It’s official, retail investors have re-entered the market, bidding up growth stocks, and two widely discussed stocks include Fiverr (NYSE:FVRR) and Wix.com (NASDAQ:WIX). However, the question beckons: should investors be lured into the hype?

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Investing into the hype can often result in lucrative gains if executed effectively. In fact, taking advantage of what is known as the “momentum anomaly” is a proven investment strategy executed by some of Wall Street’s finest investors. Nevertheless, it needs to be detected whether discussions surrounding popular stocks hold substance or if they are pure noise.

I discovered value in abundance after thoroughly analyzing Fiverr and Wix.com’s prospects. Here are a few factors to consider.

Fiverr (FVRR)

To say that Fiverr’s stock has surged since the turn of the year is an understatement, as its more than 38% year-to-date return is unparalleled by most. Yet, key variables imply that the stock’s scintillating run is far from over.

Fiverr’s fourth-quarter earnings report surfaced on Wednesday, which revealed an earnings-per-share beat of eight cents ($0.26 EPS vs. $0.18 consensus). More crucially, Fiverr’s management initiated a favorable outlook, eclipsing the broader consensus by stating that the firm may reach revenue of $88.5 million in 2023.

A more detailed look at Fiverr’s quarterly earnings report conveys robust organic growth, as the company’s spend per buyer has increased by 8% year-over-year, which is considered encouraging, given last year’s macroeconomic headwinds. In addition to resilient customer spending, Fiverr’s third-party revenue increased year-over-year as take rates reached 30.2% versus a previous 29.2%.

Much of Fiverr’s operational success is due to its substantial market share in the freelance market, which was projected to grow by an annual rate of 15.3% from 2021 until 2026. As such, investors will likely price in the probability that Fiverr’s operating cash flow is going to proliferate in the coming years.

Furthermore, the company’s EBITDA (earnings before interest tax depreciation and amortization) is anticipated to settle between $45 to $55 million in 2023, surpassing the initial estimated value of $37 million.

Fiverr’s significant EBITDA improvement might be priced in by many investors who now spot an opportunity amid improved cost management by the company. According to Fiverr’s CEO, Micha Kaufmann, the company’s enhanced profit and loss outlook is due to both an improved macroeconomic environment and an idiosyncratic focus on efficiency by Fiverr.

In Kaufmann’s own words, “With a shift in the macro environment and SMB spending sentiment, we quickly adjusted our business focus to drive efficiency, which is reflected in us delivering the most profitable quarter in the company’s history in terms of Adjusted EBITDA.”

In terms of valuation, Fiverr’s price multiples are a cause for concern (it has a price-to-cash-flow ratio of 49x), especially if another market downturn had to surface. This is because growth stocks are more susceptible to challenging macroeconomic environments than value stocks. As such, investors must consider Fiverr’s stock in cohesion with the broader market outlook.

Is FVRR Stock a Buy, According to Analysts?

Turning to Wall Street, Fiverr earns a Moderate Buy consensus rating based on six Buys and four Holds assigned in the past three months. The average FVRR stock price target of $49.70 suggests 25.5% upside potential is in the cards.

Wix.com (WIX)

Wix possesses proximities to Fiverr. For example, Wix is also a growth stock. Additionally, as is the case with Fiverr, Wix recently posted incredible financial results, illustrating an enhanced year-over-year trajectory.

A detailed look at Wix’s fourth-quarter earnings beat reveals that the company has demonstrated continued success with a business model suitable to modern commerce.

According to its fourth-quarter report, Wix’s headline revenue grew by 6% year-over-year amid growth in subscriptions, which are now anticipated to reach a gross profit margin of 80% by the end of 2023. As a matter of fact, Wix’s subscription-based revenue has increased in quality as the segment’s deferred revenue has shrunk considerably during the past year. Consequently, this resulted in an improved credit outlook.

Wix faces close competition from Shopify (NYSE:SHOP) and has a mountain to climb before it nears WordPress in market share. Nonetheless, the website builder market is growing steeply at an expected compound annual growth rate of 7.1% from 2022 to 2030. On top of that, an inward look provides a sense of encouragement to Wix’s investors, as the firm has expanded its market share to 3.6% from a mere 0.6% in 2017.

Furthermore, Wix’s Solutions and Bookings segment saw 3% year-over-year growth. The firm’s Business Solutions segment is naturally more volatile than its Subscriptions segment, as the division’s offerings include “nice to haves” instead of staple website solutions. Nonetheless, the unit’s performance could surge in the coming years as factors such as an improved macroeconomic outlook, growing demand for corporate digitalization, and a wider variety of marketplace offerings might all play a role.

Even though WIX stock is arguably overvalued, with a price-to-sales ratio of 3.8x compared to the sector median of 2.7x, market participants seem to emphasize the stock’s growth story more than its valuation multiples.

For example, hedge funds are currently net bullish on WIX stock, as the latest 13-F filings indicate that these funds added 81,200 Wix shares to their portfolios in the past three months.

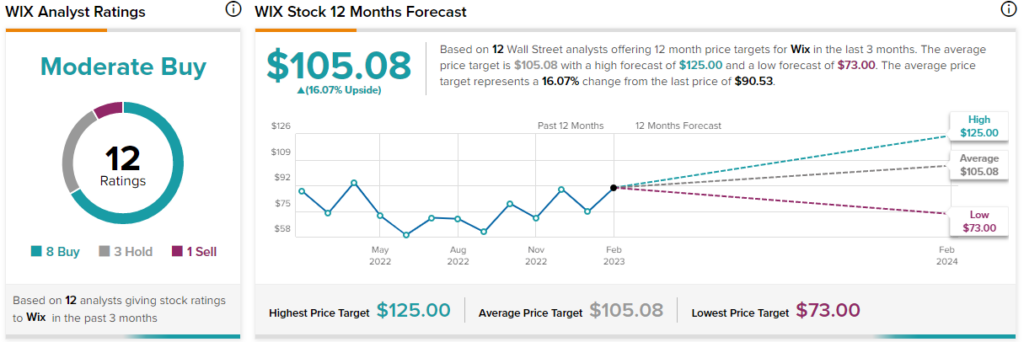

Is WIX Stock a Buy, Hold, or Sell?

Turning to Wall Street, Wix.com earns a Moderate Buy consensus rating based on eight Buys, three Holds, and one Sell assigned in the past three months. The average WIX stock price target of $105.08 suggests 16.1% upside is probable.

Concluding Thoughts

Retail investors are back at it again, meaning high beta technology stocks are in popular demand. Fiverr and Wix are two of the most-widely-discussed stocks among investors, and their prospects are alluring due to their robust fundamentals.

Although Fivver and Wix lack relative value, their growth stories are supported by continuously improving financial results, indicating that they are “best-in-class” picks in today’s market environment.