RingCentral delivered better-than-expected fourth-quarter results, as both earnings and sales topped the Street’s estimates. The cloud communications company also forecasted 1Q and 2021 guidance that came in ahead of analysts’ estimates. Despite the outperformance, the stock fell 3% in Tuesday’s extended trading.

RingCentral’s (RNG) 4Q earnings of $0.29 per share beat the consensus estimates of $0.27 per share and grew 31.8% year-over-year. The company’s 4Q revenues rose about 32% year-over-year to $335 million and topped the Street’s estimates of $317.4 million.

The company’s subscriptions revenues, which accounted for 92% of total revenue, rose 34% year-over-year to over $306 million. Other revenue of $28 million grew 20% year-over-year, driven by growing demand for RingCentral apps amid the “work from anywhere” environment.

The company’s CEO Vlad Shmunis said, “Fourth quarter was outstanding, driven by robust growth across the business with strong contributions from the channel and our key partners led by Avaya, AT&T, and Atos.”

As for 1Q, RingCentral expects to generate EPS in the range of $0.24-$0.25 per share, topping the consensus estimates of $0.23 per share. The company anticipates 1Q revenues in the range of $337-340 million, compared to analysts’ estimates of $329.7 million.

For 2021, RingCentral foresees EPS in the range of $1.20-$1.24 per share, compared to the consensus estimates of $1.17 per share. Revenues are forecasted in the range of $1.475-1.490 million. Analysts were looking for revenues of $1.44 million in 2021. (See RingCentral stock analysis on TipRanks).

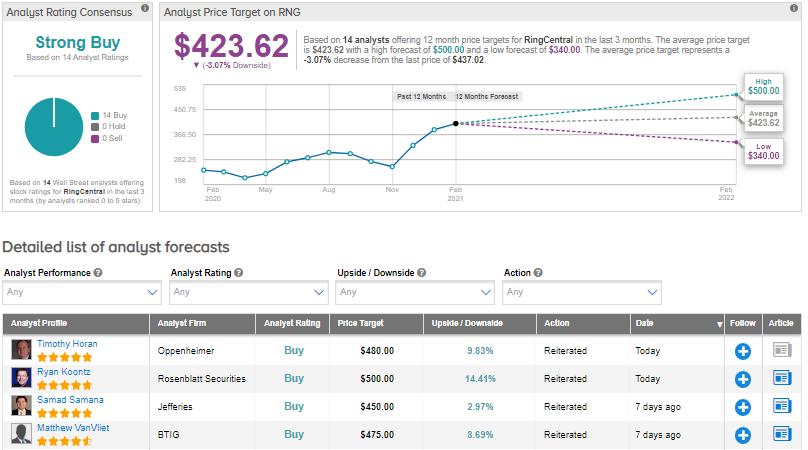

Following the strong results, Oppenheimer analyst Timothy Horan raised the stock’s price target to $480 (9.8% upside potential) from $450 and maintained a Buy rating.

In a note to investors, the analyst said, “The 4Q:2020 results show continuing acceleration of the business, ramping channel and large Telco partners’ activity, and record profits. RingCentral’s 4Q:2020 results should dispel any lingering investor concerns that demand was pulled forward during the 1H:2020 shutdowns and not sustainable.”

Horan added, “we believe RNG shares have decent valuation support with estimates mostly derisked by conservative guidance, the business acceleration, and good growth catalysts expected next year.”

Overall, consensus among analysts is a Strong Buy based on 14 unanimous Buys. Following the past year’s 80.3% share rally, the average analyst price target of $423.62 now implies downside potential of about 3.1% to current levels, given the

Related News:

Sabre Incurs 4Q Loss As COVID-19 Hurts Sales

IPG Photonics Posts Profit In Fourth Quarter; Shares Gain

Denny’s 4Q Revenues Miss Estimates Due To COVID-19 Pandemic