Lately, I have been sharing investment ideas that incorporate non-cyclical business models, extended dividend-growth track records, attractive yields, and evidence of strong cash-flow generation during market downturns. I believe that these characteristics can increase investors’ margin of safety during the highly-uncertain market landscape and enhance the predictability of one’s future total-return projections. Boasting 45 and 50 years of consecutive annual dividend hikes, The Clorox Company (NYSE: CLX) and Kimberly-Clark Corporation (NYSE: KMB) meet these criteria.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

This is due to their household and personal care products enjoying stable demand, a great trait during the current highly-inflationary environment.

My concern, however, is that both companies appear significantly overvalued, while their dividend-growth prospects are uninspiring. Thus, their future total-return prospects could be limited or even negative following a valuation multiple compression.

Accordingly, I am neutral on both CLX and KMB stock.

Inspecting CLX’s & KMB’s Dividend Prospects

Both CLX’s and KMB’s investment cases revolve around their dividend since they feature little to no growth prospects. Specifically, CLX and KMB feature 10-year revenue compound annual growth rates of 2.7% and -0.7%, respectively. Their earnings-per-share CAGRs over the same period stand at -0.9% and 3.0% as well. These numbers showcase their mature operations and rather stagnant industries they operate in.

Therefore, to evaluate whether CLX or KMB are worth investing in, we are going to review whether investors can count on their dividends and what dividend-growth pace one should expect.

CLX’s latest dividend hike occurred back in July and was by a rather disappointing 1.7% to a quarterly rate of $1.18. In the case of KMB, the company last hiked its dividend by 1.8% to a quarterly rate of $1.16, which is an equally disappointing growth rate.

This theme is not coincidental. In fact, over the past decade, both companies have been gradually decelerating the pace of their dividend increase in the face of stagnated earnings. Otherwise, their payout ratios would grow unsustainable.

In fact, this is already appearing to be becoming the case. With both companies raising their dividends against static earnings, their payout ratios grew increasingly alarming.

CLX’s guidance for Fiscal 2023 targets adjusted earnings-per-share to be between $3.85 and $4.22. Even if we assume that the company will deliver on the higher end of this range (e.g., $4.20), this implies another year of stagnated earnings and a payout ratio of 112%. Consensus earnings-per-share estimates for KMB’s Fiscal 2022 also hover at $5.63, implying an 8.9% decline year-over-year and a payout ratio of 82.4%.

Consequently, I would say that while both CLX and KMB are likely to continue producing resilient revenues and profits during the ongoing market downturn, investors shouldn’t expect meaningful dividend growth, moving forward. This is especially the case regarding CLX’s future dividend hikes, which are likely to remain below 2% as management likely anticipates earnings-per-share growth to catch up to the dividend.

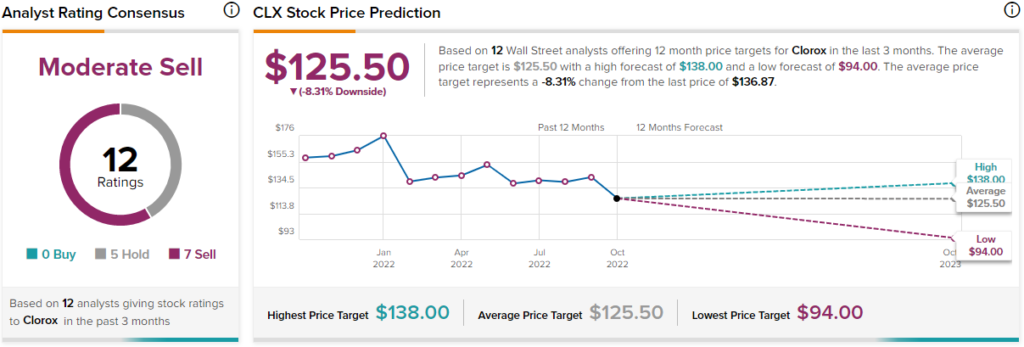

What is the Target Price for CLX Stock?

As far as Wall Street’s sentiment goes, Clorox has a Moderate Sell consensus rating based on five Holds and seven Sells assigned in the past three months. At $125.50, the average Clorox stock forecast implies 8.3% downside potential.

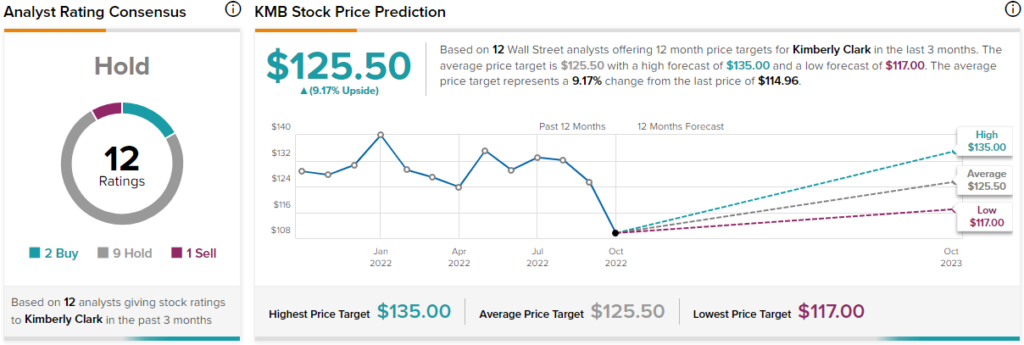

What is the Target Price for KMB Stock?

In the case of Kimberly-Clark Corporation, the stock has a Hold consensus rating based on two Buys, nine Holds, and one Sell assigned in the past three months. At $125.50, the average Kimberly-Clark stock forecast implies 9.17% upside potential.

Are CLX & KMB Reasonably Valued?

Use any valuation metric and apply any approach you believe is most accurate, and you will quickly find out that both CLX and KMB are, unfortunately, quite overvalued. Despite the two companies featuring stagnated earnings-per-share over the past decade, their P/E multiples expanded significantly during this period.

Specifically, over the past decade, CLX’s and KMB’s forward P/Es expanded from the low teens to 33.3x and 20.6x, respectively. You could maybe justify expanding multiples when rates were hovering near 0%, but you most certainly cannot justify these multiples during the current rising-rates environment.

Further, while CLX’s and KMB’s dividend yields of 3.5% and 4.0% are somewhat substantial, they are not enough to adequately compete with T-bills. Investors should require a higher equity risk premium to have a sufficient margin of safety.

Conclusion: Are CLX & KMB Worth Buying for Their Dividends?

The short answer is no. CLX and KMB are not worth buying solely for their dividends. Don’t get me wrong, both companies are not going anywhere. Their products will continue to be utilized by millions of people every day, and profitability should remain rock-solid.

However, this is one of those cases that can deceive investors due to the admittedly excellent dividend-growth track records. You should also not ignore the underlying concerns regarding the growth prospects of said dividends, as well as the multiple compression risks attached to such elevated valuation levels.