The doom and gloom brigade has been out in full force recently, persistently warning the economy is in a precarious state and that a recession next year is all but inevitable.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Maybe so, but that doesn’t necessarily mean the stock market is destined to follow suit. In fact, the J.P. Morgan Asset Management team expects 2023 will be a “bad year for the economy, a better year for markets.”

“Our core scenario sees developed economies falling into a mild recession in 2023,” added Asset Management team leader Karen Ward. “However, both stocks and bonds have pre-empted the macro troubles set to unfold in 2023 and look increasingly attractive.”

So, with 2023 at the gate, which specific stocks present an opportunity? That’s a job for the analysts to figure out and those at J.P. Morgan have pinpointed 2 names which look very attractive right now – they see both adding over 50% in value over the coming year. According to TipRanks database, the rest of the Street is on the same page, with each ticker earning a “Strong Buy” consensus rating.

Rallybio Corporation (RLYB)

We’ll start off in the biotech space – a segment exemplifying the high-risk/high-reward paradigm. Rallybio is a clinical-stage biotech focused on developing drugs for serious and rare diseases.

The company’s lead candidate is RLYB212 – a monoclonal anti-HPA-1a antibody – being developed for the prevention of fetal and neonatal alloimmune thrombocytopenia (FNAIT) and currently undergoing a phase 1b POC (proof of concept) trial in healthy volunteers.

FNAIT is a rare condition defined by the maternal immune system assaulting fetal platelets, the result of which is neurologic disability, miscarriage/still birth, and/or death. Preliminary results from the RLYB212 phase 1b study were announced at the end of September and there’s a near-term catalyst from the announcement of the Phase 1b POC results in 1Q23.

Rallybio is also developing RLYB116, a C5 inhibitor administered subcutaneously, indicated to treat patients with paroxysmal nocturnal hemoglobinuria (PNH) and generalized myasthenia gravis (gMG). A multiple ascending dose phase 1 study of this drug should kick off in 1Q23 too.

For J.P. Morgan analyst Anupam Rama, it is the potential of RLYB212 which is most eye-catching.

“Longer term, we see RLYB212 as providing multiple long-term upside levers for RLYB shares based on probability of success increases (pending data readouts) and market drivers (diagnosis / awareness rate increase, penetration rate, and pricing),” the analyst explained.

“Importantly,” the analyst went on to add, “we are taking a more conservative approach to the model in terms of peak sales for RLYB212, which is on the lower end of the peak Street consensus range for both sales and probability of success (WW peak sales – JPMe ~$1.2B; Street range ~$1- 1.7B). Even with this approach, we see meaningful upside potential in RLYB shares from current levels.”

To this end, Rama rates Rallybio shares an Overweight (i.e. Buy), unsurprisingly in light of his comments, and sets a $21 price target that suggests a hefty 350% one-year upside for the stock. (To watch Rama’s track record, click here)

Overall, Rallybio has the Street’s full support; all 6 reviews on record are positive, providing the stock with a Strong Buy consensus rating. The average price target is an upbeat one; at $27, the figure suggests shares will yield returns of 478% over the next 12 months. (See Rallybio stock forecast on TipRanks)

Samsara Inc. (IOT)

For the next J.P. Morgan-backed stock, the ticker gives the game away. Samsara’s field of expertise lies in the digitally connected realm, more specifically – the Internet of Things.

The company runs a connected operations platform designed to track fleets of vehicles and other equipment; it enables real-time connectivity between physical assets and people. The outcome of this process is automation, which in turn extends the life of assets, enhances worker productivity and safety, and boosts the performance of the company as a whole.

Going by the latest set of quarterly results, you could say the platform is gaining traction. In fiscal Q3 (October quarter), revenue climbed by 49% year-over-year to $169.8 million, beating the Street’s call by $14.4 million. Non-GAAP EPS of -$0.02 not only improved significantly from the $0.12 loss seen in the same quarter a year ago, but also came in ahead of the -$0.06 expected by the analysts.

Even better, for the Q4 outlook, the company expects revenue between $170 million – $172 million compared to consensus at just $161.38 million.

The stock, though, has in no way been immune to the market woes of 2022; despite the upbeat reaction to the latest financial statement, the shares are still down by 51% on a year-to-date basis.

Assessing the print, J.P. Morgan analyst Noah R Herman sees plenty to be upbeat about – both on the results front and going forward.

“The company achieved a ‘Rule of 40’ for the first time, including revenue growth and adj. FCF margin,” Herman noted. “Adj. FCF margin guidance for FY23 slightly improved, as Samsara notes better operating efficiency and working capital optimizations. On the macro front, the company is seeing solid sales cycle conversions and the overall pipeline hasn’t changed materially compared to 2Q. We continue to believe Samsara is attractive for long-term investors, as the company is in the early stages of digitally transforming physical operations.”

In Herman’s view, this justifies an Overweight (i.e. Buy) rating, and his $21 price target indicates his confidence in a one-year upside potential of 53%. (To watch Herman’s track record, click here)

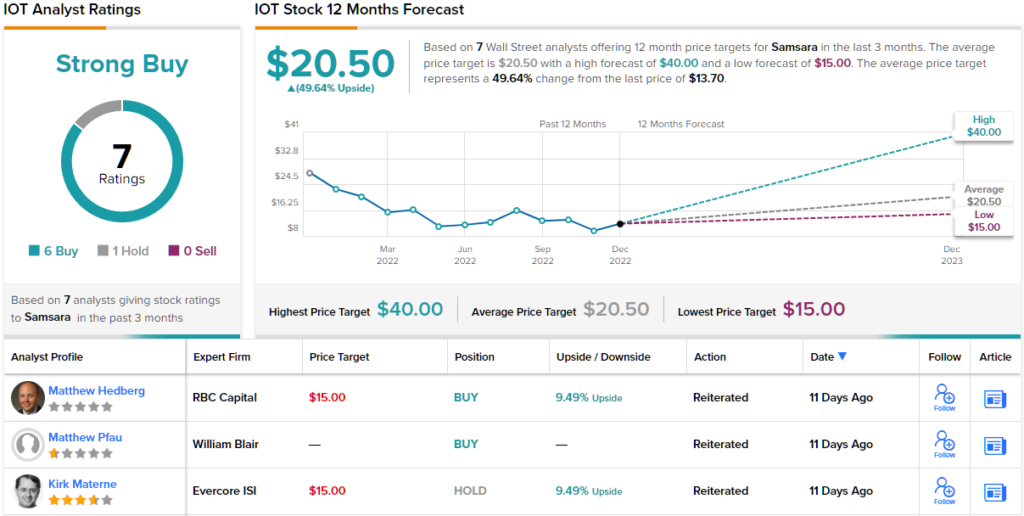

Most analysts agree with Herman’s stance. Barring one skeptic, all 5 other recent reviews are positive, making the consensus view here a Strong Buy. Going by the $20.50 average target, the shares will appreciate ~50% over the next 12 months. (See Samsara stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.