Alibaba Stock (NYSE:BABA) continues to suffer from tireless bearish sentiment that shows no sign of reversal. Although the S&P 500 (SPX) gained 20% in the past year, shares of the Chinese e-commerce giant have tumbled by 28% during the same period. Despite BABA’s improving earnings and capital returns, I believe that unless the total shareholder yield grows notably larger and/or global sentiment toward Chinese stocks shifts, shares could continue their underwhelming trajectory. Thus, I am neutral on the stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Unpacking Alibaba’s Underperformance – What’s Causing It?

Given the possible interplay of several factors, it’s hard to point out precisely what’s causing Alibaba’s underperformance. However, I would say that among these, a lasting investor mistrust towards Chinese-listed companies on U.S. exchanges, an unprecedented bearish sentiment surrounding Chinese stocks, even those listed on Asian exchanges, and a lack of substantial capital returns in proportion to Alibaba’s profits all likely contribute to this rather paradoxical situation.

The overall lack of positive sentiment surrounding Alibaba’s stock isn’t a recent occurrence; it’s a common theme negatively impacting all Chinese companies listed on U.S. exchanges. To a certain extent, it is fair. Why? Well, my extensive research into Chinese companies over the years has led me to conclude that they operate with fundamentally different values. Unlike their U.S. counterparts, Chinese companies are often unconcerned about maximizing shareholder value.

In stark contrast to the norm in the U.S., management teams in Chinese companies appear indifferent to their stock prices. There are numerous examples of companies listed on Chinese exchanges trading at 3x-4x earnings without engaging in share buybacks. It’s also not uncommon to find Chinese stocks posting growing earnings. Yet, their dividends exhibit significant variations from year-to-year and, in some cases, even decline without any provided explanation.

These occurrences are so common that, coupled with a general skepticism of the accounting standards and corporate governance of Chinese companies, they result in equities often trading at depressed levels.

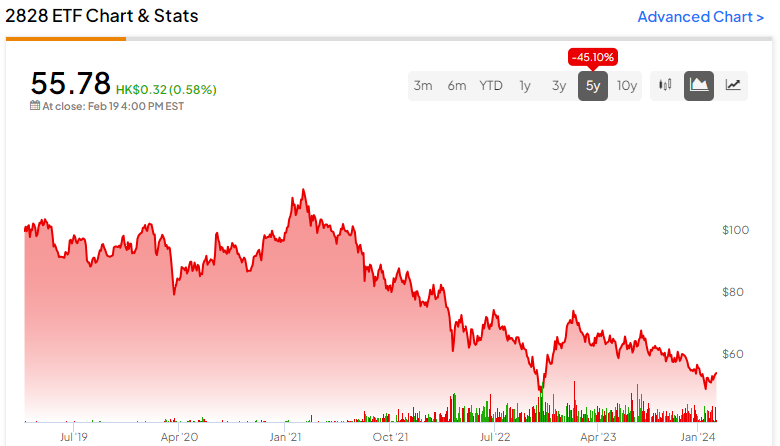

On top of that, earlier, I mentioned the ongoing unprecedented bearish sentiment surrounding Chinese stocks, with the Hang Seng Index declining for the 4th straight year in 2023. Just take a look at Hang Seng China Enterprises Index ETF (HK:2828), one of the largest ETFs, which follows the index getting hammered year after year since 2020.

What makes Alibaba a special case compared to the average Chinese stock, however, is that this is a giant generating over $130 billion in annual sales. Unlike obscure Chinese stocks run by relatively unknown managers, Alibaba is a global giant that commands the attention of a large number of investors and funds worldwide. The stock is held by numerous institutions run by highly credible investment managers. That’s why its consistent underperformance against an improving financial profile is extremely intriguing.

Nevertheless, even in the case of Alibaba, we continue to see some of the very same signs that trouble investors with Chinese stocks in general. For example, even though management has acknowledged the stock’s undervaluation and addressed this issue by committing to engage in stock buybacks, the rate of buybacks remains underwhelming for no apparent reason. Specifically, during the calendar year of 2023, Alibaba repurchased a total of $9.5 billion worth of its shares. However, this implies a mere buyback yield of about 5% at the stock’s current market cap.

In another move reflecting management’s commitment to enhance the stock’s attractiveness to investors, Alibaba declared its inaugural dividend as part of its Fiscal Q2 results. This action aimed to bridge the valuation gap by providing investors with a real, tangible capital return, thereby bolstering the overall predictability of the stock’s investment proposition.

However, the declared $1.00 dividend per ADR yields a somewhat underwhelming 1.4% at the stock’s current level. So yes, Alibaba seems to consistently be a remarkably cheap stock, yet the blended yield of 6.4% (dividend+buybacks) is hardly enough to generate significant enthusiasm. This is particularly true since investors are certain to seek a notably higher blended yield from Alibaba, given the inherent risks associated with its investment case.

The Valuation Gap May Not Close for a Long Time

Due to the absence of a substantial total shareholder yield to reward investors, it’s quite likely that Alibaba’s valuation gap may not close for a long time. On the one hand, Alibaba is trading at a P/FCF of 8.6x and a forward P/S and P/E ratios of 1.4x and 8.8x, respectively, signaling that the stock is a bargain.

On the other hand, this narrative has persisted for a few years, and the stock has ended up falling behind the general indexes every time. Therefore, it’s not unlikely to see the stock behave this way for another year, irrespective of its underlying financials.

In my view, for Alibaba stock to gain significant momentum and garner a more optimistic market sentiment, one or both of the following scenarios need to unfold:

- Alibaba achieving a blended yield that surpasses the 10% mark. I believe that a combination of share buybacks and dividends with such a robust yield has the potential to capture investors’ attention, essentially forcing them to reevaluate the stock. The rich, tangible capital returns would be too good to overlook, even in light of the inherent risks associated with the stock.

- A broader resurgence in Chinese equities, particularly with regard to the Hang Seng Index. Should Chinese markets experience a rebound, Alibaba’s Hong Kong listing is likely to witness a substantial upswing as well, subsequently translating into a rally for its NYSE listing.

Is BABA Stock a Buy, According to Analysts?

Despite the stock performance, most Wall Street analysts remain bullish on Alibaba’s prospects. The stock has garnered a Strong Buy consensus rating based on 15 Buys and three Holds. At $101.49, the average BABA stock price target implies an attractive upside potential of 34.3%.

The Takeaway

Overall, it’s clear that Alibaba’s persistent underperformance in the face of improving financials reflects the broader challenges facing Chinese stocks on both U.S. and Chinese exchanges. Despite some efforts by management to address the stock’s low valuation through buybacks and dividends, the impact has so far been underwhelming, failing to meaningfully change investor sentiment.

Therefore, even though many investors argue that Alibaba’s rally is just around the corner, I have come to the conclusion that the stock needs to achieve a much higher blended yield or benefit from a broader resurgence in Chinese equities. Until then, a long history of letdowns has taught me to have little to no expectations.