Stock indices finished today’s trading session in the green. The Nasdaq 100 (NDX), the S&P 500 (SPX), and the Dow Jones Industrial Average (DJIA) gained 0.84%, 0.59%, and 0.35%, respectively.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

The utilities sector (XLU) was the session’s laggard, as it fell 2.16%. Conversely, the consumer discretionary sector (XLY) was the session’s leader, with a gain of 1.1%.

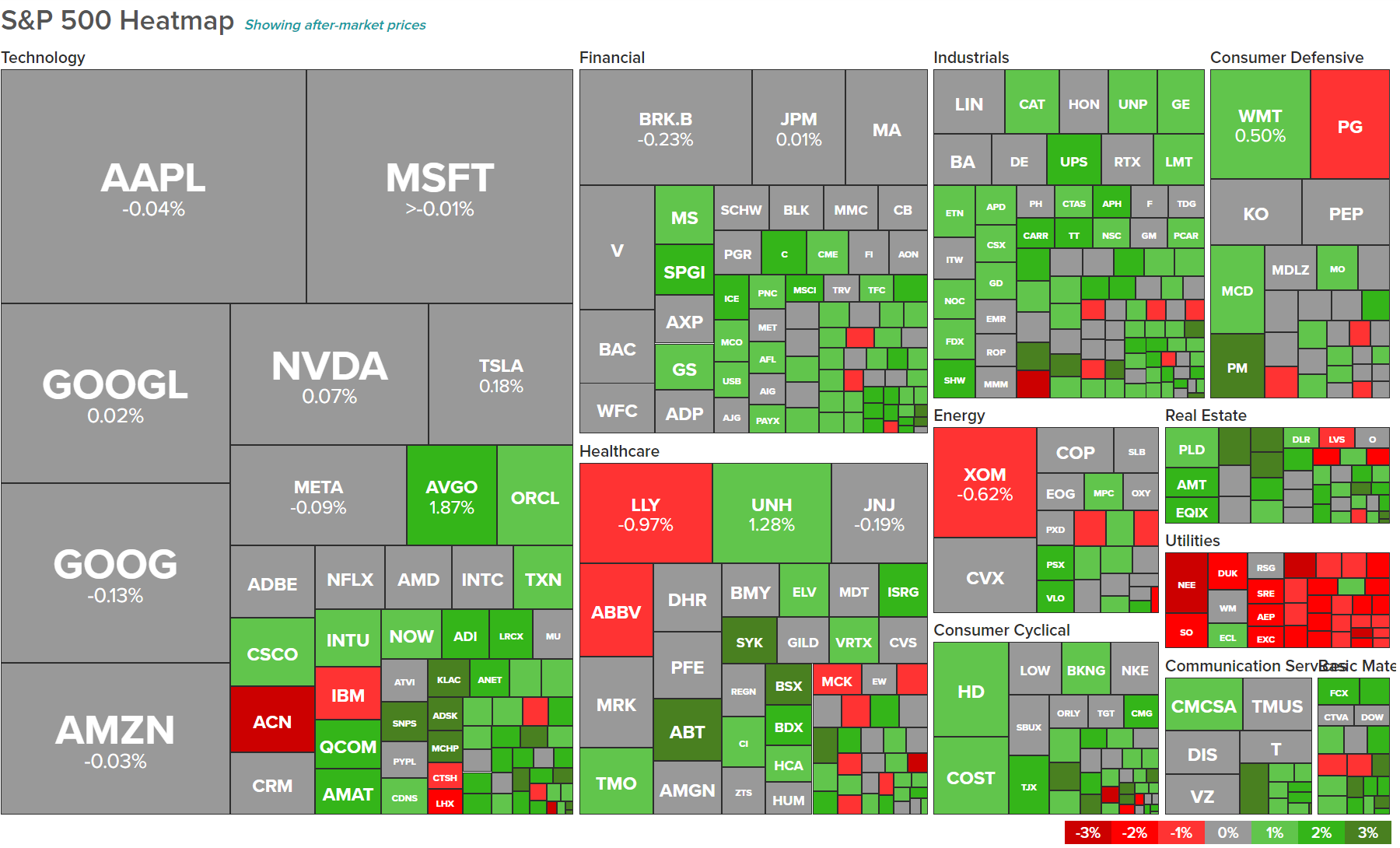

A quick look at the heatmap for the S&P 500 shows a lot more green than red, although the largest stocks in the market saw minimal change.

Furthermore, the U.S. 10-Year Treasury yield decreased to 4.57% while the Two-Year Treasury yield also slipped, as it hovers around 5.06%.

Last updated: 2:29PM EST

Stock indices are in the green so far in today’s trading. Earlier today, J.P. Morgan released its Cost of Living Survey, which showed that a significant portion of U.S. consumers expressed concerns over stagnant wages and insufficient savings. The survey took responses from over 1,000 U.S. participants and revealed that 56% haven’t seen a salary increase in the past six months, a figure that’s notably higher than results from March 2023.

The decline is especially pronounced among middle and low-income demographics. Over half of the respondents feel their savings wouldn’t suffice to maintain their lifestyle, and 61% feel less optimistic about managing household bills and essential expenditures than they did six months ago. Furthermore, the data suggests a shift in non-essential spending habits, with clothing, especially casual wear, taking precedence, while luxury items and holidays abroad lagged.

In other news, the Freddie Mac Primary Mortgage Survey shows a surge in long-term mortgage rates. The 30-year fixed-rate mortgage rose to an average of 7.31% as of September 28, a noticeable climb from 7.19% just a week earlier and the highest level since 2000.

Last updated: 12:15PM EST

On Thursday, the National Association of Realtors released its Pending Home Sales report, which measures the month-over-month change in the number of home sales that have yet to close but are contracted to be sold. This measure excludes homes that are newly constructed.

During August, Pending Home Sales decreased by 7.1% compared to July, which was worse than the expected -0.8% decrease. This is after a 0.5% increase in the previous report.

In addition, the Pending Home Sales Index came in at 71.8, which is lower than the 88.5 reading from the same time last year. This equates to an approximate decline of 18.9% on a year-over-year basis.

Last updated: 9:30AM EST

Stocks opened lower on Thursday morning after jobless claims data, with the Nasdaq 100 (NDX), S&P 500 (SPX), and the Dow Jones Industrial Average (DJIA) down by 0.04%, 0.07%, and 0.01%, respectively, at 9:30 a.m. EST, September 28.

The jobless claims data indicated that there were no signs of rising unemployment as initial jobless claims data for the week ending September 23 went up by 2,000 to 204,000. Economists had forecast new claims of 215,000. The jobless claims data indicated that job losses remained low and showed signs of a resilient U.S. economy.

Meanwhile, U.S. Q2 GDP growth advanced by 2.1% on an annualized basis, slightly higher than forecasts of a 2% increase.

First published: 4:10AM EST

U.S. Futures are trending near the flatline on Thursday morning as traders assess the impact of high treasury yields and even higher oil prices. WTI crude oil futures touched their 52-week high yesterday and are hovering near $94.27 as of the last check. In the meantime, the U.S. 10-year treasury yields are up 4.61%. Both elements are adding to the sluggishness of the already weak trading month of September. Futures on the Nasdaq 100 (NDX), S&P 500 (SPX), and the Dow Jones Industrial Average (DJIA) are up by 0.04%, 0.07%, and 0.01%, respectively, at 4:10 a.m. EST, September 28.

On the economic front, the Weekly Initial Jobless claims and final GDP estimates data will be out later today. Notably, consumers continue to remain wary of the high interest rate environment and the Fed’s hint of one more rate hike before year-end.

Turning to stocks, shares of oil and gas companies have been surging in tandem with rising oil prices. Exxon Mobil stock (XOM) hit a new 52-week high yesterday. Meanwhile, Peloton (PTON) shares rallied in Wednesday’s extended trading in reaction to a five-year strategic partnership with Lululemon (LULU). Also, Micron stock (MU) fell in after-hours trading on soft earnings guidance despite beating Q4FY23 expectations. Footwear maker Nike (NKE) will report its Fiscal Q1-2024 financial results after the market closes today.

Elsewhere, European indices are trading mixed today as markets feel the heat from the impact of a gloomy economic environment. Traders will also parse preliminary inflation data for September from Germany and Spain today.

Asia-Pacific Markets End Mixed on Thursday

Asia-Pacific indices finished mixed on Thursday, weighed down by rising treasury yields and oil prices in the U.S. In the meantime, shares of Chinese property developer Evergrande were suspended on the Hang Seng Index today following the news of its chairman being under police surveillance. The news dragged down the stocks of major real estate firms.

Hong Kong’s Hang Seng index ended lower by 1.41%, while China’s Shanghai Composite and Shenzhen Component indices ended up by 0.10% and 0.05%, respectively.

Conversely, Japan’s Nikkei and Topix indices finished lower by 1.54% and 1.43%, respectively.

Unlock all the tools you need to get through the market uncertainty with 40% off Premium!