We’re in a volatile bear market right now, and key riddle investors need to answer is, which stocks are going to bring the best returns, even in today’s uncertain conditions. One market segment that can’t be ignored is the low-cost penny stocks. These equities, typically priced under $5 per share, offer the best combination of risk and reward: a minimal cost of entry, and frequently triple-digit upside potential.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Going beyond the argument that you get more for your money, even minor price appreciation can result in massive percentage gains. However, some investors prefer to avoid these stocks entirely, as the fact that shares are trading at such depressed levels could signal insurmountable headwinds or weak fundamentals.

The key here is to find the difference between penny stocks priced low due to poor fundamentals, and those whose prices are low due more to bad luck or simple prevailing market conditions.

To help with the due diligence process, we’ve used TipRanks’ database to zero in on only the penny stocks that have received bullish support from the analyst community. We found two that are backed by enough analysts to earn a “Strong Buy” consensus rating. Not to mention each offers up massive upside potential, as some analysts see them climbing to $14, or more.

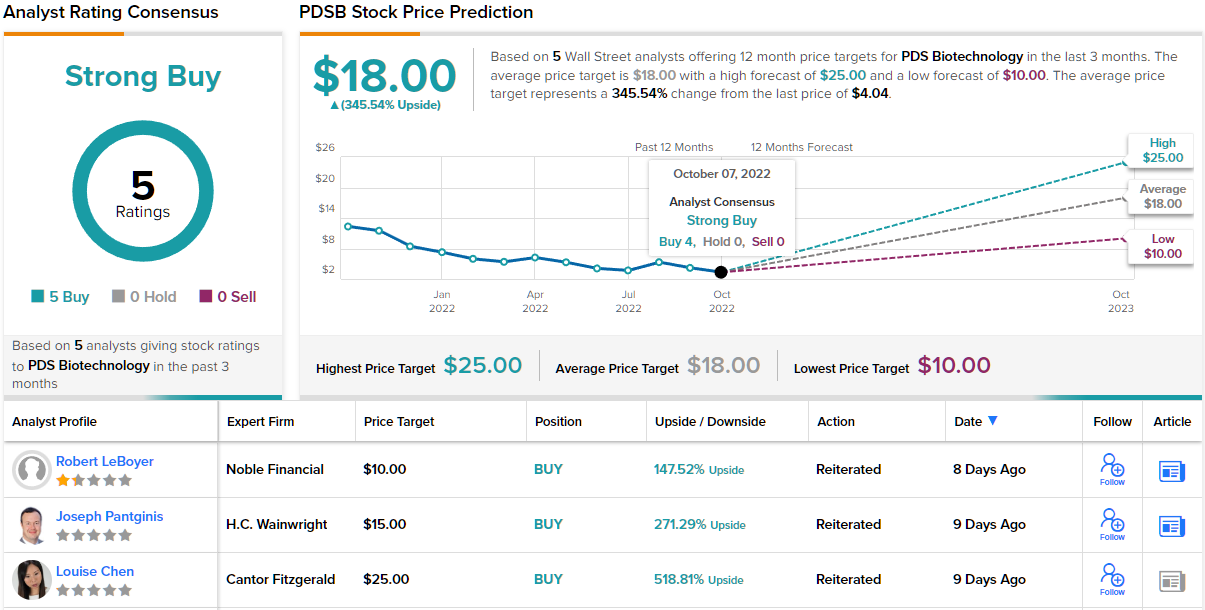

PDS Biotechnology (PDSB)

The first penny stock we’ll look at is PDS Biotechnology, an immune-oncology focused biopharma company that is working on novel methods of ‘training’ the patient’s own immune system to attack malignant tumors. The company’s Versamune platform, a proprietary technology, uses the CD8+ killer T cell to attack cancer growths. This is a more powerful type of T cell than is usually activate by immune-oncological treatments, and is designed to overwhelm the ability of tumor cells to evade or suppress attacks by T cell therapeutics. The technology also has applications in the treatment of infectious disease, which the company is pursuing using a second proprietary platform, Infectimune.

PDS currently has one leading drug candidate, PDS0101, which is being tested at the clinical stage as a combination therapy against several cancers. The chief drug used in combination with PDS0101 is Merck’s Keytruda; PDS has just completed a Phase 2 trial of this combination against HPV16-positive head and neck squamous cell carcinoma (HNSCC), and has another Phase 2 trial of the combination ongoing against various other HPV-positive cancers, including pre-metastatic HPV-associated oropharyngeal cancer (OPSCC).

On the first-mentioned track, PDS has recently announced a successful end-of-Phase 2 meeting with the FDA, which clears the way for additional clinical trials of the PDS0101/Keytruda combo against HNSCC. The company is preparing for a registrational trial to follow on the success of the Phase 2 study. The therapeutic combo was granted Fast Track status by the FDA earlier this year.

“We believe this is good news and moves the opportunity for PDS0101 forward,” Cantor analyst Louise Chen noted. “The guidance received from the FDA on key elements of the clinical will support the submission of a Biologics License Application (BLA) for PDSB’s lead asset, PDS0101. The interim safety and efficacy data PDSB presented to the FDA have allowed the company to move into a registrational trial ahead of its projected schedule.”

On the second track, against other HPV-related cancers, the company has recently announced positive interim data from a Phase 2 study conducted in conjunction with the Center for Cancer Research at the National Cancer Institute. The interim data, based on 37 patients, was consistent with earlier studies showing potential efficacy of PDS0101/Keytruda in the treatment of HPV-positive cancers.

“In our view, the expanded interim data continue to show clinical signs of efficacy, durability and safety in CPI refractory patients, who have no approved standard of care,” Chen added.

Finally, PDS is also pursuing its platform technology in the infectious disease realm, where its second drug candidate, PDS0202, in under study as a potential universal flu vaccine. In the last update on this track, pre-clinical data was showing progress in creating an efficacious preventative vaccine treatment.

Given the company’s positive clinical progress, Chen rates PDSB shares an Overweight (i.e. Buy), with a price target of $25 suggesting a powerful one-year upside of 505%. (To watch Chen’s track record, click here)

Overall, PDSB gets a Strong Buy consensus rating, based on 5 recently posted analyst reviews that are unanimously positive. The shares are trading for $4.04 and their $18 average price target implies ~345% upside in the coming year. (See PDSB stock forecast on TipRanks)

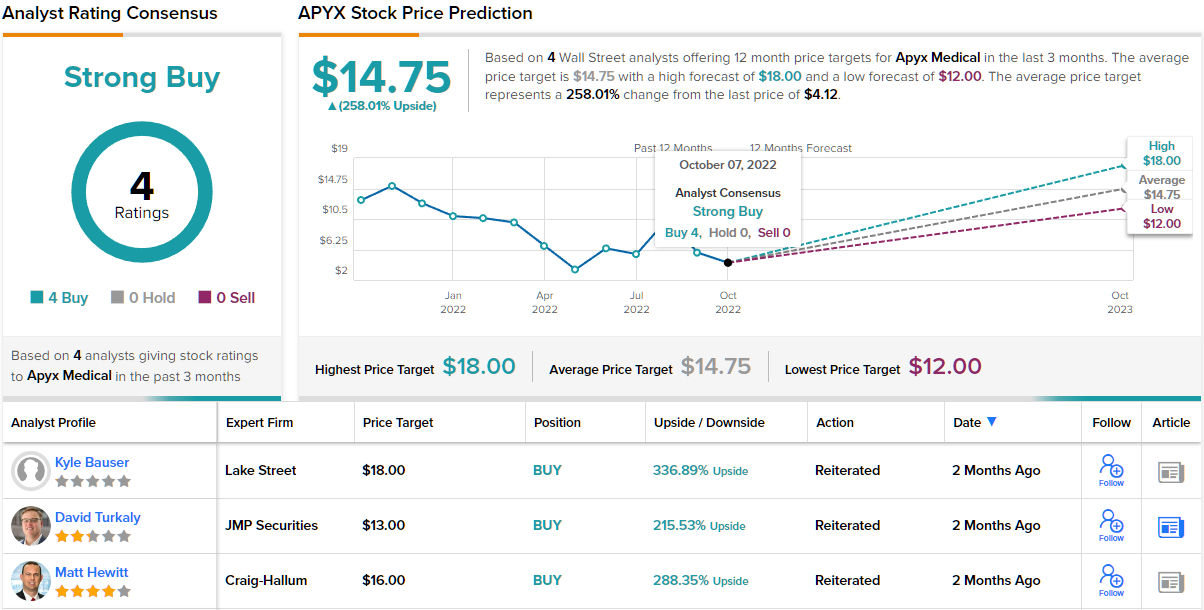

Apyx Medical Corporation (APYX)

Next up is another company in the healthcare sector – but in a different niche. Apyx Medical has developed a cosmetic surgical technology based on helium plasma, for use in tightening skin on and around the face. Apyx’s Renuvion product is the only FDA approved device for cosmetic use on loose skin of the neck and chin. The innovative technology combines helium plasma with RF energy to allow a high level of precision in cosmetic surgical procedures.

Apyx has been actively pursuing additional FDA regulatory clearances, and earlier this year announced that Renuvion device had been cleared for dermatological resurfacing procedures involving the treatment of severe wrinkles and rhytides, although limited to patients with certain specific skin types. The company is moving to increase its marketing activities based on this clearance, which it estimates may expand the patient base by over 200,000.

Like many cutting edge, tech-based firms, Apyx typically runs a net loss and can experience volatile revenue results from quarter to quarter. The company’s most recent financial release, for 2Q22, demonstrated that. The top line of $10.3 million was down 8% year-over-year, and down 38% from the peak value of $16.8 million reached in 4Q21. At the same time, the company’s OEM revenue grew 55% to $1.9 million. The net loss for the quarter was $5.4 million, giving an EPS loss of 16 cents per share. The EPS loss showed a 33% increase from the year-ago quarter.

Even though the company is experiencing some difficulty gaining traction, JMP analyst David Turkaly sees this more in the nature of ‘growing pains’ for a new, and expanding tech company. He recently wrote of Apyx: “We continue to view Renuvion as a differentiated helium-based plasma technology, which can save significant time and provide superior clinical outcomes in several large, high-growth plastic surgery markets. Additionally, with ~$20 mln in cash, Apyx should have adequate capital to: 1) support ongoing regulatory efforts; 2) increase its international footprint; 3) enhance physician and practice support worldwide (through surgeon education) in order to drive adoption; and 4) expand margins (both gross and operating, with the former driven by substantial enhancements across capital and handpieces).”

Looking forward, Turkaly adds, “In the remaining months of the year, APYX will focus on entering full commercialization for its two new clinical indications by year-end. Both indications bring 200,000 potential procedures in the U.S., which the company will begin to market to drive growth.”

Taking all of this together, Turkaly sees reason for an Outperform (i.e. Buy) rating on the stock, and his price target of $13 implies a robust one-year upside potential of ~215%. (To watch Turkaly’s track record, click here)

Turning now to the rest of the Street, other analysts are on the same page. With 5 Buys and no Holds or Sells, the word on the Street is that APYX is a Strong Buy. The shares are currently trading for $4.12 and have an average price target of $14.75, suggesting a one-year gain of 258%. (See APYX stock forecast at TipRanks.)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ ‘Top Penny Stocks to Watch’ page.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.