Every investor seeks to reap the rewards of their stocks; otherwise, they wouldn’t be involved in the markets. However, discovering the ideal investment, one that will yield profits, can prove to be a challenge, particularly in today’s market environment.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

To ensure solid returns, investors can follow two straightforward strategies. The first is to buy low and sell high. That is, find a cheap stock with sound fundamentals and good prospects for growth – and buy in to take advantage of the growth potential. The second strategy is to invest in dividend stocks, which provide regular payouts, allowing investors to earn returns on their investment.

Keeping these strategies in mind, we’ve used the TipRanks database to identify two stocks that offer dividends of at least 15% yield – that’s more than 7x higher than the average yield found in the markets today. Both of these stocks have received a Strong Buy rating and have positive analyst reviews on record. And all that for a cost of entry below $10. Let’s take a closer look.

Redwood Trust (RWT)

The first stock we’ll look at is Redwood Trust. This real estate investment trust, or REIT, has originally based its portfolio on residential mortgages and loans but has expanded into business purpose bridge loans. Of the $3.7 billion in Redwood’s ‘economic interest’ portfolio, 33% consists of business purpose bridge loans, 14% consists of multifamily residential developments, and 12% consists of residential jumbo securities. Since 1994, the company has been a provider of credit and financing for homebuyers.

The combination of high inflation and rising interest rates have put pressure on Redwood over the past year. Mortgage rates are now just over 7%, more than double the 3.2% average rate that prevailed early last year, and as a result, business has slowed for mortgage backers.

A look at Redwood’s last quarterly release, for 1Q23, shows the softness due to current conditions, but also some of the company’s strengths. At the top and bottom line, Redwood missed expectations in Q1. Revenues, based on net interest income, came in at $26 million, down from $53 million in the year-ago quarter and missing the forecast by almost $10.3 million. The EPS figure of 12 cents per share came in 2 cents below forecast.

Drilling down a bit, though, we find that Redwood posted an ‘earnings available for distribution’ of $14 million, a strong turnaround from the $12 million loss this metric showed at the end of December. This solid figure supported the company’s dividend payment, which was declared in March for 23 cents per common share. Redwood raised its dividend payment from mid-2020 through the end of 2021, and has held the common share dividend at its current level for the past 6 quarters. The 23-cent payment, which went out on March 31, annualizes to 92 cents and gives a hefty 15.8% yield.

Looking at Redwood for JPMorgan, 5-star analyst Richard Shane sees the company emerging from a difficult time in good shape to benefit as the interest rate climate improves. Shane writes: “We think RWT could be turning the corner. The company has cleared out substantially all of its low coupon resi inventory which should put gross margins back into positive territory. The BPL business is also achieving profitable execution again, with strong demand from investors. And with the Fed rate hike cycle nearing its end, a lot of the volatility that drove negative gross margins should be behind us.”

Going forward, Shane puts an Overweight (i.e. Buy) rating on RWT, and his price target, set at $7.50, suggests the stock will gain 29% in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~45% potential total return profile. (To watch Shane’s track record, click here)

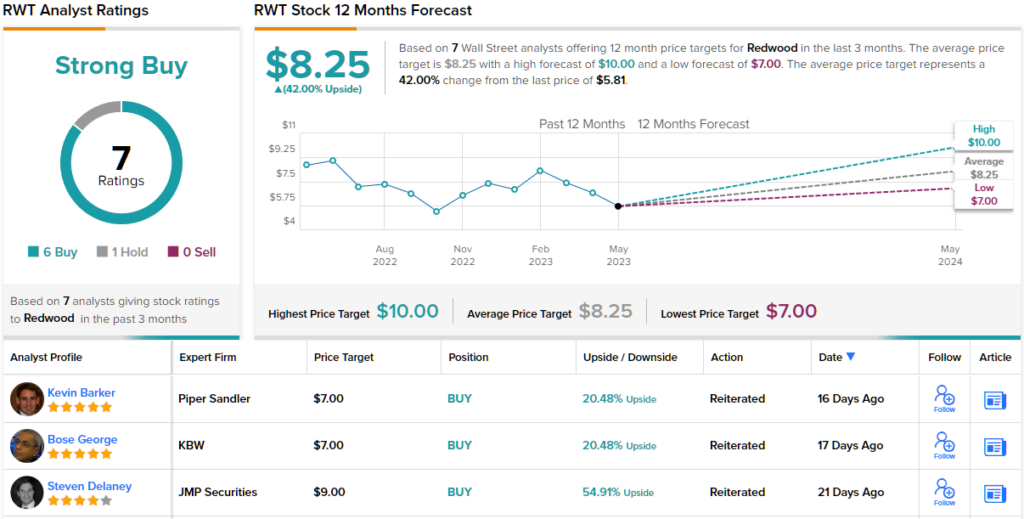

Overall, there are 7 recent analyst reviews on record for RWT shares and they break down to 6 Buys and 1 Hold, for a Strong Buy consensus view. The stock is selling for $5.81 and its $8.25 average price target suggests a potential upside of 42% in the next 12 months. (See RWT stock forecast)

Granite Point Mortgage (GPMT)

Let’s stick with REITs, and look at Granite Point Mortgage. This company is more narrowly focused than Redwood, sticking to commercial real estate mortgage loans. Granite Point’s portfolio, which is worth approximately $3.5 billion and is currently comprised of 88 loans, is made up of directly originated senior floating-rate commercial mortgage loans. Granite Point invests in and manages these assets, as well as other ‘debt and debt-like’ commercial real estate investments.

As with all REITs, Granite Point’s management team works to generate sound risk-adjusted returns for its shareholders, suitable for long-term investment. Capital return, whether through dividend payments or share purchase, is the main strategy to accomplish that, and to that end, Granite Point earlier this month announced Board authorization to repurchase 5 million shares of common stock. This authorization is on top of a previously existing share repurchase program, so the company will be repurchasing a total of 5,157,916 common stock shares in the coming year.

This does not mean that the company has set its dividend aside. On the contrary, Granite Point made its last dividend declaration in March of this year for the Q1 payment, setting the dividend at 20 cents per common share. The payment annualizes to 80 cents per share, and yields an impressively high 18%. The Q1 dividend was paid on April 17.

The company’s Q1 revenue and earnings were sufficient to support that generous dividend. For 1Q23, Granit Point reported a top line of $22.9 million, beating the forecast by $2.08 million, or about 10%. The bottom line EPS was reported as 20 cents per share – fully covering the dividend – and was 5 cents ahead of expectations. The company also had $220 million in available liquid assets as of the end of Q1, and the firm’s book value was reported at $14.08 per common share.

For 5-star analyst Stephen Laws, of Raymond James, this all adds up to a stock worth buying. Laws rates the shares an Outperform (i.e. Buy), with a $7 price target that implies a 58% gain going out to the one-year time horizon. (To watch Laws’ track record, click here)

Supporting this outlook, Laws writes, “Our price target is based on shares trading at ~50% of book value. We believe our multiple is appropriate given the diversified portfolio, attractive loan portfolio characteristics, our portfolio return estimates, and expectation the dividend is maintained, while considering macro concerns around commercial real estate and sector headwinds that are likely to persist for some time.”

Overall, Granite Point has earned a Strong Buy consensus rating from the Street’s analysts, based on 3 unanimously positive reviews filed in recent weeks. The stock’s $4.42 trading price and $7.67 average share price combine to suggest a robust 73.5% upside potential, even more bullish than Laws would allow. (See GPMT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.