Needham increased Electronic Arts’ price target to $165 (22% upside potential) from $150 and reiterated a Buy rating citing strong growth prospects in the video gaming industry.

Needham analyst Laura Martin wrote in a note on Tuesday that Electronic Arts’ (EA) “ongoing pivot toward annuity revenue streams as well as the rapidly accelerating video game industry growth with higher Lifetime Customer Value, or LTV, during the COVID-19 outbreak.” Martin added that the company is “benefiting over the near and the long-term from the rapid rise in hours played, more new games tried, higher in-game spending, and limited competition from live sports during the pandemic.”

On July 31, Electronic Arts reported that 1Q revenues grew 20.7% to $1.46 million year-on-year, beating the Street consensus of $1.05 billion. The company’s non-GAAP EPS of $1.42 also compared favorably with $0.25 reported in the year-ago quarter, surpassed Street estimates of $0.79.

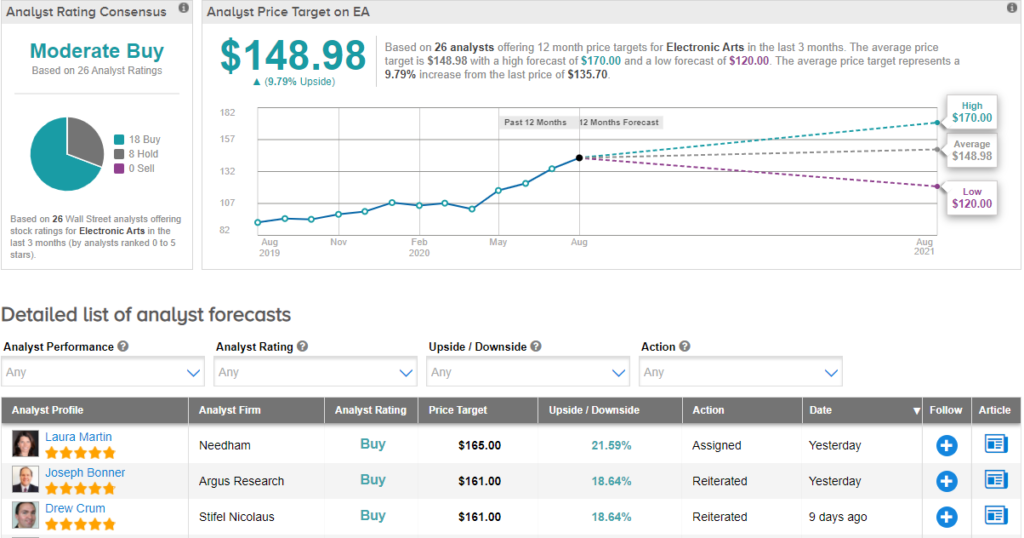

Currently, the Street has a cautiously optimistic outlook on the stock. The Moderate Buy analyst consensus is based on 18 Buys versus 8 Holds. The average analyst price target of $148.98 implies an upside potential of 9.8%. (See EA stock analysis on TipRanks).

Related News:

Rosenblatt Lifts ON Semiconductor’s PT Amid Gross Margin Outlook

William Blair Raises Kforce To Buy After 2Q Profit Beat

Susquehanna Turns Bullish On MercadoLibre, Doubles PT