Shares of Peloton Interactive (NASDAQ: PTON) dropped 3.5% on January 18 to close near its 52-week low of $29.11, after the American exercise equipment and media company hired management consulting group McKinsey & Co to review its cost structure and potentially cut certain jobs, according to CNBC.

Markedly, shares of the company that had risen 5 times in 2020, lost 80% over the past year.

Beginning of a Slowdown Last Year

The company witnessed a huge upsurge in demand at the start of the COVID-19 pandemic and made incremental investments thereon. However, the rocketing demand didn’t sustain as customers returned to the gym and opted for other fitness options.

As a result, in November 2021, company CFO Jill Woodworth indicated that Peloton was planning to lower costs keeping in mind the slowdown in revenue growth as well as new subscriptions.

Likewise, the company announced a hiring freeze in November after doubling its employee strength to over 6,500 people compared to the prior year. The company had also stated that it would consider optimizing its marketing spending as well as curbing showroom development.

However, the company has been suffering losses and does not foresee turning to profitability till fiscal 2023.

In the quarter ended September 30, Peloton added only 161,000 connected fitness subscribers, the lowest addition recorded in the eight consecutive quarters. Furthermore, revenues only grew 6% year over year compared to a whopping 250% seen in the prior-year quarter of 2020.

The Possible Road Ahead: More Expensive Bikes, Job Cuts

Due to historically-high inflation levels and increased supply chain costs, the company may increase the fees related to the delivery and assembly of its Bike and Tread products. Consequentially, the cost of the products may go up by around 15% approximately.

By passing on the increased costs to the customers, Peloton plans to improve its profitability that has been impacted by the costs as well as slower sales.

According to CNBC, there could be a potential cut in jobs, especially in the apparel division, which has reported weak sales recently.

Additionally, Peloton could consider store closures. As of June 30, Peloton had 123 showrooms, in the U.S., Canada, the U.K., and Germany.

Management Comments

Ahead of its upcoming earnings scheduled for February 8, Peloton’s chief marketing and communications officer, Dara Treseder, said, “Right now, people are raising prices. Ikea just raised prices. We want to go in the middle of the pack.”

Wall Street’s Take

Following the news, Evercore ISI analyst Shweta Khajuria maintained a Hold rating on the stock with a price target of $72 (138.2% upside potential).

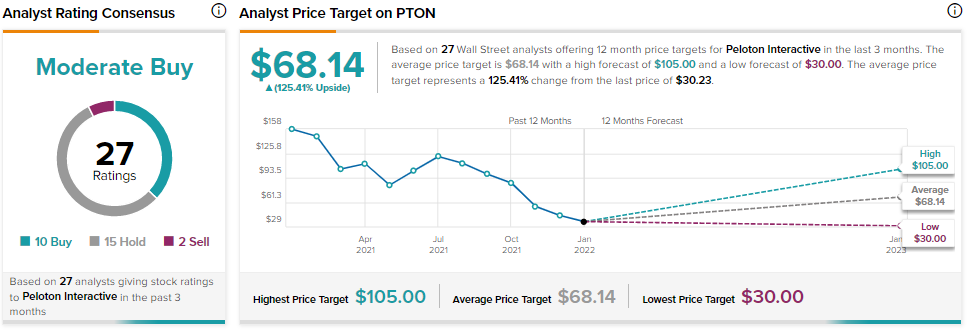

The Wall Street community is cautiously optimistic about the stock, with a Moderate Buy consensus rating based on 10 Buys, 15 Holds and 2 Sells. The average Peloton Interactive stock forecast of $68.14 implies 125.4% upside potential to current levels.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

Bank of New York Beats Q4 Expectations

Kirkland Lake Gold Reports Strong Q4 & FY2022 Production

Ford Hires Stripe to Boost its E-commerce Plans