Mercury Systems (MRCY) has acquired Pentek Technologies and Pentek Systems (collectively called Pentek) in an all-cash deal valued at approximately $65 million, subject to net working capital and net debt adjustments. Mercury Systems is a global technology company that serves the aerospace and defense industry.

The buyout was funded through a mix of cash and the existing revolving credit facility of Mercury.

Pentek designs and manufactures software-defined radio and data acquisition boards, recording systems, and subsystems for high-end commercial and defense applications. The addition of Pentek’s capabilities will complement Mercury Systems’ product portfolio and expand its reach in core radar and electronic warfare/SIGINT markets.

Furthermore, the deal is likely to be immediately accretive to the company’s adjusted EPS and Pentek is expected to generate around $20 million in revenue for Mercury’s Fiscal Year ending July 1, 2022.

Mercury Systems CEO Mark Aslett said, “The acquisition of Pentek is an excellent fit for our market and low-risk content expansion strategy.”

He added, “Their capabilities add scale and breadth to Mercury’s existing mixed-signal product portfolio and deepen our penetration into our core radar, electronic warfare (EW), and signals intelligence markets. Like our previous acquisitions in the RF and microwave domain, the acquisition of Pentek doesn’t just provide important new capabilities for our customers; it also enables us to grow the size of our total addressable market.” (See Mercury Systems stock analysis on TipRanks)

On May 6, Jefferies analyst Sheila Kahyaoglu upgraded the stock to Buy from Hold and maintained a price target of $80 (21.8% upside potential).

Kahyaoglu said, “Despite near term timing delays in larger programs, the HSD-LDD organic growth outlook remains intact with 8% organic growth expected in FY22-FY24 with support from tech refreshes and the growing EW business.”

Consensus among analysts is a Strong Buy based on 3 Buys versus 1 Hold. The average analyst price target stands at $81.50 and implies upside potential of 24.1% to current levels. Shares have lost 7.8% over the past six months.

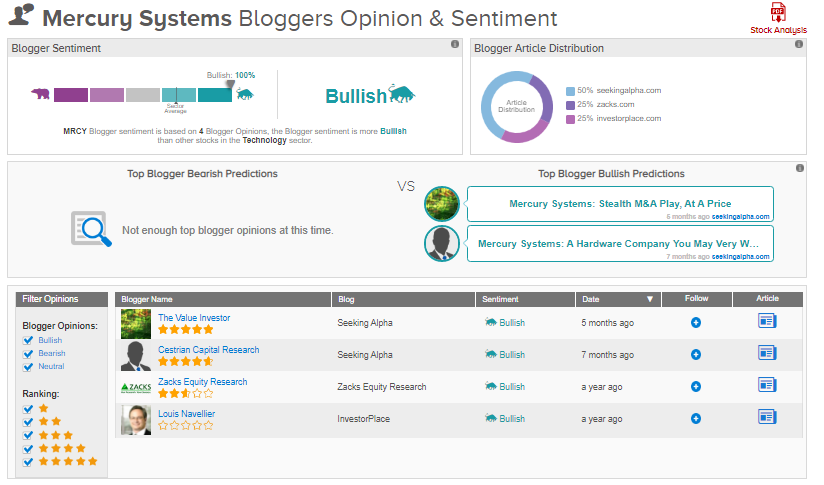

TipRanks data shows that financial blogger opinions are 100% Bullish on MRCY, compared to a sector average of 69%.

Related News :

Workday Beats Analysts’ Expectations in Q1; Shares Down

Abercrombie & Fitch Delivers Strong Q1 Results; Shares Pop 8%

Garmin Expands Digital & Aviation Offerings with AeroData Buyout