Shares of Okta Inc. fell 10.4% in Wednesday’s extended trading session, as the cloud-based enterprise identity-management platform provider disappointed investors with wider-than-expected loss guidance for 1Q and FY22.

Meanwhile, Okta’s 4Q results (ending Jan. 31, 2021) came in higher than analysts’ expectations and revenue guidance also topped estimates.

Okta (OKTA) reported 4Q earnings of $0.06 per share, compared to the Street’s expectations for a loss of $0.01 per share. Notably, the company reported a loss of $0.01 per share in the year-ago period.

Revenues of $234.7 million jumped 40% year-over-year and exceeded consensus estimates of $221.9 million. Subscription revenue grew 42% year-over-year to $225.4 million.

The company’s CFO Bill Losch said, “We were particularly pleased with the continued strength in RPO [Remaining Performance Obligations], revenue, and cash flows, which reflects the success we’ve experienced with large enterprise customers.”

Despite upbeat 4Q results, the company’s guidance failed to impress investors. For 1Q, the company expects a loss in the range of $0.20-$0.21 per share, significantly wider than the Street’s expectations for a loss of $0.07 per share. Moreover, for fiscal 2022 (ending Jan. 2022), Okta forecasts a loss of $0.44-$0.49 per share versus analysts’ expectations for earnings of $0.01 per share.

The company projects revenues in the range of $237-$239 million for 1Q, with the midpoint being higher than consensus estimates of $237.3 million. For fiscal 2022, the company anticipates revenues of between $1.08 and $1.09 billion, topping the Street’s estimates of $1.07 billion. (See Okta stock analysis )

Along with the 4Q results, Okta announced the acquisition of peer Auth0 for $6.5 billion in stock. The company expects the stock deal to close in the second quarter ending July 31. It expects the deal to “accelerate the companies’ shared vision of enabling everyone to safely use any technology, shaping the future of identity on the internet.”

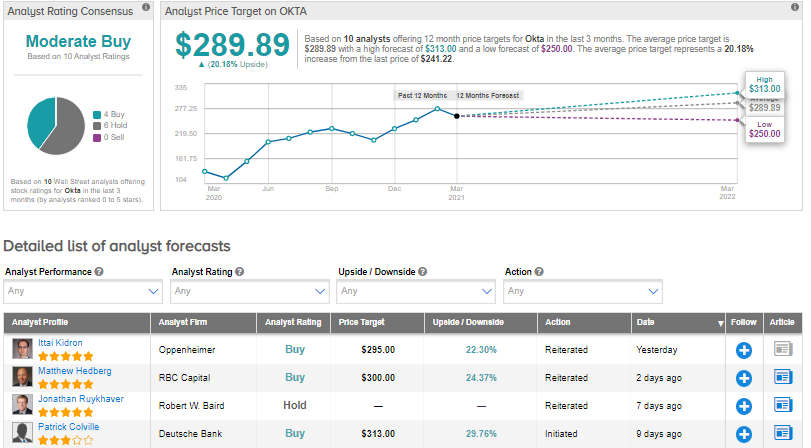

Following the results, Oppenheimer analyst Ittai Kidron maintained a Buy rating and a price target of $295 (22% upside potential).

In a note to investors, Kidron said, “While initial guidance for FY22 points to a significant deceleration in growth (down to ~30% YoY), we believe the underlying demand drivers remain strong/unchanged (Cloud, Zero Trust, digital transformation) and that management is being prudent given the macro environment.” As for the Auth0 acquisition, Kidron sees “synergies ahead.”

Turning now to the rest of the Wall Street community, Okta has a Moderate Buy consensus rating based on 4 Buys and 6 Holds. The average analyst price target of $289.89 implies over 20% upside from current levels. Shares have gained 81% over the past 12 months.

Related News:

Ross Stores Disappoints With Weak 1Q EPS Outlook; Stock Drops

Box’s 4Q Profit Soars 214%; Street Sees 14% Upside

Ambarella Pops 8% On Upbeat Outlook, 4Q Earnings Beat