Texas-based Copart (CPRT) operates a global online vehicle auction platform. It sells vehicles in more than 170 countries to more than 750,000 members. The company auctions vehicles on behalf of banks, insurance companies, rental car companies, dealers, fleet operators, and individuals.

Let’s take a look at the company’s latest financial performance and changes in its risk factors. (See Copart stock charts on TipRanks).

Q4 Financial Results

Revenue for the fourth quarter of Fiscal 2021 (ended July 31) increased 42.4% year-over-year to $748.6 million, beating the consensus estimate of $688.56 million. The company posted adjusted EPS of $1.03, compared to $0.68 a year ago, beating the consensus estimate of $0.91. Copart ended Q4 with $1.05 billion in cash and $397.64 million in long-term debt.

For Fiscal 2021, revenue increased 22.1% to $2.7 billion. Additionally, adjusted EPS for the year was $3.70, compared to $2.56 in the previous year.

Risk Factors

The new TipRanks Risk Factors tool shows 37 risk factors for Copart. In its Fiscal 2021 annual report, the company introduced one new risk factor and removed one previously highlighted risk factor. All the changes were classified under the Finance and Corporate category.

In the newly added risk factor, Copart tells investors that it has designated a specific court in Delaware as the exclusive forum for settling disputes with shareholders. It says this may limit the ability of shareholders to raise disputes in courts of their choice. However, Copart cautions that it may incur additional costs if it were forced to settle shareholder lawsuits outside its preferred court.

The company removed the risk factor that warned that an impairment of goodwill could cause a material adverse effect on its results of operations.

The majority of Copart’s risk factors fall under the Finance and Corporate category, with 24% of the total risks. That is below the sector average of 37%. Copart’s stock has gained about 11% year-to-date.

Analysts’ Take

Following Copart’s Q4 report, Truist analyst Stephanie Moore reiterated a Buy rating on Copart stock and raised the price target to $160 from $145. Moore’s new price target suggests 13.36% upside potential.

Moore noted that Copart’s Q4 results beat expectations and that the company’s revenue will continue to grow in Fiscal 2022.

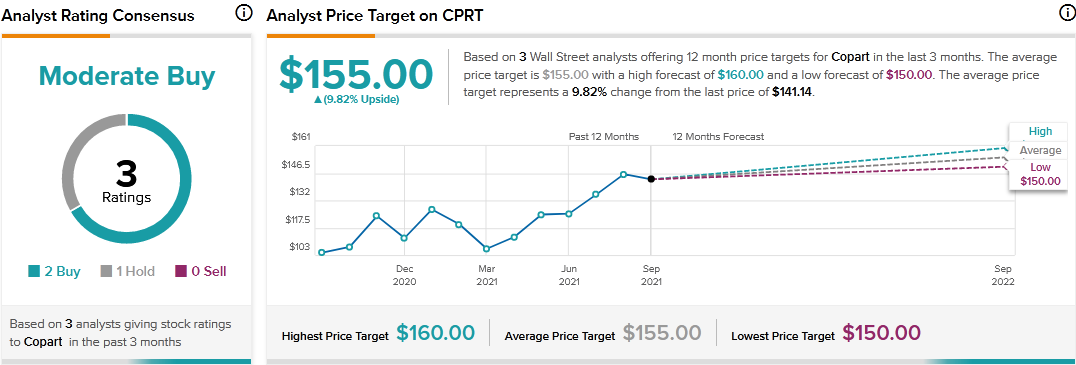

Consensus among analysts is a Moderate Buy based on 2 Buys and 1 Hold. The average Copart price target of $155 implies 9.82% upside potential to current levels.

Related News:

Gauging Veracyte’s Newly Added Risk Factors?

Understanding Associated Banc-Corp’s Risk Factors

TransAlta Hikes Dividend by 11%, Sets Growth Targets