HubSpot (HUBS) provides a cloud-based software platform for marketing, sales, and customer services. The platform is available in more than 120 countries.

For Q4 2021, HubSpot reported a 47% year-over-year rise in revenue to $369.3 million and exceeded the consensus estimate of $357.5 million. It posted adjusted EPS of $0.58, which rose from $0.40 in the same quarter the previous year and beat the consensus estimate of $0.53.

For Q1 2022, HubSpot anticipates revenue in the band of $381 million to $383 million. It expects adjusted EPS in the range of $0.46 to $0.48. The consensus estimate calls for EPS of $0.46 on revenue of $377 million.

With this in mind, we used TipRanks to take a look at the risk factors for HubSpot.

Risk Factors

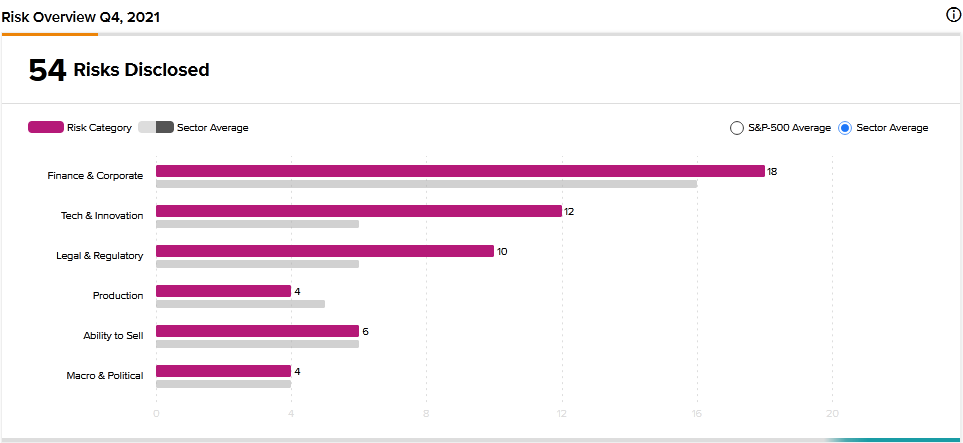

According to the new TipRanks Risk Factors tool, HubSpot’s top risk category is Finance and Corporate, with 18 of the total 54 risks identified for the stock. Tech and Innovation and Legal and Regulatory are the next two major risk categories with 12 and 10 risks, respectively. The company recently introduced a new risk factor and updated several previously outlined risk factors.

The newly added risk factor falls under the Tech and Innovation category and relates to the challenge of keeping HubSpot’s systems running properly. The company explains that it maintains a complex IT system that requires constant software updates to correct defects or errors.

The company cautions that if it fails to correct errors in its systems, its internal operations and services provided to customers could be disrupted. HubSpot warns that such disruptions could result in revenue loss, increased expenses, and damage to its reputation. Moreover, the company’s cash flow and stock price may also be harmed.

In an updated Tech and Innovation risk factor, HubSpot tells investors that broader adoption of its solutions will depend on the effectiveness of its salesforce. As a result, the company will continue to invest significant resources to expand its sales and marketing capabilities. The problem is that the investments in expanding its marketing capabilities may not lead to the anticipated revenue growth.

In an updated Macro and Political risk factor, HubSpot informs investors that the COVID-19 pandemic situation remains highly unpredictable. For example, it cautions that economic shocks stemming from the pandemic could adversely affect the demand for its products. The company also explains that it may experience challenges retaining existing customers and adding new ones.

HubSpot stock has declined about 21% year-to-date.

Analysts’ Take

Mizuho Securities analyst Siti Panigrahi recently maintained a Buy rating on HubSpot stock and raised the price target to $625 from $500. Panigrahi’s new price target suggests 30.60% upside potential. The analyst commented that HubSpot stands to benefit from digital transformation efforts as the company continues with its product expansion.

Consensus among analysts is a Strong Buy based on 17 Buys and 2 Holds. The average HubSpot price target of $725.16 implies 51.53% upside potential to current levels.

Download the TipRanks mobile app now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

SoFi Technologies to Acquire Technisys for $1.1B

Meta Platforms’ Facebook Takes Reels Global

Amgen Issues Green Bond for The First Time