Which stocks are either a fan favorite or a must-avoid? Penny stocks. These tickers going for less than $5 apiece are particularly divisive on Wall Street, with those in favor as well as the naysayers laying out strong arguments.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

These names are too appealing for the risk-tolerant investor to ignore. Given the low prices, you get more for your money. On top of this, even minor share price appreciation can translate to massive percentage gains, and thus, major returns for investors.

However, there is a but here. The critics point out that there could be a reason for the bargain price tag, whether it be poor fundamentals or overpowering headwinds.

Based on the above, weeding out the long-term underperformers from the penny stocks going for gold can pose a significant challenge.

To help with the due diligence process, we’ve used TipRanks’ database to zero in on only the penny stocks that have received bullish support from the analyst community. We found two that are backed by enough analysts to earn a “Strong Buy” consensus rating. Not to mention each offers up massive upside potential, as some analysts see them climbing to $15 per share in the coming months.

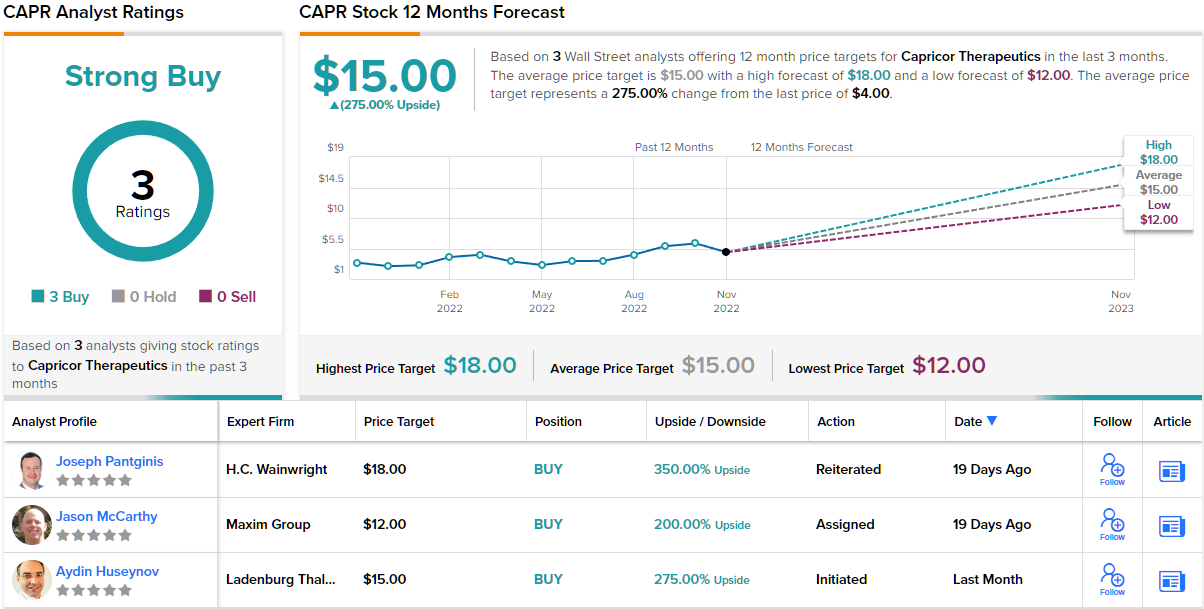

Capricor Therapeutics (CAPR)

The first stock well look at is Capricor Therapeutics, a clinical-stage biopharma company working on new treatments for Duchenne muscular dystrophy (DMD), a rare, genetically-based physical developmental disease that most commonly appears in boys around age 4. Symptoms are progressive, and patients may lose the ability to walk by age 12. Capricor is taking a cell and exosome-based approach to the development of therapeutic agents to treat, or even prevent, serious cases of DMD.

Capricor’s leading drug candidate is CAP-1002, a therapeutic agent based on cardiosphere-derived cells (CDCs), a proprietary technology of the company. The company’s CDCs have been undergoing a range of studies, including some early-stage human trials, since 2007, and some 200 DMD patients have participated. The drug candidate uses cardiac cell therapy for its demonstrated immunomodulatory activity, and CAP-1002’s trials are investigating its ability to encourage cellular regeneration.

In recent months, Capricor has presented important results from the HOPE-2 open label extension study of CAP-1002 in the treatment of patients with late-stage DMD. The results were considered positive, and resulted in statistically significant improvements in skeletal muscle function, observable by objective improvement in upper limb function. The company is currently enrolling patients in the HOPE-3 study, a Phase 3 pivotal trial on the double-blind placebo-controlled model. Capricor plans to release an interim data analysis of the HOPE-3 study in mid-2023.

Earlier this year, Capricor out-licensed the US rights for CAP-1002 to Nippon Shinyaku for a $30 million upfront fee. In addition, the company is entitled to up to $705 million in potential milestone payments, and a double-digit royalty of U.S. sales.

The company is also engaged in ongoing discussions with the FDA regarding completion and submission of a Biologics License Application (BLA) for CAP-1002. Acceptance of a BLA will be an important milestone toward later commercialization of the product.

Covering this stock for Ladenburg Thalmann, analyst Aydin Huseynov expresses his confidence in the company’s ability to capitalize on the potential of CAP-1002. He writes, “CAPR is continuing to enroll DMD patients in the HOPE-3 pivotal… In the meantime, CAPR also appears to be looking for out-licensing opportunities for CAP-1002 in ex-US territories, which may result in meaningful upfront fees. It seems CAPR wants to build a royalty/milestone model that some other platform companies have built, to focus on additional potential vaccines/therapeutics using its proprietary exosome technology.”

“It seems to us, 2023 will be a deal-rich year for CAPR, which may strengthen CAPR’s balance sheet, boost confidence in CAPR’s exosome platform, and may allow the company to raise additional equity capital for other exploratory projects… Our price target for CAPR suggests a 2-3x potential upside in case of a positive CAP-1002 readout in mid-2023 and/or an out-licensing deal for CAP-1002 ex-US. 4Q22.”

Indeed, Huseynov gives CAPR shares a Buy rating, and his $15 price target implies a robust upside potential of 275% for the coming year. (To watch Huseynov’s track record, click here)

Huseynov is not the only analyst to see a solid upside here; all three of this stock’s recent reviews are positive, for a Strong Buy consensus rating. The stock is trading for $4, and its average price target, $15, matches Huseynov’s for a 275% one-year upside potential. (See CAPR stock forecast on TipRanks)

Vor Biopharma (VOR)

The second penny stock we’ll look at, Vor Biopharma, is another clinical-stage medical research company. Vor is focused on the development of new treatments for blood cancers, treatments that will ‘change the standard of care’ for these difficult-to-treat disease conditions. The company is using engineered hematopoietic stem cells to enable precision-targeted cancer therapies for post-transplant use. The company’s goal is to protect healthy cells while exposing cancer cells to medicinal agents.

Vor currently has two main drug candidates, VOR33 and VCAR33, in multiple research tracks, including 4 pre-clinical, 1 clinical-stage, and 1 in preparation for clinical trials. VOR33, the leading candidate, is an eHSC product, created by genetically modifying healthy donor HSCs to remove the CD33 surface target. The goal is to create HSCs that are protected from the therapeutic agents post-transplant, leaving the cancer cells exposed to the targeted therapy. This candidate is the subject of a Phase 1/2 clinical trial, with initial clinical data on track for release before the end of this year. The trial has nine sites currently active, and is continuing to recruit patients.

VCAR33, the other leading candidate, is a CD33-directed chimeric antigen receptor T cell (CAR-T) therapeutic agent, under investigation as a treatment for adults with acute myeloid leukemia (AML). The drug candidate is planned as the target of a Phase 1/2 clinical trial next year, and the IND application is on track for 1H23.

In a review of Vor for JMP, analyst Silvan Tuerkcan writes: “VOR33 data are still expected in 4Q22… We remain confident in this readout based on preclinical work from several groups showing successful engraftment of edited CD33KO eHSCs and natural history data in humans with a spontaneous mutation leading to lack of CD33 in HSCs. We are also confident in the cell process, considering VOR’s CSO, Tirtha Chakraborty, Ph.D., was already involved in the successful translation of another engineered HSC that showed engraftment in humans (CTX001)… Successful engraftment would be very meaningful, in our view, validating a significant portion of the VOR approach.”

All of the above makes it clear why Tuerkcan is now standing with the bulls. The analyst rates VOR an Outperform (i.e. Buy), while his $15 price target implies an upside of ~242% for the year ahead. (To watch Tuerkcan’s track record, click here)

So, that’s JMP’s view, what does the rest of the Street make of Vor’s prospects? All are on board, as it happens. The stock has a Strong Buy consensus rating, based on a unanimous 6 Buys. VOR is selling for $4.38 and the analysts price targets average out to $20.50, for an impressive 368% upside. (See VOR stock forecast on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.