FireEye Inc. (FEYE) is a California-based cybersecurity company. It recently announced the sale of its FireEye Products business to focus on its Mandiant brand.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Let’s take a look at FireEye’s latest financial performance, corporate updates, and risk factors.

FireEye’s Q2 Financial Results and Q3 Outlook

The company reported a 17% year-over-year increase in revenue to $114 million for the second quarter. It posted an adjusted loss per share of $0.14. The results exclude the FireEye Products business, which is being divested and has been marked as a discontinued operation. (See FireEye stock charts on TipRanks).

FireEye bought back $68 million of its shares during Q2 under its board-approved $500 million stock repurchase program.

For Q3, the company anticipates revenue in the band of $118 million – $122 million. It expects an adjusted loss per share in the band of $0.16 – $0.14. The company reminds investors that the guidance is subject to certain risk factors.

FireEye’s Corporate Updates

FireEye aims to close the sale of its FireEye Products business by the end of the fourth quarter of 2021. It expects to receive $1.2 billion in cash from the transaction, and the buyer will assume certain liabilities related to the unit. After the sale of the unit, FireEye will primarily rely on its Mandiant business for revenue.

As it works on concluding the unit sale, FireEye has moved to acquire Intrigue to bolster its remaining Mandiant business. Intrigue provides attack surface management solutions.

FireEye’s Risk Factors

The new TipRanks Risk Factors tool reveals 75 risk factors for FireEye. Since December 2020, the company has updated its risk profile to add five new risk factors under the Finance and Corporate and the Ability to Sell categories.

FireEye says it cannot assure investors that it will fully execute its stock repurchase program. It further cautions that the repurchase program could reduce its cash reserve and fail to enhance long-term shareholder value.

The company warns investors that the sale of the FireEye Products unit may adversely impact staff focus and morale. It further says that failure to close the sale in a timely manner could adversely affect the results of its operations.

Additionally, FireEye cautions that it may not achieve the anticipated benefits of the FireEye Products unit sale. It says that if its strategy is unsuccessful, its stock price could decline.

Finance and Corporate is FireEye’s main risk category, accounting for 41% of the total risks. That is above the sector average at 39%. FireEye’s shares have declined about 20% since the beginning of 2021.

Analysts’ Take

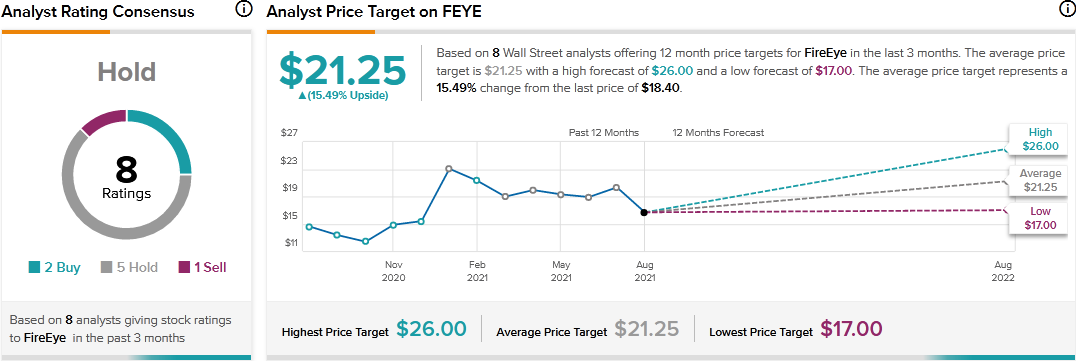

Robert W. Baird analyst Jonathan Ruykhaver recently downgraded FireEye’s stock rating to a Hold and cut the price target to $20 from $24. Ruykhaver’s new price target suggests 8.70% upside potential. The analyst cited increased execution risk as the reason for the downgrade.

“While we continue to appreciate the strategic rationale behind the divestiture, we are more comfortable waiting on the sidelines for now until we see the company prove its ability to drive success (particularly on the subscriptions side) with the standalone business,” commented Ruykhaver.

Consensus among analysts is a Hold Buy based on 2 Buys, 5 Holds, and 1 Sell. The average FireEye price target of $21.25 implies 15.49% upside potential to current levels.

Related News:

What Do Tenable’s Newly Added Risk Factors Tell Investors?

Dollar General Q2 Results Top Estimates, Raises Guidance

Domo Q2 Results Surpass Estimates; Shares Decline 8.4%