Shares of Slack Technologies dived 18.7% in Tuesday extended market session after the company reported lower-than-expected 2Q billings, a key indicator for future revenues. The cloud-based business solution provider’s 2Q billings amounted to $218.2 million, while analysts had forecast $232.9 million.

Meanwhile, Slack Technologies’ (WORK) 2Q revenues grew 49% to $215.9 million, surpassing analysts’ expectations of $208.3 million. The company posted break-even earnings for the quarter, which compared favorably with Street estimates of a loss per share of $0.03 as well as the year-ago quarterly loss of $0.14.

Slack raised its fiscal 2021 outlook. The company now forecasts revenues between $870 million and $876 million, up from the previously guided range of $855-$870 million. It lowered its fiscal 2021 loss per share guidance to $0.13-$0.14 from $0.17-$0.19 previously. For 3Q, the company projects revenues between $222 million and $225 million and expects to report a loss per share in the range of $0.05-$0.06. (See WORK stock analysis on TipRanks).

Ahead of the earnings report, Robert W. Baird analyst William Power reaffirmed his Buy rating on the stock with a price target of $37 (26.2% upside potential), citing positive risk/reward for the company. In a note to investors, Power wrote this month that he expects ongoing digital transformations to drive strong growth for Slack.

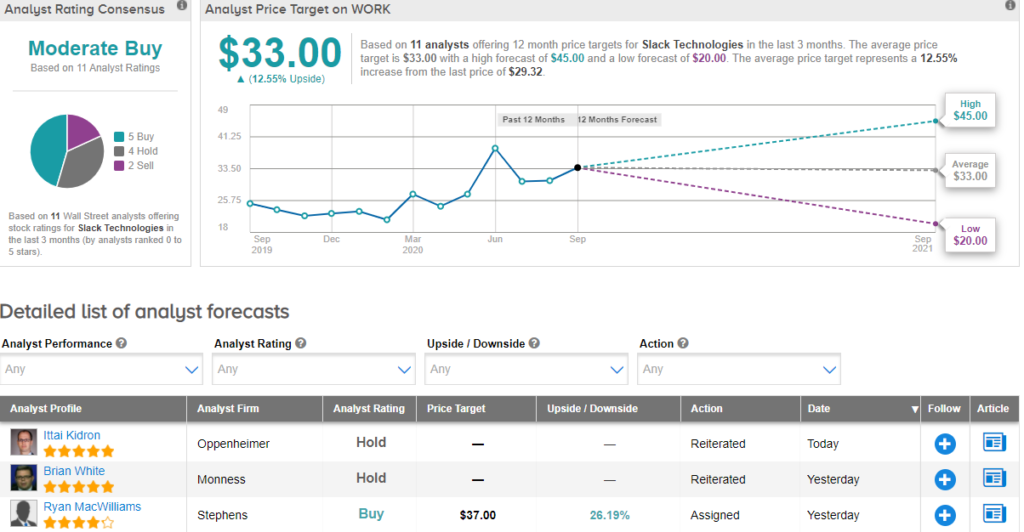

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 5 Buys, 4 Holds, and 2 Sells. With shares up over 30% so far this year, the average price target of $33 still implies further upside potential of about 12.6%.

Related News:

Microsoft Unveils Xbox Series S Gaming Console At $299

Google Scraps Plan To Rent Large Office Space In Dublin – Report

Disney’s Streaming App Downloads Jump 68% On ‘Mulan’ Debut – Report