The tech-heavy Nasdaq represents a collection of more risky stocks than the other major indexes and that is reflected by a poorer performance in bear markets and a better display during bull runs.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But the risks associated with the Nasdaq are mere child play compared to edgier funds such as Cathie Wood’s Ark Innovation ETF. Now that really hit the skids during last year’s bear, but the fund is also up 37% year-to-date, putting the Nasdaq’s 15% gain in the shade.

In fact, throwing more shade the Nasdaq’s way, after January represented its best ever monthly performance, Wood recently said the ARKK ETF is “the new Nasdaq,” and offers investors much better exposure to the disruptive stocks she supports.

So, let’s go down that route and dig up the details on a pair of disruptive, high-risk, high-reward names the Ark CEO has been loading up on in recent times. Using the TipRanks database, we can see whether the Street’s analysts are also backing Wood’s picks. Here are the details.

Verve Therapeutics, Inc. (VERV)

The first Cathie Wood pick we’re looking at is Verve Therapeutics, a biotech company with one mission: to offer protection against cardiovascular disease. This it intends to do by developing medicines using cutting edge techniques — human genetic analysis, gene editing, messenger RNA (mRNA)-based therapies and lipid nanoparticle (LNP) delivery — to realize its vision and disrupt the present care model by which cardiovascular disease is treated.

Verve’s pipeline has two programs still in the early stages of development. Leading the way is VERVE-101, designed as a single-course in vivo liver gene editing therapy and initially intended to treat heterozygous familial hypercholesterolemia (HeFH), an autosomal dominant disease defined by noticeably raised plasma concentrations of low-density lipoprotein (LDL) cholesterol (LDL-C).

The program, however, has run into some issues. In November, the FDA placed a clinical hold on the company’s Investigational New Drug application (IND) for the candidate, citing the need for more clinical and preclinical data plus a modification to a U.S. study.

Nevertheless, a Phase 1 study for VERVE-101 titled heart-1 is currently taking place in New Zealand and the U.K. An early data readout from the dose-escalation portion is anticipated in H2 2023.

Cathie Wood is evidently not too concerned about the clinical hold; she bought 691,589 shares via ARKK over the past two months. The ETF now holds 1,534,882 VERV shares in total – amounting to more than $35 million at the current share price.

Mirroring Wood’s confidence, and reflecting its high-risk/high-reward status, Stifel analyst Dae Gon Ha calls Verve a “wildcard,” but still considers the stock a “top pick.”

“We believe VERVE-101’s (heterozygous familial hypercholesterolemia [HeFH]) clinical hold can be resolved (timing TBD) – which can drive shares higher – but regardless, Ph.1 heart-1 data (2H23) has a high likelihood of generating positive data – which can also drive shares higher. With a potential stock support at ~$19/shr, we think 2023 could claw back some of the 2022 losses. We expect investor pushback on the commercial viability to continue for VERVE-101 but do not see it as a major hindrance to the stock’s performance,” Ha opined.

Overall, Ha thinks the stock has some way to go, and by some way, we mean 140% of upside. Those are the returns investors are looking at, should the stock make it all the way to Ha’s $56 price target. No need to add, the analyst’s rating is a Buy. (To watch Ha’s track record, click here)

Most agree with Ha’s bullish stance. Based on 6 Buys, and 1 Hold and Sell each, VERV has a Moderate Buy consensus rating. All in all, the analysts expect shares to appreciate by 69%, as indicated by the $39.43 average price target. (See VERV stock forecast)

Intellia Therapeutics, Inc. (NTLA)

We’ll stay in the biotech space for the next Wood-backed stock. Using CRISPR-based technologies, Intellia Therapeutics’ goal is to develop genome editing treatments for people suffering from serious diseases. In fact, one of Intellia’s co-founders, Jennifer Doudna, was part of the team that invented the CRISPR gene editing system – a genetic engineering method in molecular biology whereby the genomes of living organisms may be altered – and along with Emmanuelle Charpentier, was awarded the 2020 Nobel Prize in Chemistry for the groundbreaking CRISPER work.

Last year, Intellia reported positive interim data from two ongoing clinical studies assessing the company’s in vivo CRISPR/Cas9 gene editing treatments; one is from the study of NTLA-2001, indicated to treat patients with ATTR (transthyretin amyloidosis) – a collaboration with Regeneron Pharmaceuticals – and the other for NTLA-2002 in hereditary angioedema (HAE).

For the former, the company plans on releasing more clinical data from the ongoing Phase 1 study of NTLA-2001 in 2023 and intends to file an IND application around mid-year to allow for the inclusion of U.S. sites in a pivotal study of the candidate.

As for NTLA-2002, the company plans to kick off the Phase 2 segment of the ongoing Phase 1/2 study during the first half of the year. An IND to get U.S. sites included in the Phase 2 study of NTLA-2002 should also be submitted during 1H.

Despite a recent uptick, the stock has severely underperformed over the past year, having shed 54% of its value. Wood evidently thinks now is the time to pounce; over the past two months, via ARKK, she purchased 181,295 shares, bringing the ETF’s total holdings to 6,744,252 shares. These are currently worth more than $291 million.

Sharing Wood’s enthusiasm, Wells Fargo’s Yanan Zhu likes the look of the shares right now and assuages investor fears on specific issues.

“We see NTLA shares as attractively valued at current price, and would note that concerns on U.S. IND filing and approval as well as on safety of the company’s in vivo gene editing programs, although understandable, are greatly overdone,” the analyst wrote. “In 2023, we see high likelihood of FDA allowing INDs for NTLA’s and other companies’ in vivo gene editing studies. Our confidence is based on FDA’s previous clearance of zinc finger nuclease (ZFN)-based gene editing INDs. We also note that the accumulation of safety data from ex-US studies of in vivo CRISPR gene editing studies could also facilitate FDA’s decision.”

Backing that stance, Zhu rates NTLA shares an Overweight (i.e. Buy) to go alongside a $120 price target. This target brings the upside potential to a whooping 177%. (To watch Zhu’s track record, click here)

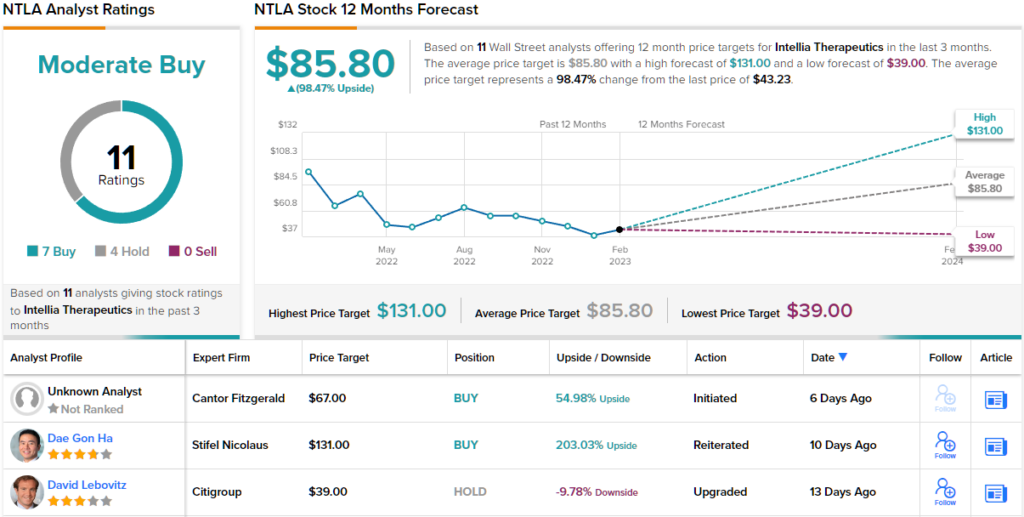

Looking at the consensus breakdown, based on 7 Buy ratings vs. 4 Holds, this stock claims a Moderate Buy consensus rating. The analysts see the shares delivering returns of ~98% over the coming year, considering the average target clocks in at $85.80. (See Intellia stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.