Peloton Interactive’s 2Q earnings and revenues topped the Street’s estimates. The company also raised its sales outlook for fiscal 2021. However, shares of the fitness products maker dropped about 5.9% on Feb. 5 due to continued delay in product deliveries, which resulted in “significant carry-over of undelivered product” into the third quarter.

Peloton (PTON) said, “The ongoing COVID-19 pandemic continues to present a challenging operating landscape, and we continue to work to address long order-to-delivery timeframes.”

The company expects to invest over $100 million in air freight and expedited ocean freight over the next six months to help improve deliveries.

During 2Q, the company posted adjusted earnings of $0.18 per share compared to a loss of $0.20 per share in the year-ago period. Analysts were looking for $0.09 per share. Peloton’s 2Q revenues of $1.06 billion exceeded the Street consensus of $1.03 billion and spiked 128% year-over-year, driven by continued strong demand for its fitness products and services.

The company’s connected fitness subscriptions grew 134% to approximately 1.67 million at the end of the quarter, while paid digital subscriptions jumped 472% to about 625,000. Total members reached over 4.4 million at the end of 2Q ending on Dec. 31.

For 3Q, Peloton forecasted for revenues to generate $1.10 billion compared to analysts’ estimates of $1.09 billion.

As for fiscal 2021, Peloton raised its sales guidance to over $4.075 billion versus analysts’ expectations of $3.95 billion. Earlier, the company had anticipated fiscal 2021 revenue of $3.9 billion or more.

In a letter to shareholders, Peloton said, “Our revised forecast anticipates slow but steady progress in narrowing our order-to-delivery windows over the remainder of the fiscal year.” (See Peloton stock analysis on TipRanks).

Following the earnings results, Stifel Nicolaus analyst Scott Devitt maintained a price target of $170 (14.6% upside potential) and a Buy rating on the stock.

“Elevated demand and shipping congestion at ports continue to cause delivery delays for the company’s products,” Devitt wrote in a note to investors. “Peloton is investing an incremental $100mm in expedited shipping which should lead to normalized order-to-delivery times by the end of FY21. With a path to normalized delivery and growing manufacturing capacity, Peloton is well positioned to deliver strong growth through the balance of the fiscal year.”

For the long term, the analyst said, “we continue to see a number of opportunities to support sustainable growth as the company expands its product line, develops broader fitness content and enters into new geographies.”

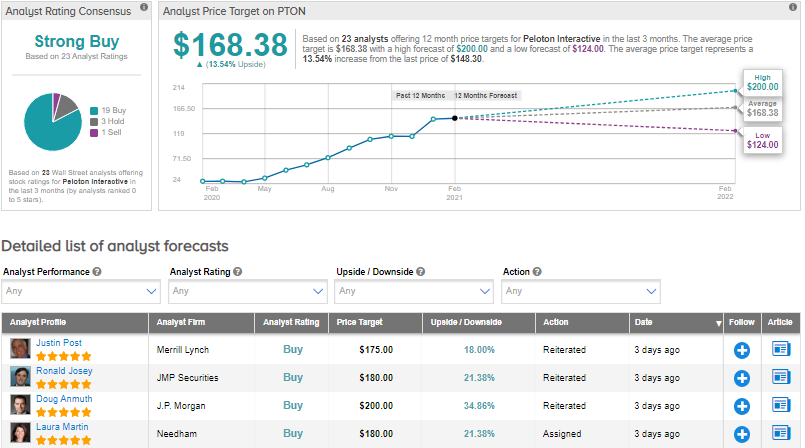

Overall, consensus among analysts is a Strong Buy based on 19 Buys, 3 Holds and 1 Sell. The average analyst price target of $168.38 implies upside potential of about 13.5% to current levels. Shares have rallied by over 343% over the past year.

Related News:

Illinois Tool’s ‘Record’ Operating Margin Drives 4Q Profit Beat

Linde’s 1Q Profit Outlook Tops Estimates After 4Q Beat; Shares Gain

Trane Technologies’ Productivity Savings Fuel 4Q Profit Beat