With most semiconductor stocks set to report earnings at the end of the month, investors are already bracing for poor results. Yet, there are some companies in the space whose strong backlogs and momentum place them in a better position. Two such names are Microchip Technology Inc. (NASDAQ: MCHP) and Monolithic Power Systems (NASDAQ: MPWR), which also appear to be relatively reasonably valued. I am bullish on both stocks.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

While semiconductors are essential components of any electronic device, the demand for electronic devices is cyclical. Thus, the semiconductor industry is also quite cyclical. During favorable market environments, high demand for semiconductors leads to supply shortages. Naturally, this leads to tight supply and high prices, which is usually followed by inventory buildup and falling prices during unfavorable economic periods. For this reason, semiconductor stocks are particularly notorious for their cyclical nature.

Undoubtedly, the market is not in its best shape right now, and with the ongoing macroeconomic unrest pressuring consumer spending and corporate CapEx, demand for semiconductors is entering a downcycle.

Advanced Micro Devices (NASDAQ: AMD), whose performance can function as a bellwether to the industry due to its significance in the market, released its preliminary results last Friday. The company massively disappointed investors as its numbers came in way below consensus estimates, which resulted in its shares plunging further.

Nonetheless, as mentioned above, MCHP and MPWR are well-positioned to navigate current market conditions. Let’s examine why.

Strong Backlogs & Momentum to Drive Revenues

MCHP and MPWR benefit from strong backlogs and momentum, respectively, which should result in a “softer landing,” if not continuous growth, moving forward. I find these to be strong traits in the semiconductor space currently.

MCHP’s Latest Earnings Results Showed Strong Growth

MCHP’s latest results demonstrated this. In its Fiscal Q1-2023 results, the company reported record net sales of $1.96 billion, up 25.1% from the comparable period last year. Revenues grew 6.5% sequentially as well, reflecting its strong momentum.

In the earnings report, MCHP’s CEO, Mr. Moorthy, mentioned that the company ended the quarter with its highest unsupported backlog ever, with well over 50% of this backlog being non-cancelable under MCHP’s Preferred Supply Program (PSP).

He also highlighted that due to MCHP’s unsupported backlog being well ahead of the actual revenue the company achieved in Q1, management believes MCHP is well-positioned to continue to propel incremental revenue growth and profitability. The keyword here is “incremental,” as it doesn’t only imply positive year-over-year growth but actually sequential revenue growth on top of fiscal Q1’s record numbers.

MPWR’s Latest Earnings Results Were Also Strong

MPWR’s latest results also showcased robust growth momentum in fiscal Q2, and based on management’s guidance, the pace will persist, moving forward. Quarterly revenues rose by 57.2% year-over-year to $461 million, driven by the company’s diversified growth strategy, technological innovation, and broad-based market share gains.

Impressively, Storage and Computing revenues skyrocketed by 112% to $122.3 million, while Enterprise Data revenues leaped to $65.2 million, a gain of 118% versus the prior-year period. The rest of its segments also delivered exceptionally-high growth rates.

However, since we are mostly interested in the company’s forward-looking growth, management expects that Q3 revenues will be in the range of $480 million to $500 million. This implies year-over-year growth of 51.7% at the midpoint, which implies little to no slowdown from Q2’s revenue growth.

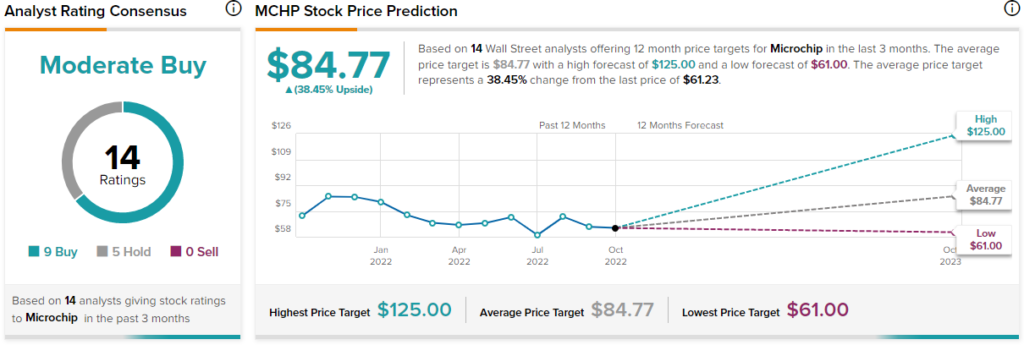

Is MCHP Stock a Buy, According to Analysts?

Turning to Wall Street, Microchip Technology has a Moderate Buy consensus rating based on nine buys and five Holds assigned in the past three months. At $84.77, the average MCHP stock forecast implies around 32.8% upside potential.

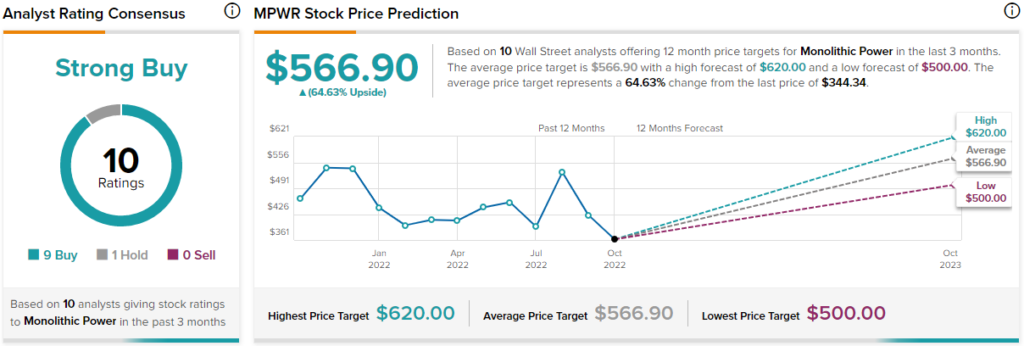

Is MPWR Stock a Buy, According to Analysts?

Turning to Wall Street, MPWR has a Strong Buy consensus rating based on nine buys and one Hold assigned in the past three months. At $566.90, the average MPWR stock forecast implies around 64.6% upside potential.

Are MCHP & MPWR Reasonably Valued?

While both MCHP and MPWR are set to report robust revenue growth this year, they are also set to grow their net income quite substantially. MPWR is set to grow its adjusted EPS by nearly 69% to $12.58. MCHP is expected to grow its adjusted EPS by nearly 23% to $5.66. These figures imply that the stocks trade at forward P/E ratios of 27.4x and 10.8x, respectively. MPWR’s more elevated multiple likely reflects the company’s more explosive growth rates. Overall, I would say that when taking into account both companies’ forward expectations, both stocks appear reasonably valued.

MCHP likely offers a higher margin of safety due to its humbler valuation multiple and higher cash flow visibility amid its backlog.

I highly suggest that prospective investors review MCHP’s and MPWR’s stock-based compensation expenses regularly, as they are often high, nonetheless. This is common in the industry to retain talent, but it can seriously dilute investors over the long run. For context, MCHP’s and MPWR’s shares counts have expanded by 34.8% and 31.9% over the past decade. Consistent dilution, in turn, means that the current valuation multiples could be somewhat warped.