When a company starts considering “strategic options,” there’s usually an effect on its stock as well. In payroll services provider TriNet’s (NYSE:TNET) case, that’s just what happened. And investors are over the moon about the idea, sending shares up in a double-digit surge at one point in Friday afternoon’s trading.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The latest reports from Reuters note that TriNet is working with Morgan Stanley in a bid to find some potential buyers. Whoever does go in for such a deal will need deep pockets, as TriNet was last valued at around $5.8 billion. With TriNet’s shares recently climbing—up 44% this year before the Reuters report even hit—it’s a safe bet that it might draw at least some interest.

Naturally, TriNet wasn’t talking; it has a policy against “discussing rumors or speculation.” However, there’s more of a draw to TriNet than just its healthy market cap. At last report, TriNet has around 23,000 clients, and it processes more than $70 billion in payroll annually. That’s one monster client list, and any business services operation—from cloud services to staffing and beyond—could likely find somebody interested in something to cross-sell. Meanwhile, the company most likely to benefit from such a sale is the private equity firm Atairos, which owns 36% of TriNet from a deal back in 2017.

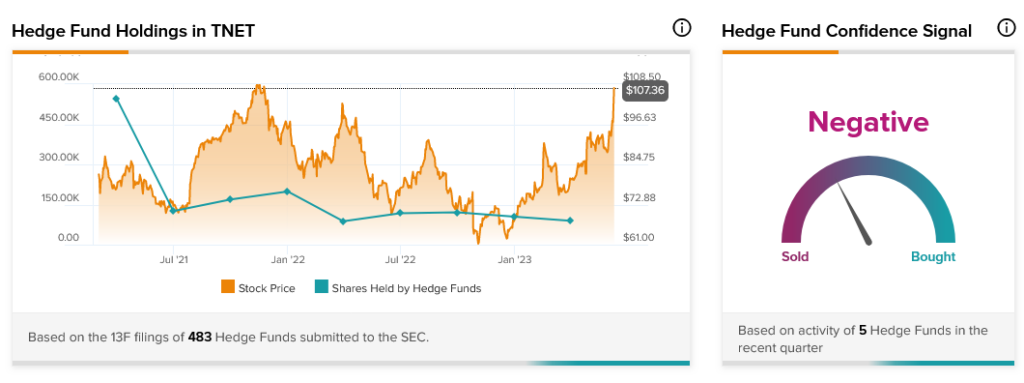

However, despite this great potential, hedge funds aren’t that enthusiastic about TriNet. Currently, the hedge fund confidence level for TriNet is “Negative” after lowering their holdings by 16,200 shares last quarter. Moreover, this is the second quarter running that hedge funds have lowered their stakes in TriNet.