Do you love dividends? Of course you do — and rightly so!

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Scholars who study the stock market’s historical performance estimate that over time, the payment (and reinvestment, and compounding) of dividends have contributed anywhere from 30% to 90% of the S&P 500’s total returns. Simply put, if you’re not investing in dividend stocks, you’re doing it wrong.

Using the TipRanks platform, we’ve looked up two stocks that are offering dividends of at least 12% yield – that’s almost 7x higher the average yield found in the markets today, and best of all, they all offer investors a low cost of entry, under $10 per share. Let’s take a closer look.

Seven Hills Realty Trust (SEVN)

We’ll start with Seven Hill Realty Trust, a real estate finance company operating as a real estate investment trust (REIT) with a focus on middle market and transitional commercial real estate in the US markets. In short, Seven originates and invests in first mortgage commercial real estate loans. The company’s portfolio boasts $727.5 million in total loan commitments, with an average weighted maximum maturity of 3.3 years. Seven currently holds approximately $37 billion in total assets under management.

Like most firms operating in the REIT universe, Seven has a substantial history of reliable dividend payments, going back to 2012 – with a total history of dividends stretching back to 2007. Like its niche peers, Seven’s dividend policies are impacted by governmental regulations that require a certain percentage of profits to be returned directly to shareholders each year; dividend make a convenient mode of compliance, and the result is, usually, a reliable payment and a high yield.

In Seven’s case, the dividends are supported by income numbers that are currently showing mixed year-over-year results. In the last quarter reported, 4Q22, the company derived its earnings from a top line of $9.3 million, which came in below the $10.5 million forecast. The adjusted distributable earnings, an important metric for dividend investors, came in at $5.37 million, for a 76% y/y gain; on a per share basis, the adjusted distributable earnings came in at 37 cents per common share, beating the forecast by 48% and also representing an increase of 76% year-over-year.

The strong gains in distributable earnings gave management confidence, and back in January Seven boosted its quarterly dividend by 40%. The same day of that announcement, the shares jumped 15%.

In Seven’s last dividend declaration, scheduled for a May 18 payment, the company kept the raised dividend of 35 cents per common share. At the annualized rate of $1.40 per share, the dividend is currently yielding a sky-high 14%.

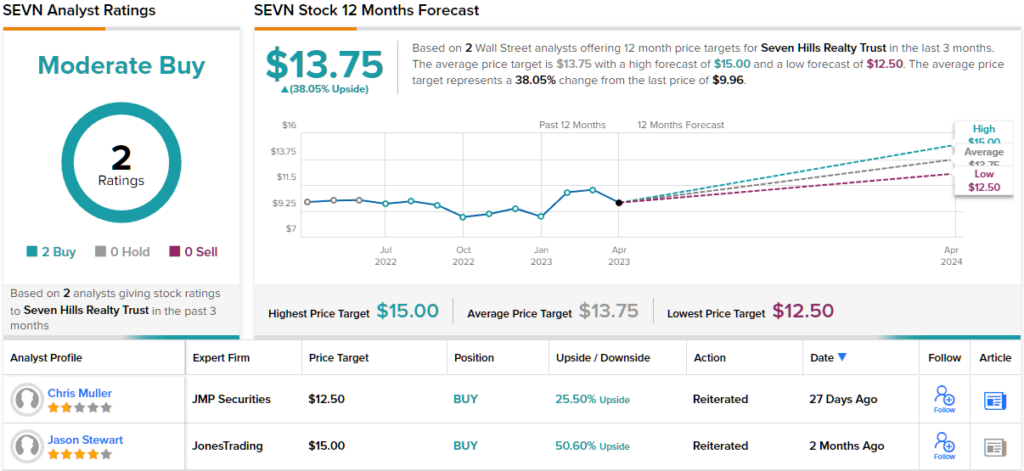

In the eyes of JMP analyst Chris Muller, all of this adds up to a stock that deserves a second look. Muller takes special note of the current interest rate regime in his comments, writing: “Our new model reflects our March 2023 interest rate forecast, which projects YE23/YE24 one-month LIBOR rates of 4.55%/3.50%. We have modeled the quarterly dividend staying at the newly increased level of $0.35 per share through 2024… With SEVN shares now trading at just 0.55x December 31 GAAP BV of $18.46, we believe the current discount to book value is unwarranted given the growth in earning assets, a tailwind from rising interest rates, and potential for further meaningful dividend growth.”

Quantifying his stance, Muller gives SEVN shares an Outperform (i.e. Buy) rating, with a $12.50 price target that indicates potential for a 26% one-year upside potential. Based on the current dividend yield and the expected price appreciation, the stock has ~40% potential total return profile. (To watch Muller’s track record, click here)

Zooming out, we find that SEVN gets a Moderate Buy rating from the analyst consensus, based on 2 recent positive reviews on file. The shares are trading for $9.91, and their average price target, standing at $13.75, implies 38% gain out to the one-year horizon. (See SEVN stock forecast)

Rithm Capital (RITM)

For the second stock on our list, we’ll turn to Rithm Capital, another REIT, operating as an internally-managed firm. The company has operations at ‘both ends’ of its business, both in mortgage loan origination and in mortgage servicing rights (MSRs). Rithm’s investment portfolio leans heavily toward the servicing end, with 44% composed of mortgage servicing, and another 29% composed of MSR-related investment. Another 8% of the portfolio is mortgage loans receivable, and 5% is listed as origination, or original mortgage loans. The remainder of the portfolio is made up of real estate securities and properties and residential mortgage loans.

A look at some of the company’s basic numbers gives an idea of Rithm’s quality. The company has approximately $32 billion in total assets, including $8.89 billion in MSR and related assets. Rithm could boast some 3 million customers as of the end of 2022. The company was formed through a restructuring in the summer of 2021, and since that time it has paid out more than $4.4 billion in dividends to its investors.

The dividends that Rithm pays out are supported by a solid base of earnings available for distribution, totaling $156.9 million as of the end of 4Q22. This was a non-GAAP result, coming to 33 cents per share, 4 cents better than had been predicted. The earnings for distribution showed a modest increase from 3Q22’s $153 million and 32 cents per share. Rithm’s total revenue in Q4, at $762.4 million, was $12.3 million better than the expectations.

Based on the Q4 earnings, Rithm declared a 25 cent dividend per common share, to be paid out on April 28. The $1 annualized payment gives the dividend an impressive yield of 12.6%, and marks the seventh quarter in a row with the dividend at this level. Rithm paid out $118.6 million in total dividends in Q4, and $470.4 million in 2022 as a whole. The total dividends paid in 2022 were up 14.8% year-over-year.

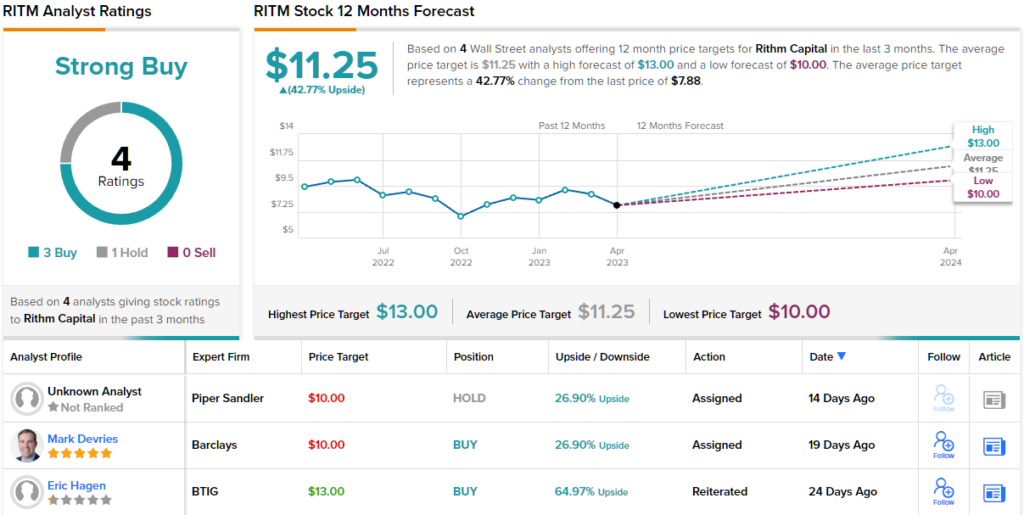

In his coverage of this Rithm for BTIG, analyst Eric Hagen is impressed by the company’s ability to keep its stable dividend, and notes that the MSRs in the portfolio show plenty of potential for maintaining the earnings base.

“We like the stock here in part because we see dividend stability mostly being a function of slow prepays in the MSR portfolio, and less conditioned on the origination segment returning to profitability in the near term. We expect MSR valuations are still finding some support from higher short-term interest rates, although to that end, we think growing expectations for the Fed to cut rates later this year could limit some upside potential for servicing valuations. Roughly half of the company’s capital is in the MSR portfolio, but with the leverage it has there, we estimate it drives closer to 60-75% of core earnings,” Hagen opined.

Hagen’s analysis indicates that RITM shares are worth buying, with a price target of $13 that implies a substantial 64% upside over the next year. (To watch Hagen’s track record, click here)

Overall, there are 4 recent analyst reviews of this stock on file, and they include 3 Buys against a single Hold, for a Strong Buy consensus rating. The stock is selling for $7.89, and its $11.25 average price target suggests it will grow ~43% by year’s end. (See RITM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.