With the S&P 500 (SPX) beginning to sour again, many bearish pundits have doubled down on their calls for more pain. Undoubtedly, things could go either way from here as a recession looms.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Eventually, stocks will turn a tide, and it’s the hardest-hit, risk-on plays that could have the most to gain. Until then, a more balanced approach may be the way to go, as it’s clear that many market participants aren’t yet done worrying about inflation and more Fed rate hikes.

With fast-food stocks, you don’t have to worry about what other investors are worried about or how much recent economic data hit or missed the mark. As inflation and economic headwinds take a toll, it’s the quick-serve restaurant companies with best-value offerings that could fare well as the economy takes a few steps back in 2023.

Fast-food stocks may not be cheap, given investors have had plenty of time to rush into the defensives. Regardless, the following two names — MCD and CMG — have the confidence of Wall Street, so let’s compare them.

McDonald’s (NYSE:MCD)

McDonald’s is the fast-food giant that’s held its own incredibly well through 2022. Over the past year, shares are up around 16.7% — a solid gain, given the bear market that clawed down broader markets for most of 2022. I am bullish on MCD.

Looking ahead, I expect continued resilience from McDonald’s as it continues to execute under top boss Chris Kempczinski. He’s not only proven himself as an effective manager, but he’s helped make McDonald’s compelling again through the eyes of younger consumers. With new menu items (the McCrispy chicken sandwich) and celebrity-endorsed meals, McDonald’s remains “cool” even with all the new up-and-coming players in the fast-food scene.

It’s not just innovation and new menu items that could help the growth at McDonald’s going. The international licensee segment also appears like a promising long-term growth driver.

It’s no mystery that many firms across numerous industries are looking to China to bolster their growth rates. McDonald’s is well-equipped to benefit from China’s rapidly-ascending middle class. With strategic partners in place to help mitigate risks and provide expertise in local markets, I view McDonald’s as one of the most prudent ways to play a Chinese expansion.

Unlike in the U.S., McDonald’s can’t replicate its real estate-focused model in China due to regulatory hurdles, but that doesn’t mean McDonald’s can’t get more skin in the game.

With numerous partners in place, McDonald’s can reap the rewards from growth in China while getting help managing the sizeable risks that come with operating within the region.

Undoubtedly, expanding into new markets accompanies can be a risky, expensive endeavor. Such risks are better managed by McDonald’s Chinese partners, who are more familiar with operating and growing within the Chinese market.

At 32.1 times trailing earnings, MCD stock is historically pricy. Still, I think the multiple is well-deserved. It’s hard to find a company that can grow (by mid-to-high single digits) as the economy stalls out.

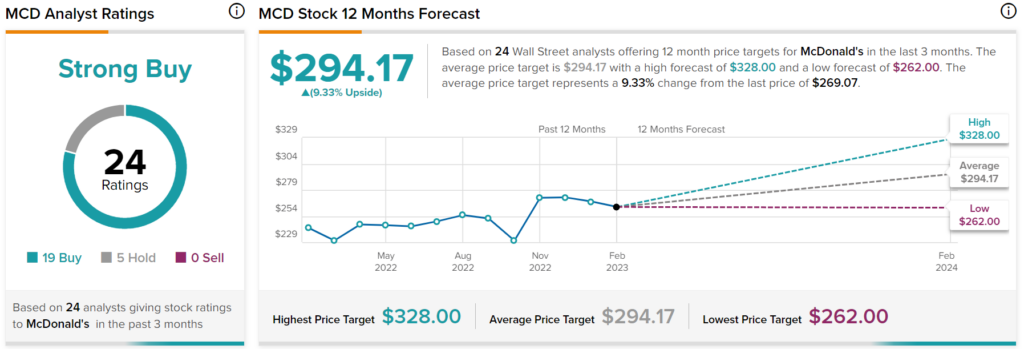

What is the Price Target for MCD Stock?

Wall Street loves McDonald’s in this risk-on environment, with a “Strong Buy” consensus comprised of 19 Buys and five Holds. The average MCD stock price target of $294.17 implies 9.3% upside potential from here.

Chipotle Mexican Grill (NYSE:CMG)

Chipotle is one of the quick-serve restaurant chains that’s really hit the spot with young and health-conscious consumers. Fresh ingredients and tasty new offerings (so-called “food with integrity”) have kept the lines long over at the local Chipotle, even amid inflation. Undoubtedly, Chipotle has been the growth play to play the industry. I am bullish on CMG.

Still, with rates rising, investors aren’t nearly as keen to overpay for growth stocks anymore. Further, Chipotle doesn’t seem like the most recession-resilient way to play the space, given its offerings tend to be much pricier than the likes of rivals like McDonald’s. As the year progresses and a recession “lands,” we’ll get a gauge of just how much pricing power the firm has. My guess is lines will shorten as consumers opt to save money with superior value menus at other restaurants.

Chipotle stock has dragged its feet since peaking in 2021. I think more of the same is in the cards. Despite the rocky ride, shares still command a very premium 46.3 times trailing earnings multiple, which is much higher than the restaurant industry average of 33.9 times. However, despite short-term headwinds, the company’s growth potential looking beyond a recession keeps me bullish for the long term.

What is the Price Target for CMG Stock?

Wall Street maintains its “Strong Buy” consensus on Chipotle, with 17 Buys and five Holds. The average CMG stock price target of $1,850.71 implies 22.6% gains.

Conclusion

Many fast-food firms are betting big on various initiatives to drive foot traffic. Restaurant modernization and menu innovation are two potential catalysts that could help the top fast-food plays to power growth in a harsher environment.

Both McDonald’s and Chipotle have delivered on the tech front. Between the two names, Wall Street expects more gains from Chipotle. It’s the harder hit of the two and could enjoy more explosive upside once the market’s ready to look past a potential recession.