rate assumption of $24,800/day and cash break-even of $9,500/day, we estimate GNK could potentially pay a dividend of $2.61 per share in 2022. Furthermore, with a net loan-to-value of 16% or $166 million in pro-forma net debt, we believe GNK has added flexibility to pursue accretive acquisition to continue renewing its fleet.”

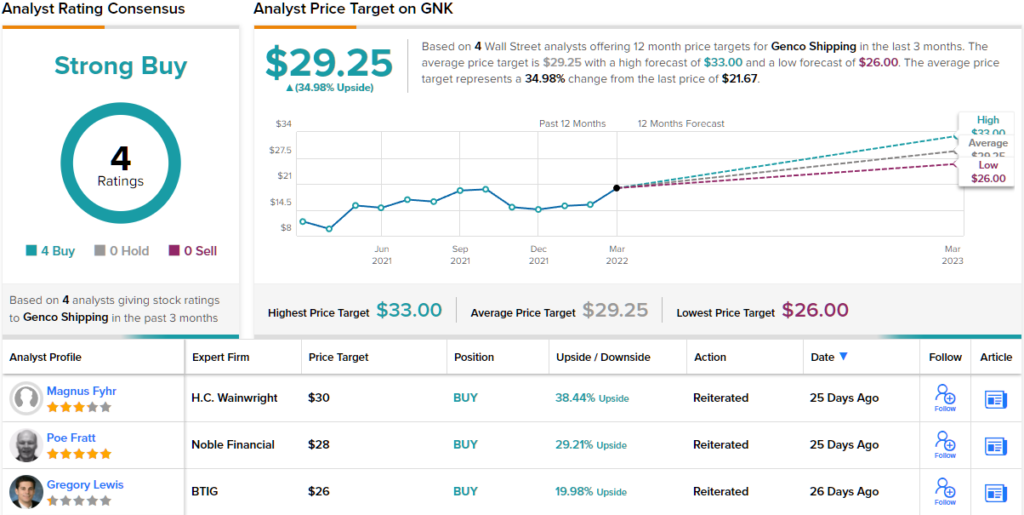

These comments support Fyhr’s Buy rating on the stock, while his $30 price target suggests an upside of ~39% for the year ahead. (To watch Fyhr’s track record, click here)

Overall, GNK has managed to pick up a unanimous Strong Buy consensus rating from Wall Street, based on 4 positive analyst reviews. The shares are selling for $21.67, and their $29.25 average target indicates room for ~35% appreciation by the end of the year. (See GNK stock forecast on TipRanks)

Sixth Street Specialty Lending (TSLX)

The second dividend stock we’ll look at is a specialty finance company, Sixth Street Specialty Lending. This company focuses on the small- to mid-market enterprise niche, making capital access available to firms that may not be able to secure credit with larger financial institutions. This is a vital niche in the financial industry, and the economy generally, as smaller enterprises have a history of driving US job creation numbers.

Sixth Street’s portfolio currently includes 69 companies, representing a range of industries including business services, software & tech, consumer & retail, manufacturing, healthcare, and energy. Portfolio target companies range in size from $50 million to $1 billion +, and Sixth Street makes capital available in loans between $15 million and $350 million. Sixth Street holds a range of such investments, including senior secured debt, mezzanine loans, and common equity.

As 2021 ended, Sixth Street reported gains in its investment income. For 4Q21, the company brought in $78.3 million, up from $62.2 million in the year-ago quarter. For 2021 as a whole, investment income totaled $278.6 million, compared to $270 million in 2020. Sixth Street’s investment income translated into 63 cents per share for Q4, easily beating the 53-cent forecast. Total investment EPS for 2021 came in at $2.16 per share.

This small-cap financial company has a long-standing dividend policy, that extends back 10 years. The company pays out a regular quarterly base dividend, along with supplementals and special dividends when applicable or as affordable. The most recent declaration, to be paid next month, is for a base dividend of 41 cents per share. This annualizes to $1.64 and gives a yield of 7.2%. Sixth street will also pay a quarterly supplemental dividend on March 31, of 11 cents per commons share.

Devin Ryan, 5-star analyst with JMP, paints an optimistic picture of Sixth Street’s prospects, writing, “We were encouraged by Sixth Street Specialty Lending’s strong fourth quarter to cap a terrific year, and more importantly, we see momentum continuing into the year ahead… Looking ahead to 2022, we believe Sixth Street Specialty Lending is positioned for another strong year given: 1) low leverage and significant available liquidity of $1.2B to grow the portfolio over time; 2) the support of a $60B leading direct lending platform in Sixth Street Partners, which has co-investment capacity; 3) excellent credit quality; and 4) a rising rate environment which should lead to NII expansion in the intermediate term and beyond…”

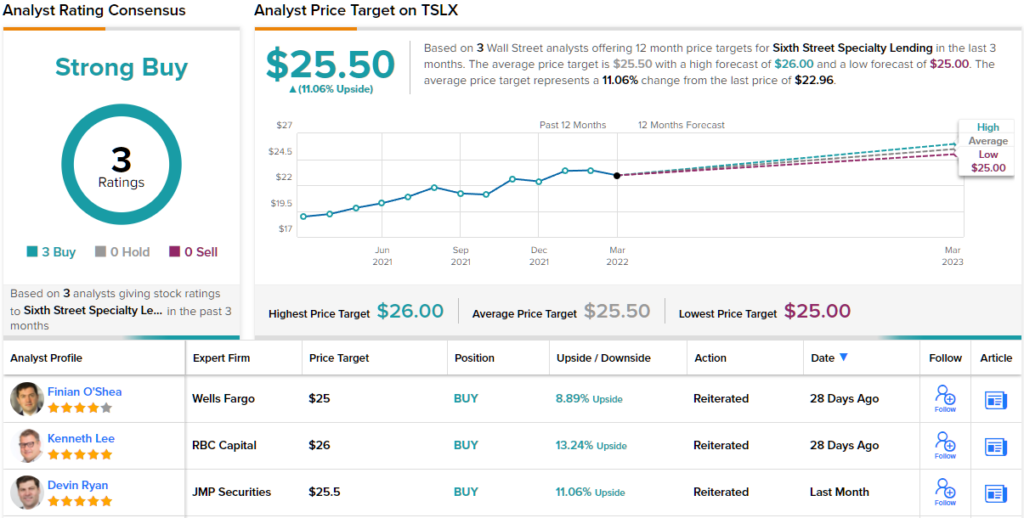

To this end, Ryan puts an Outperform (i.e. Buy) rating on Sixth Street, and his $25.50 price target suggests a 12-month upside of 11% for the shares. (To watch Ryan’s track record, click here)

While there are only 3 recent share reviews for Sixth Street, they all agree that it’s a stock to Buy, making the Strong Buy consensus rating unanimous. TSLX has an average price target of $25.50, matching Ryan’s, and a current share price of $22.95. (See Sixth Street stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.