Volkswagen AG (VWAGY) has removed Herbert Diess as the company’s CEO, The Wall Street Journal reported, citing people familiar with the matter. He will step down on September 1.

The ouster follows an internal disagreement over the delay in developing core software for electric vehicles (EVs). The Germany-based company had to postpone the launches of a few electric models due to the delay. This raised doubts about Diess’ promise to turn Volkswagen into a top EV maker.

Diess joined Volkswagen in 2015 and was named the CEO in 2018.

Oliver Blume, the CEO of Volkswagen’s subsidiary Porsche, will succeed Diess. Blume, who joined the automaker in 1994, will continue to run Porsche as well.

Wall Street’s Take on Diess’ Removal

In a note to clients, Daniel Roeska, an analyst at Bernstein Research, said, “The hope of the supervisory board must be for new group CEO Blume to have more success in guiding the software strategy of the group. However, it will take months to come up with a new plan, and creating unrest as the group is heading into a challenging 2023 is the wrong time.”

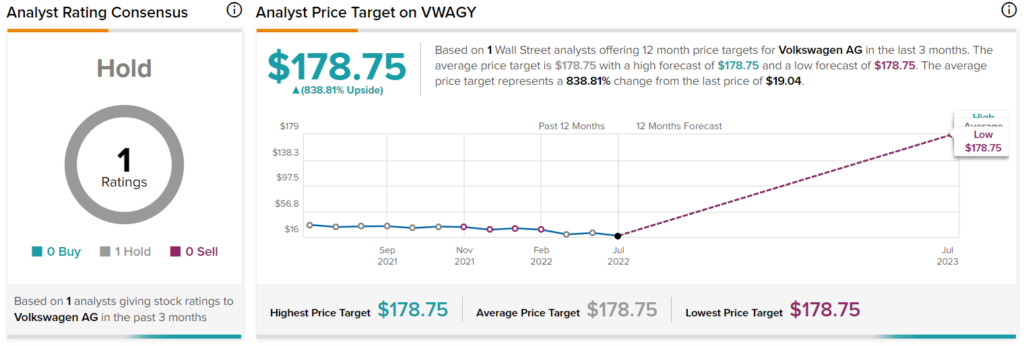

As per TipRanks, the stock has a Hold consensus rating based on a single Hold. VWAGY’s average price target of $178.75 reflects upside potential of 838.8% from current levels.

Volkswagen Likely to Perform in Line with the Market

According to TipRanks’ Smart Score rating system, Volkswagen scores a five out of 10, suggesting that the stock is expected to perform in line with the market.

Investors’ Reaction to the News

Following the release of the news on Friday, VWAGY stock lost 1.8% to close at $19.04. The announcement comes just days ahead of the company’s second-quarter results, which are scheduled to be released on July 28. The Street anticipates the company to report earnings of $0.43 per share, lower than the year-ago figure of $1.15 per share.

Read full Disclosure