Verint shares are rising about 9.7% in Thursday’s pre-market trading as the software company announced better-than-expected results for the second quarter of fiscal 2021, which ended July 31. The company announced its results after the close of financial markets on September 9.

Verint Systems’ (VRNT) fiscal second-quarter revenue declined 4.7% Y/Y to $309.1 million but exceeded analysts’ estimate of $299.2 million. Second-quarter results gained from an acceleration in cloud business amid the pandemic. Plus Verint’s on-premises business began to recover from the initial impact of COVID-19. Adjusted EPS grew 29.3% to $1.06 and was way ahead of analysts’ forecast of $0.69.

“Our cloud-first strategy is working well. In Q2, we delivered strong cloud revenue growth, strong SaaS bookings growth, and an increase in the percentage of our software revenue that is recurring.” said CEO Dan Bodner. “During the quarter, we continued to win new cloud customers and displace competitors due to our strong differentiation in artificial intelligence and automation and communications infrastructure neutrality.”

Looking ahead, the company expects continued cloud momentum in the second half of the year and gradually recovery in on-premises deals. It anticipates non-GAAP revenue to improve sequentially both in 3Q and 4Q and adjusted EBITDA for 2020 to be similar to last year. (See VRNT stock analysis on TipRanks)

Meanwhile, the company is also on track to separate into two independent public companies and expects to complete the separation shortly after the end of fiscal 2021. In December 2019, Verint announced that it will split into two companies, one of which will comprise its customer engagement business, while the other will consist of its cyber intelligence business.

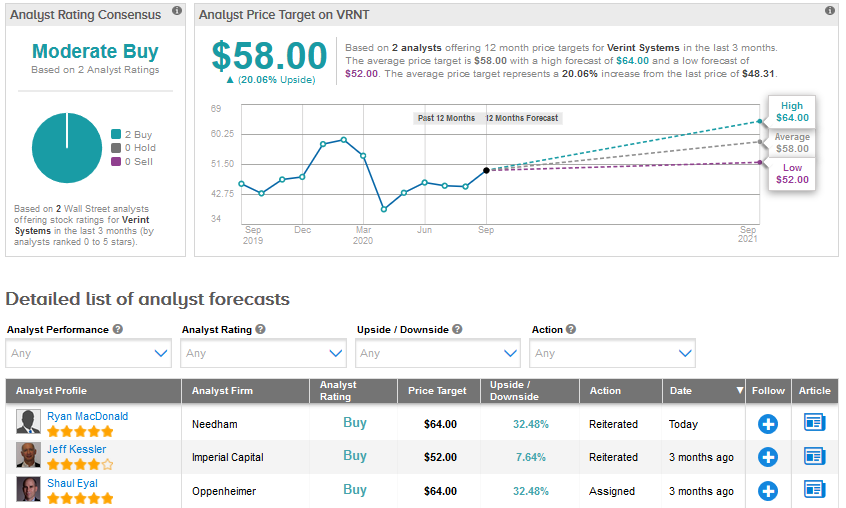

Following the better-than-anticipated results, Needham analyst Ryan MacDonald raised his price target for Verint to $64 from $53 and reaffirmed a Buy rating. The analyst stated, “Given the expectation of seq. growth in 2H’21 suggests a continuation of these positive trends, we have an increased confidence that the fundamentals will continue to improve in a post-COVID environment.”

The Street shares MacDonald’s bullish stance and has a Strong Buy consensus based on 6 Buys and no Holds or Sell ratings. Verint stock has declined 12.6% year-to-date but the average analyst price target of $58.00 indicates a possible upside of 20% ahead.

Related News:

Zscaler 4Q Sales Outperform Fueled By Cybersecurity Demand

GameStop Sinks 15% In Pre-Market On 2Q Miss

Corning Gains 4% On Upbeat 3Q Revenue Outlook