Second quarter earnings season is winding down in its usual fashion, with retail reports, just in time for the summer doldrums. At this point nearly 90% of S&P 500 companies have reported, and according to FactSet 83% have beaten bottom-line expectations, the highest number in 12 years, since they began tracking this data. It turns out a lack of corporate guidance prompts analysts to be even more conservative with their estimates.

China is an important player for most multinational retailers, but perhaps never more important than they will be this quarter, and for the remainder of the year. According to FactSet, 4.8% of revenues from S&P 500 companies comes from China, the largest amount from any individual country. While the sector with the greatest impact here is no doubt Technology, Consumer Discretionary is catching up. Many companies that have already reported this season have credited China with somewhat salvaging the quarter, as the economy there has bounced back and instances of COVID-19 infections after reopening have remained subdued.

Nike, for example, reported that Greater China was the only region that saw revenue growth last quarter, of 1% (excluding the impact of currency changes). Similar sentiments regarding strength in China can be seen in recent reports from peers such as Lululemon and Under Armour.

Other consumer areas are seeing the same trend. When Marriott reported Q2 results this morning, overall results were dismal, with EPS down 141% YoY and revenues declining 72%. Yet, in Greater China, occupancy levels are at 60%, just 10 percentage points below where they were this time last year. They also reported the improvements were not just due to higher demand for leisure travel, but increased business demand as well.

No sub-sector of retail relies quite as heavily on the Chinese customer as luxury does. Brands such as LVMH Moët Hennessy Louis Vuitton SE have already reported that strength in China has helped to offset weakness in other regions. This week we hear from a few more luxury and premium brands that will be counting on the region to also give them a boost, that’s if increased political tensions between the two nations doesn’t get in the way, an issue that has been top of mind for many of these brands over the last year.

Farfetch (FTCH)

Reports Thursday, August 13, after the close

- Earnings growth: -87%

- Revenue growth: 56%

- Analyst Consensus Rating: Strong Buy

- Price Target: $23.23 (14.55% downside)

- Smart Score: 9

Despite the current economic environment which doesn’t seem like it would be great for the luxury space, Farfetch continues to thrive, it’s stock up nearly 150% YTD. They are uniquely positioned to sell from luxury retailers, with an online platform that boasts products from over 700 global boutiques and brands. Recent investments in building out global logistics capabilities, geo-diversified supply network and localized services for a global consumer base have clearly paid off.

CEO and founder, Jose Neves, admitted on the Q1 call that things will probably never go back to the “normal” we knew pre-COVID, and that will likely cause structural changes that impact the luxury industry, but reassured “I am confident that our unique set of capabilities position Farfetch to be even stronger in the future.”

It’s also important to note that Farfetch has a particular focus on China, earlier this year announcing it raised $250M from Chinese tech behemoth, Tencent, and Dragoneer, a California based investment group. This move was made with the intent of supporting growth plans that include China as a key market. According to Bain & Co., China is projected to account for 46% of all luxury sales by 2025. Not only is this an important move for FTCH’s long-term growth, but seems to be coming at a time when China could be a life-line to retail survival, with consumer health there rebounding at a much quicker pace.

Revolve (RVLV)

Reports Wednesday, August 12, after the close

- Earnings growth: -83%

- Revenue growth: -26%

- Analyst Consensus Rating: Moderate Buy

- Price Target: $15.14 (14.17% downside)

- Smart Score: 7

While they operate in a similar space as Farfetch, Revolve appears to be poised for more disappointment this quarter. The e-tailer officially pivoted away from operating exclusively in the luxury space after the recession, they now focus on a broader range of products, most of which fall into the premium bucket.

Revolve has built a huge following through social media by partnering with influencers. They’ve become known for their Revolve festivals and “Revolve Around the World” events in which they host influencers, models and actresses in exotic locations. These sort of branding activities have been genius up until this point. But what happens to that model when travel and large social gatherings are paused? Well you can see the answer in those earnings and revenue expectations.

Estimates for 2021 seem to be suggesting that analysts believe there will be a vaccine by then that allows for more of these events to return, with EPS growth anticipated to be 83% and revs 23% for Q1 2021, the next time both metrics are anticipated to be positive.

While RVLV is more often tied to LA trendsetters, they have been growing their China base organically over the years, as more interest from that region came when they started offering international shipping in 2008, prior to any real investment. The ongoing U.S.- China trade war has induced anxiety for Revolve, as it has for other brands concerned about how tariffs will impact their business. As of earlier this year, however, the company said their tariff exposure level is manageable, but if tariffs were to be increased they would be forced to either raise prices, which would limit their competitiveness with similar brands, or take a hit on gross margins.

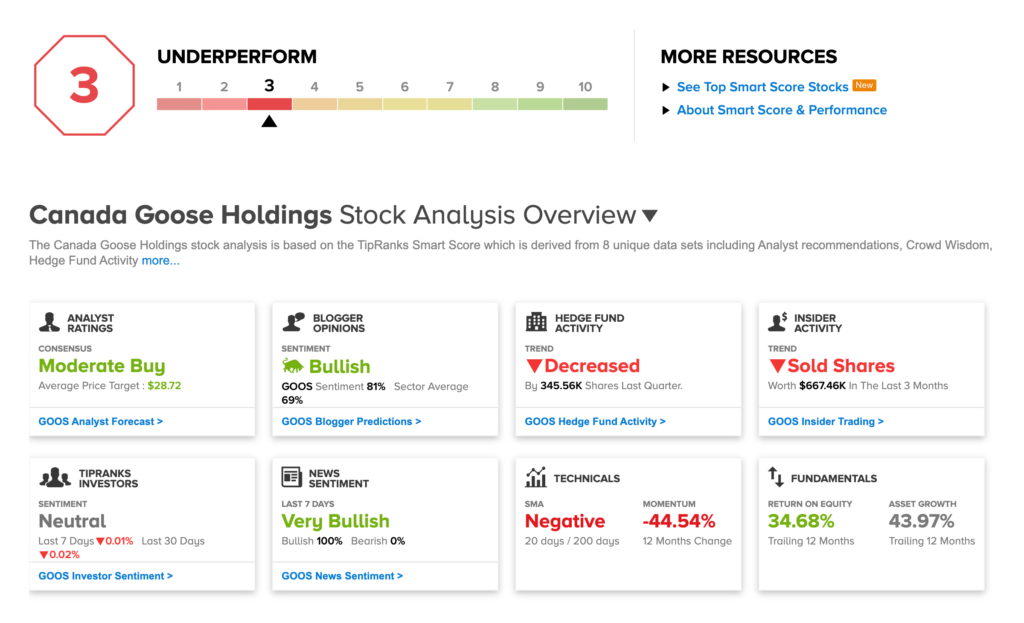

Canada Goose (GOOS)

Reported Tuesday, August 11, before the open

- Earnings growth: -72%

- Revenue growth: -73%

- Best Analyst Consensus Rating: Hold

- Price Target: $25.40 (6.14% upside)

- Smart Score: 3

Canada Goose, the seller of those $1000+ goose down winter jackets, reported better than expected results this morning, beating EPS estimates by 3 cents, and revenue estimates by $4M. While they have an e-commerce presence, they do most of their sales at their brick and mortar stores, most of which had to be shut completely down until May.

GOOS is heavily exposed to China, the site of its most active international shoppers. On the company’s June 4 earnings call, CEO Dani Reiss spoke about the early green shoots of recovery they were seeing there. “When it comes to Mainland China, we are seeing good strong performance coming back very gradually, high conversion rates, particularly standing out. And that doesn’t matter whether I’m talking about Shanghai, Beijing or Shenyang. I’m seeing it in all of them, and I’m seeing it more strongly online.”

We saw some of that continued strength in today’s report, with the company stating all new store openings will be focused in China, “where the recovery of traffic remains ahead of other markets. With international tourism now heavily constrained, serving the world’s largest luxury consumer base at home is increasingly crucial. The first of 4 committed new stores opened in Chengdu in June and it has consistently performed ahead of expectations.”

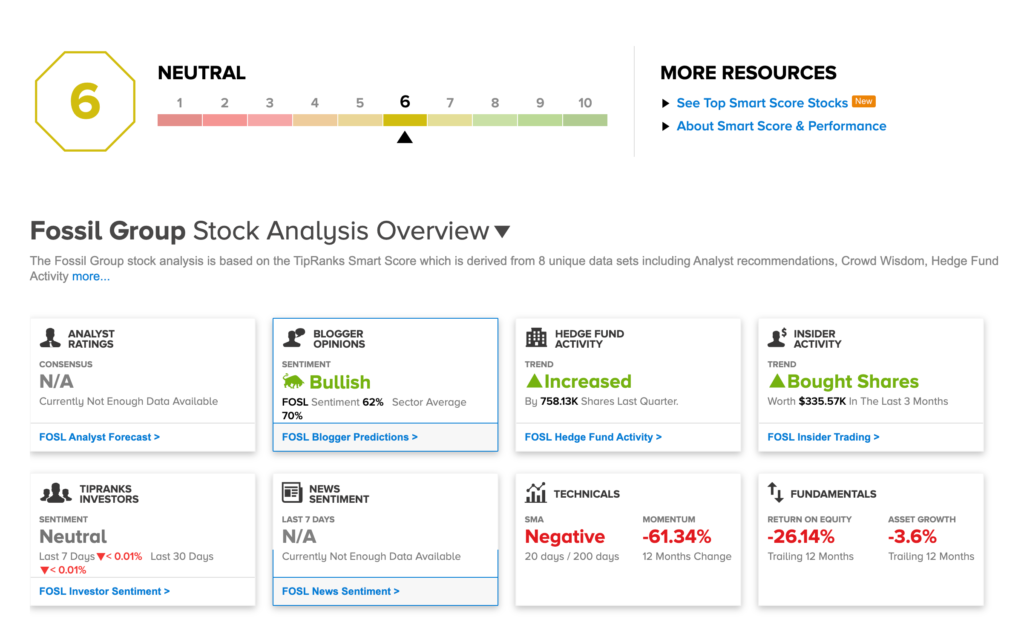

Fossil Group (FOSL)

Reports Wednesday, August 12, after the close

- Earnings growth: -4165%

- Revenue growth: -64%

- Analyst Consensus Rating: Strong Buy

- Price Target: $241.94 (15.72% downside)

- Smart Score: 10

Fossil has been hurting for a while, with interest in traditional watches declining. They tried to get behind the smart watch trend with their partnership with xx, but it hasn’t had meaningful impact. The bottom-line has seen declines for the last 4 quarters. Closure of stores and wholesale partners throughout much of Q2 due to COVID-19 has not helped, the company saying they expect a decline of worldwide net sales of 60 – 70%, “with a contraction in retail and wholesale partly offset by strength in e-commerce channels.” The companies investment in digital capabilities including a new global e-commerce platform has come at the right time, but won’t be enough to save them this quarter.

Fossil gets approximately 12% of it’s revenue from China, which continues to be a region of focus and expansion for the company. Despite seeing sales decrease 7% in Asia last quarter, Greater China revenues grew by double-digits, with particular interest in their Armani portfolio.

“The impacts of COVID may disrupt our growth trajectory in the short-term, but we are seeing strong performance in China year-to-date, and continue to view both of these markets [and India[ as compelling long-term opportunities.”

Tapestry (TPR)

Reports Tuesday, August 13, after the bell

- Earnings growth: -195%

- Revenue growth: -56%

- Analyst Consensus Rating: Moderate Buy

- Price Target: $16.50 (13.71% downside)

- Smart Score: 7

There is so much more than COVID plaguing Tapestry this quarter. Not only is the accessories space in a slump due to the pandemic and less people going out, but a shake up in management is currently underway. Just last month, CEO Jide Zeitlin resigned suddenly after allegations of personal misconduct.

Despite strong e-commerce growth last quarter, it was not enough to offset the sales lost from store closures. Coach sales were down 20%, Kate Spade down 11% and Stuart Weitzman down 40%.

There has also been mention of plans to reduce the workforce, both at the corporate and retail level. The company said to expect pretax charges of roughly $55-$70M, related to severance costs, starting in Q4.

Acceleration of growth in Mainland China remains a strategic goal across all Tapestry brands, but especially Coach, where the region represents their largest geographic growth opportunity.

“Chinese customers are proving resilient in their continued appetite for fashion and luxury. Our strong brand momentum and positioning will enable us to benefit from the rapid growth of the Chinese middle class.”