Soliton, a medical devices company, reported a fourth-quarter loss of $0.22 per share, narrower than analysts’ expectations for a loss of $0.23. However, the loss widened from the year-ago period’s loss of $0.20 per share due to higher operating expenses.

Soliton (SOLY) said that the rise in operating expenses in 4Q was primarily due to higher general and administrative as well as sales and marketing expenses.

Meanwhile, on March 2, the company named its Rapid Acoustic Pulse (RAP) device “RESONIC”, and said that the commercialization of the device is expected to begin in 2Q. In February, it announced that its RAP device has received 510(k) clearance from the FDA [Food and Drug Administration] for cellulite indication.

Last week, Soliton’s CEO Brad Hauser said, “We expect RESONIC to be a gamechanger in the removal of tattoos and improvement in cellulite appearance and believe the RESONIC brand captures our innovation; giving patients the opportunity to reimagine themselves without their tattoo or with greatly improved cellulite.”

During the earnings call, Hauser said, “Our recent 510(k) clearance for the short-term improvement in the appearance of cellulite marks a sizable expansion to the addressable market for our RAP technology.” He added, “We believe the cellulite remains one of the largest unmet aesthetics and a market in which we can deliver strong value to our shareholders.” (See Soliton stock analysis on TipRanks)

Following the results, Maxim Group analyst Anthony Vendetti said, “Before the end of March 2021, we expect SOLY to file a Special 510(k) application with the FDA for RAP (rapid acoustic pulse) system upgrades, with no alterations to the therapy. We expect clearance by the end of April 2021.” Vendetti added, “We also expect Soliton to launch its RAP device for both tattoo and cellulite indications to 25 KOLs (key opinion leaders) in 2Q21, followed by a full commercial launch in 2022.”

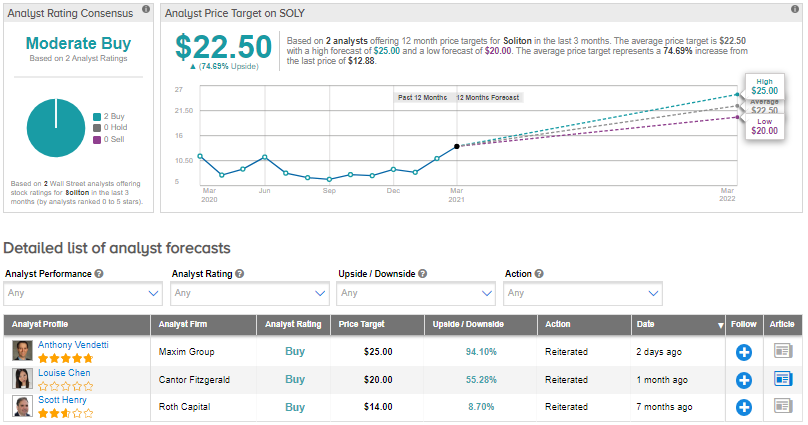

Vendetti maintained a Buy rating and a price target of $25 (94% upside potential) on the stock, “due to the significant growth potential in the tattoo removal and cellulite reduction markets,” the analyst said in a note to investors.

Overall, consensus among analysts is a Moderate Buy based on 2 unanimous Buys. The average analyst price target of $22.50 implies upside potential of about 75% to current levels. Shares have gained around 3.5% over the past year.

Related News:

Burlington Pops 11% As 4Q Sales Outperform Estimates

Costco’s 2Q Sales Soar 15% On E-Commerce Boom; Street Is Bullish

Gap Rises 4% On 4Q Profit Beat