Data Cloud company Snowflake (NYSE: SNOW) has reported a loss in the fourth quarter of its Fiscal 2022 (ended January 31) despite revenues beating analysts’ expectations. Additionally, the company disappointed investors regarding its guidance on revenue.

Following the update, shares of the company fell over 22% in extended trading on Wednesday.

Results in Detail

Snowflake incurred a loss of $0.43 per share, compared with the Street’s earnings estimate of $0.02 per share. The company reported a loss of $0.70 per share in the same quarter last year.

Total revenues generated during the quarter jumped 101% year-over-year and stood at $383.8 million, surpassing the consensus estimate of $372.7 million. A significant rise of 102% in product revenue of $359.6 million acted as a tailwind.

Adjusted product gross margin came in at 74.99%, up 500 basis points on a year-over-year basis.

Exiting the fourth quarter, remaining performance obligations were $2.6 billion, up 99% year-over-year. As of January 31, 2022, the net revenue retention rate was 178%, while the company has 5,944 total customers and 184 customers, with a trailing 12-month product revenue of more than $1 million.

Fiscal 2022 Results

For the year, Snowflake recorded a loss of $2.26 per share, compared with the loss of $3.81 per share reported in Fiscal 2021. Total revenues more than doubled on a year-over-year basis to $1.22 billion, including product revenue of $1.14 billion, up 106%.

Adjusted free cash flow stood at $149.8 million, compared with the negative free cash flow of $71.6 million in Fiscal 2021.

Snowflake exited the year with around $5.1 billion in cash, cash equivalents, and short-term and long-term investments.

Guidance

For Fiscal Q1 2023, the company forecasts product revenue in the range of $383-$388 million, representing 79% to 81% year-over-year growth. The consensus estimate is pegged at $410 million.

For Fiscal 2023, product revenue is expected between $1.88 billion and $1.9 billion, representing year-over-year growth of 65% to 67%. The guidance fell short of analysts’ expectations of $2 billion.

Continuing with product improvements, management has planned to roll out platform improvements this year within its cloud deployments. Consequently, around $97 million in impacts on full-year revenue is expected.

Other Developments

Snowflake has inked a deal to acquire Streamlit, a framework built to simplify and accelerate the creation of data applications. Financial details were kept under wraps.

Through this strategic acquisition, pending certain approvals, the two companies aim to discover the unrealized potential of data and develop beautiful applications easily.

Wall Street’s Take

The Street is cautiously optimistic about the stock and has a Moderate Buy consensus rating based on 17 Buys and six Holds. The average Snowflake price target of $384.93 implies 45.43% upside potential from current levels. Shares have increased 7.15% over the past year.

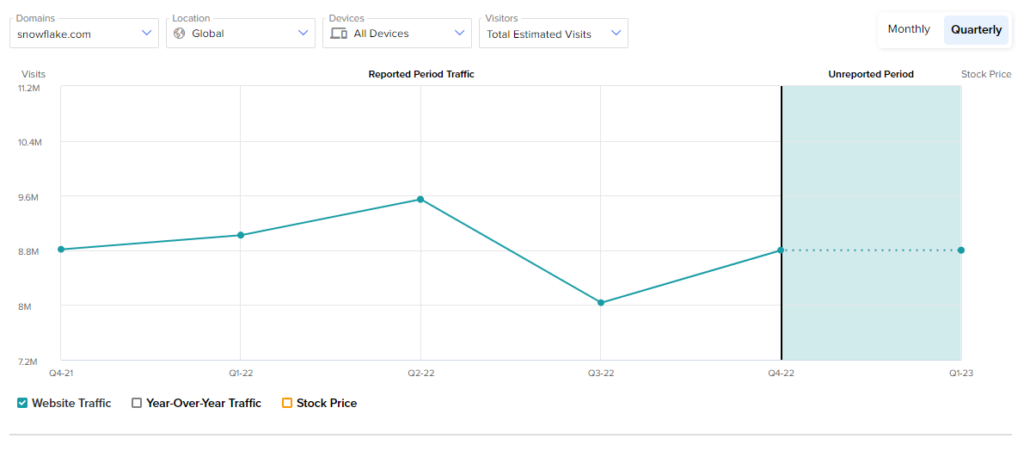

Website Traffic

The earnings results were corroborated with TipRanks’ new tool that measures visits to Snowflake’s website. Pre-earnings, we were able to see insights into Snowflake’s performance in the January quarter.

According to the tool, a website traffic uptrend was visible. In Fiscal Q4 2022, total estimated visits on snowflake.com showed an increasing trend, on a global basis, representing a 9.54% jump from the third quarter. This, in turn, indicated that the company might report strong revenues in the reported quarter.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

AMC Entertainment Books Smaller-than-Feared Q4 Loss

Baidu Posts Upbeat Q4 Results; Shares Jump 7%

DexCom Granted FDA Breakthrough Designation for Hospital CGM System