Let’s talk about winning in the stock market. You can make money no matter what the overall economic conditions are – whether stocks go up or down, there will be opportunities to profit by the moves. The key, of course, is understanding when to buy in and when to sell. Every stock will come with the potential for both risk and reward; successful investors know how to balance them.

Few stock segments offer a more interesting – and, potentially, more profitable – risk/reward profile than the penny stocks. These equities, typically priced under $5 per share, offer a minimal cost of entry, and frequently triple-digit upside potential.

For some, however, the risk poses too great a threat to ignore. When you look under the hood of these low-priced names, you might find very real problems like poor fundamentals or looming headwinds.

So, how are investors supposed to spot the penny stocks poised to go from rags to riches? By turning to the pros.

Using TipRanks’ database, we pulled two penny stocks that have amassed enough analyst support to earn a “Strong Buy” consensus rating. Not to mention each offers multi-bagger upside potential. Let’s take a closer look.

Aravive, Inc. (ARAV)

We’ll start with Aravive, a clinical-stage biopharmaceutical company with one major drug candidate, batiraxcept, under investigation in multiple, simultaneous human clinical trials against various cancers. The company’s goal is to transform targeted cancer therapeutics, using batiraxcept, its new compound, in combination with approved anticancer treatments, with the goal of improving the treatment of metastatic disease.

Batiraxcept is described as ‘an ultra-high affinity decoy protein that binds to GAS6, the sole ligand that activates AXL, inhibiting metastasis, tumor growth, and restoring sensitivity to anti-cancer agents.’ The drug candidate has received Fast Track designation from the US FDA as well as an Orphan Drug designation from the European Commission, both in the treatment of platinum-resistant ovarian cancer (PROC).

Currently, batiraxcept is undergoing two Phase 1b/2 clinical trials, one in the treatment of pancreatic adenocarcinoma and one in the treatment of clear cell renal carcinoma. Both trials are testing the drug candidate as a combination therapy, and data readouts are expected in mid-2023.

The leading trial, however, the driver of investor interest in this company, is the ongoing Phase 3 study of batiraxcept-plus-paclitaxel in the treatment of PROC. Enrollment in this trial was begun last year, and the top-line data release is anticipated in the mid-part of this year. The study aims to enroll up to 350 patients with platinum resistant, high-grade serous ovarian cancer, who have already tried 1 to 4 other lines of treatment. The company is currently on track to complete its BLA submission for batiraxcept in the treatment of PROC during 4Q23.

With multiple shots on goal, several analysts believe that at $1.80 per share, now is the time to pull the trigger.

Among them is H.C. Wainwright analyst Joseph Pantginis, who has high hopes for Aravive. He writes, “We highlight Aravive as a top pick to keep an eye on as it continues to advance batiraxcept through its oncology-focused clinical pipeline. With several clinical milestones approaching in 2023, we believe now is an opportune time for investors to take a closer look at Aravive, with a particular emphasis on the upcoming top-line data from the registrational Phase 3 study AXLerate-OC of batiraxcept for the treatment of platinum-resistant ovarian cancer (PROC).”

“In PROC, Aravive has potential for best-in-class potential with the differentiated mechanism of batiraxcept synergizing with current SOC chemotherapy regimens and providing significant quality of life improvements in patients,” the analyst added.

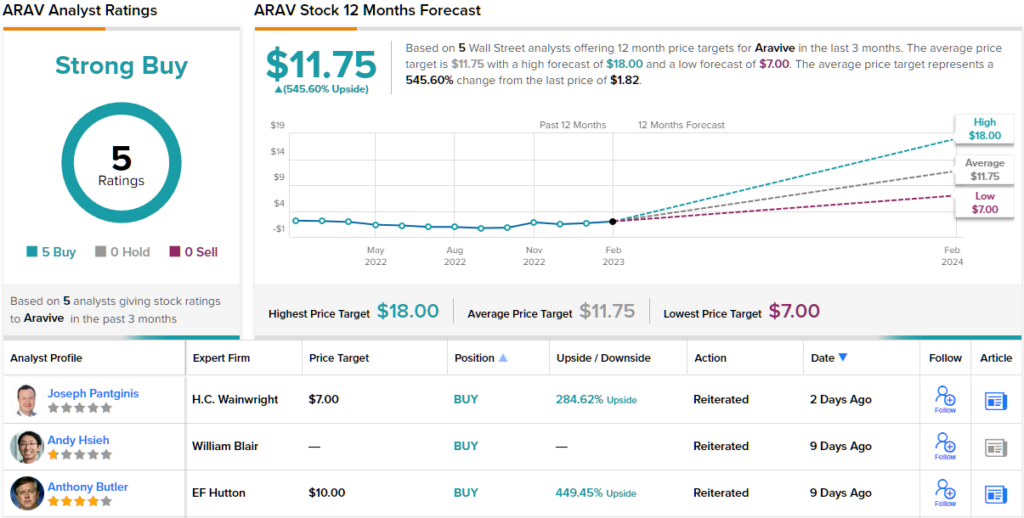

In line with this optimistic stance, Pantginis puts a Buy rating on ARAV stock. His $7 price target suggests a one-year upside potential of ~285%. (To watch Pantginis’ track record, click here)

That’s a bullish take, but the Street generally leans even more to the bullish side on this stock. All 5 of the recent analyst reviews are positive, for a unanimous Strong Buy consensus rating, and the average price target of $11.75 suggests a sky-high 545% upside potential on the one-year horizon. (See ARAV stock forecast on TipRanks)

Spruce Biosciences (SPRB)

We’ll now turn our attention to Spruce Biosciences, a biopharmaceutical company working on the treatment of rare endocrinological disorders with significant unmet medical needs – that is, conditions of the endocrine system that do not currently have effective treatments available. Spruce’s leading drug candidate is tildacerfont, which is being investigated as a therapy for both adult and pediatric congenital adrenal hyperplasia (CAH), as well as for polycystic ovary syndrome (PCOS).

Tildacerfont is a wholly-owned drug candidate, and Spruce currently has it in several clinical trials. The leading studies, dubbed CAHmelia-203 and CAHmelia-204, are testing the drug against adult classic congenital adrenal hyperplasia. These late-stage trials both have upcoming milestones. The -203 study, which is looking at patients with high levels of androstenedione (A4) while on their current glucocorticoid regimen, is currently 50% enrolled with a target enrollment of 72. The company expects to release topline results in the second half of this year.

On the second advanced trial, CAHmelia-204, the company has recently passed 25% enrollment, with a total planned patient base of 90. The study is looking at patients on supraphysiologic doses of glucocorticoids at or above 30 mg/d hydrocortisone equivalent with normal or near normal levels of A4. Spruce anticipates releasing topline results in 2H24.

In addition to these studies, Spruce is also conducting a Phase 2 trial series, the CAHptain clinical study, in pediatric classic CAH. This study will follow three sequential cohorts, looking at adolescents ages 11 to 17 and children ages 2 to 10, and is looking to release topline data from the adolescent portion of the study – cohorts 1 and 2 – during 2H23.

On the PCOS program, Spruce is running the P.O.W.E.R. Phase 2 trial, a study designed to evaluate the safety and efficacy of tildacerfont at a dose of 200 mg once daily. The topline data release for this trial is expected during 1H23.

No companies act in a vacuum, and Spruce faces competition in its research niche from other biopharma researchers. Competitor NBIX’s drug candidate, crinecerfont, is under investigation in both adult and pediatric patients, and the company plans to report the registrational data in 2H23. The competition, however, has not stopped RBC analyst Gregory Renza from coming down in favor of Spruce.

“We continue to like the risk/reward at current levels going into CAHmelia 203 topline and believe the recent landscape development improves SPRB’s positioning. With NBIX pushed out with a now set pivotal topline of crinecerfont to 2H23, we believe the gap from data from the two CAHmelia studies have improved SPRB’s positioning. We look to CAHmelia 203 topline data in 2H2023 to assess tildacerfont’s profile, as well as to compare with crinecerfont to further gauge product differentiation,” Renza opined.

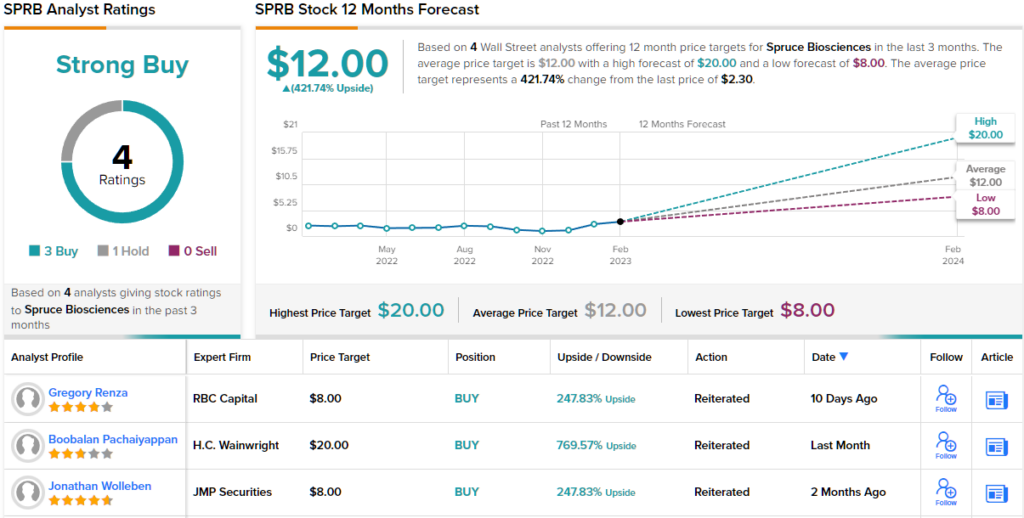

To this end, Renza gives SPRB an Outperform (i.e. Buy) rating with an $8 price target that suggests room for ~248% share appreciation over the coming year. (To watch Renza’s track record, click here)

Overall, there are 4 recent analyst reviews for SPRB, and their breakdown of 3 Buys and 1 Hold gives this penny stock a Strong Buy consensus rating. The shares are trading for $2.37, while their average target of $12 implies a strong gain of ~422% in the next 12 months. (See SPRB stock forecast at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.