The jobs market remains robust, and after hitting heights not seen during the last 40 years, it looks like inflation is cooling down. At the same time, there are still concerns a recession is on the way while the geopolitical landscape remains uncertain.

However, weighing the positives against the negatives, Oppenheimer’s Chief Investment Strategist John Stoltzfus believes the economy’s display of strength spells good news for the stock market.

“From our perch on the market radar screen the potential for things to get better even as uncertainty and risk persist on the landscape continues,” Stoltzfus recently said. “The resilience reflected in the economy in our view points to the potential for stocks to persist climbing the proverbial ‘wall of worry’ if not in a straight line higher.”

That will be music to investors’ ears, especially for those wondering where the best place is to park some cash right now. As it happens, Stoltzfus’ analyst colleagues at Oppenheimer have some ideas about that. They pinpointed two stocks they think are primed to push ahead – by the order of 30% or more over the following months.

We opened the TipRanks database to find out what the rest of the Street has to say about these names. Turns out there’s widespread agreement here; the analyst consensus rates both as Strong Buys. Let’s find out what makes them so.

RxSight, Inc. (RXST)

The first Oppenheimer-backed stock we’ll look at is an ophthalmic medical device company that has notched a big achievement. RxSight has developed and commercialized the world’s first adjustable intraocular lens (IOL) that allows for customization following cataract surgery. The FDA-approved proprietary RxSight Light Adjustable Lens system includes the Light Adjustable Lens (LAL) and the Light Delivery Device (LDD).

How does the RxSight system work, then? The LAL is implanted using a typical cataract process, refractive error is determined with patient input when healing is complete, and the LAL is then reshaped using the LDD with the precise amount of visual correction required to produce the patient’s preferred vision outcomes.

The company has been showing consistent top-line growth and that was on offer again in RXST’s latest quarterly readout – for 4Q22. Revenue reached $16.1 million, amounting to 91.7% year-over-year growth whilst meeting Street expectations. On the bottom-line, Adj. EPS of -$0.45 came in well ahead of the expected -$0.74. Looking ahead, the company guided for 2023 revenue in the range between $78 to $83 million, suggesting growth of 59% to 69% vs. 2022. Consensus was looking for $77.24 million.

The novel IOL tech has caught the attention of Oppenheimer analyst Steven Lichtman, who sees room for more growth ahead.

“Of the ~4.5M US cataract procedures, premium IOLs like RXST’s LAL account for +/-20%. We look for continued expansion of the premium IOL market over the next few years as the technology has improved and patients look for spectacle independence,” the 5-star analyst explained. “While there are risks to LAL adoption (high out-of-pocket cost, need for follow-up visits for adjustments), our survey work shows increasing interest and utilization in the technology from both current users and those looking to adopt near term. We see a path to meaningful gross margin expansion for this razor/razorblade story.”

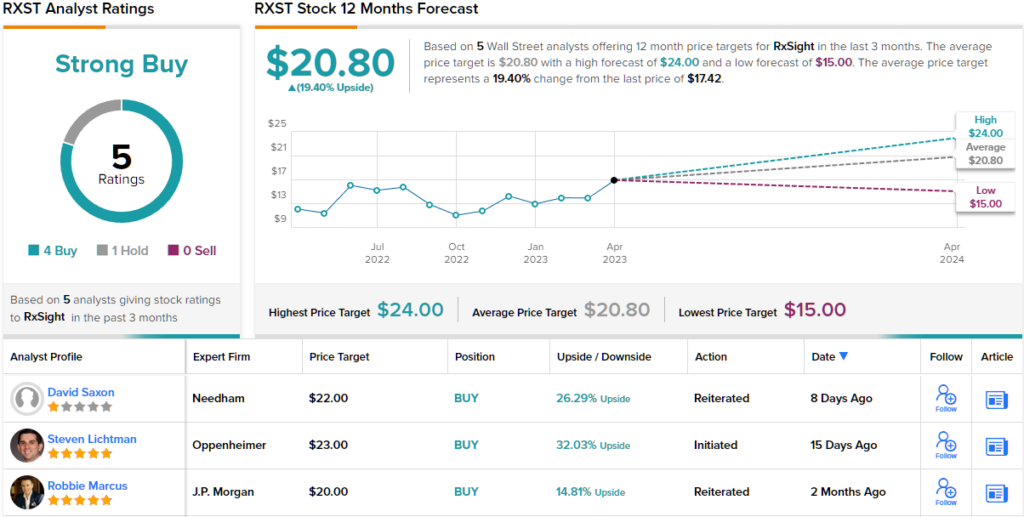

How does this translate to investors? Lichtman rates RxSight shares an Outperform and backs that up with a $23 price target. That figure implies 32% upside potential from current levels. (To watch Lichtman’s track record, click here)

Looking at the consensus breakdown, while one analyst remains on the sidelines, all 4 other analyst reviews are positive, providing this stock with a Strong Buy consensus rating. The Street sees shares climbing by 19% in the months ahead, given the average target clocks in at $20.80. (See RxSight stock forecast)

Advanced Drainage Systems (WMS)

No doubt, there’s not much glamour attached to a company called Advanced Drainage Systems but that doesn’t mean its value proposition isn’t sound.

Advanced Drainage Systems offers water management solutions and drainage products for use in the construction and agriculture sectors, namely the $6 billion stormwater and $1 billion onsite septic wastewater industries. Its product line includes plastic leach field chambers and systems, septic tanks, polypropylene and polyethylene pipes, water filters and water separators, amongst a host of other offerings.

Over the past 12 years, the company has noticeably bettered end-market growth (non-residential market by +10%, residential by +6%). That said, there was no top-line growth on tap in the company’s most recently reported results – for the fiscal third quarter of 2023 (December quarter). Revenue dropped by 8.4% year-over-year to $655.2 million, missing consensus by $58.37 million. Adjusted EBITDA also fell by 3.6% to $169.7 million. On the other hand, Gross profit rose by 7.1% to $223.9 million and net income climbed 11.7% to $83.2 million. However, at $0.99, EPS still fell short of the $1.22 forecast.

The soft results are no turn off for Oppenheimer’s Bryan Blair. The 5-star analyst recently initiated coverage of WMS and sees plenty to like about the company.

“The team’s comprehensive product portfolio, unmatched scale and resource support (including an expansive sales network, engineering staff, and company-owned fleet of 700 trucks and 1,250 trailers), and the continued material conversion (favoring plastic) of stormwater and septic systems all bode well for sustained outperformance,” Blair wrote. “Although construction-driven stocks remain generally out of favor (particularly those with non-res concentration), we view near-term estimate risk as well understood with solid, likely underappreciated upside potential over F2H24-FY25.”

These comments form the basis for Blair’s Outperform (i.e., Buy) rating on WMS, while his $108 price target implies one-year share appreciation of ~34%. (To view Blair’s track record, click here)

Overall, Wall Street likes this drainage solutions stock. All 6 recent analyst reviews are positive, making for a Strong Buy consensus rating. Going by the $114.33 average target, the shares will surge ~41% in the months ahead. (See WMS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.