NexTier Oilfield Solutions posted a lower-than-expected loss in the fourth quarter, driven by a rise in activity growth across all product and service lines along with continued strong operational performance. Shares of the oilfield service company are up over 15% year-to-date.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

However, NexTier’s (NEX) business still grapples with continued inefficiencies in calendar utilization. The company incurred a non-GAAP loss of $0.30 per share in 4Q, compared with the $0.34 loss per share estimated by analysts. Total sales generated in the quarter amounted to $215.1 million, above analysts’ expectations of $193.73 million.

Meanwhile, revenue at NexTier’s Completion Services unit, surged 30.2% sequentially to $200.5 million. The Well Construction and Intervention (WC&I) Services segment recorded revenue of $14.6 million, up 50.5% from the previous quarter.

The company reported an adjusted EBITDA of $7.7 million, compared with a $2.4 million loss posted in the prior quarter. NexTier averaged 17 deployed and 14 fully-utilized fleets in the quarter compared with 13 deployed and 11 fully-utilized fleets in the third quarter. (See NexTier stock analysis on TipRanks)

NexTier CEO Robert Drummond said, “Because of our leading service quality and market readiness program, we have nearly tripled deployed fleets since late June with minimal start-up costs and record safety and operational performance. Looking ahead, we anticipate a more constructive supply and demand balance and improved calendar efficiency as global demand, and call on U.S. shale, returns, setting the stage for a more favorable earnings climate in the second half of 2021 and beyond.”

For the first quarter of 2021, NexTier anticipates 18 deployed and 15 fully-utilized fleets. Revenue is expected to record a sequential increase of 5-10%. Adjusted EBITDA is forecasted in the range of $5 million to $10 million.

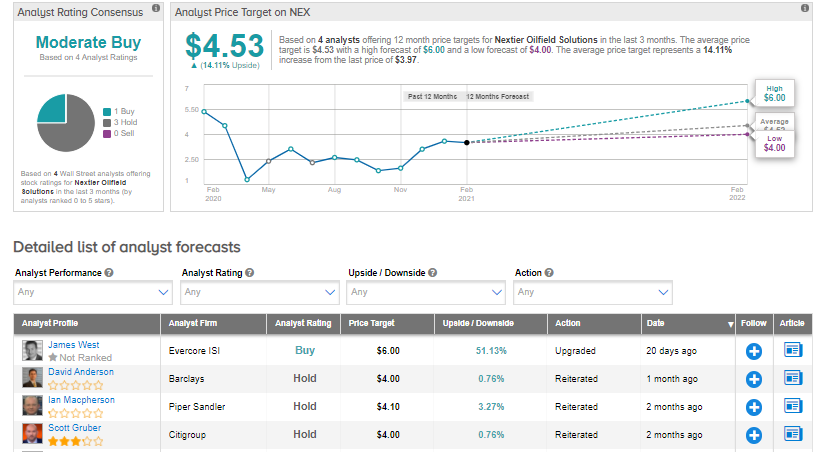

On Jan. 27, Evercore ISI analyst James West upgraded the stock to Buy from Hold and increased the price target to $6 (51.1% upside potential) from $4. In a note to investors, the analyst said that the North American, and particularly the U.S Land stimulation market, is “quickly tightening and may soon reach the threshold for pricing improvements.”

The rest of the Street is cautiously optimistic about the stock. The Moderate Buy consensus rating is based on 3 Holds vs. 1 Buy. The average analyst price target stands at $4.53 and implies upside potential of about 14.1% to current levels over the next 12 months. Shares have gained 66.1% over the past six months.

Related News:

Lincoln Electric Posts Better-Than-Expected Quarterly Profit; Street Sees 5% Upside

Chemours Quarterly Earnings Outperform; Shares Gain 3.3%

Coca-Cola Posts Better-Than-Expected Quarterly Profit; Street Sees 14% Upside