Medtronic announced restructuring plans to cut annual costs by $450 million – $475 million by fiscal 2023 as the medical device maker introduces a new operating model to simplify its organizational structure.

Medtronic (MDT) said that the cost savings resulting from the new operating model are designed to enable reinvestment to drive future revenue growth and to strengthen the company’s ability to deliver strong long-term earnings per share growth. As part of the revamp, Medtronic is reorganizing its current business groups into operating units (OUs), each focused on specific therapy areas.

The “new operating model is designed to make the company a more nimble and competitive organization focused on accelerating innovation, enhancing the customer experience, driving revenue growth, and winning market share, while at the same time more efficiently and effectively leveraging its enterprise scale,” Medtronic announced in a SEC filing.

As a result of the restructuring program, the company expects to incur total pre-tax costs of approximately $400 million – $450 million, the majority of which will be recognized by the end of fiscal year 2022.

Medtronic plans to transition to this new model in its fiscal third quarter and said that it will be fully effective at the start of its fourth quarter of fiscal 2021. The company is also currently assessing the impact of these changes to the external reporting of its segments and may provide an update, if changes are necessary, prior to the start of its fiscal fourth quarter.

Moreover, Medtronic’s operations will be consolidated at the enterprise level – including the company’s global manufacturing, supply chain and facilities – to provide better service to the new OUs and better leverage the company’s enterprise scale to realize greater efficiencies and capitalize on its global reach, the company said.

Medtronic management will discuss its new operating model at its virtual Investor Day on October 14.

The medical device maker employs more than 90,000 people worldwide, serving physicians, hospitals and patients in more than 150 countries.

Medtronic shares have suffered greater losses earlier this year as many hospitals that use its medical devices had deferred elective procedures due to the coronavirus pandemic. The stock, which advanced 10% over the past month, is still down 5% on a year-to-date basis (See Medtronic stock analysis on TipRanks).

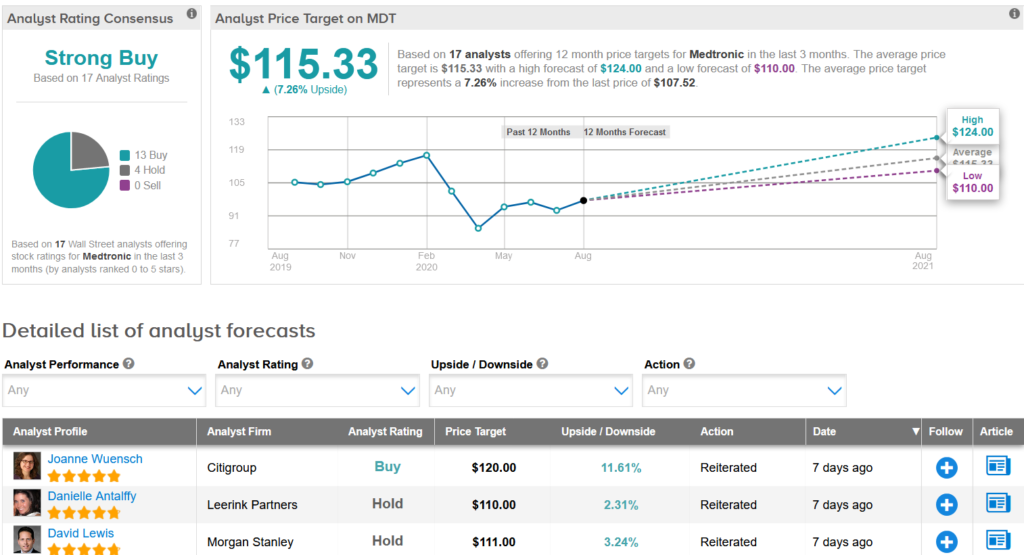

Oppenheimer analyst Steven Lichtman at the end last month raised the stock’s price target to $118 from $112 and reiterated a Buy rating, citing “recent peer multiple expansion”.

Commenting on the company’s revenue outlook, Lichtmann expects “sequential improvement in F2H21 with F4Q21 returning to more normalized revenue (mid-single-digit growth on two-year stacked basis) and margin levels (we forecast high-20’s op margin in F4Q)”.

“MDT remains on offense to drive top-line growth via tuck-in M&A and continued R&D reinvestment,” the analyst added. “MDT trades at a discount to peers on calendar 2021E P/E multiples (~19.5x versus ~22.5x).”

The rest of the Street shares Lichtmann’s bullish outlook on the stock. The Strong Buy analyst consensus boasts 13 Buy ratings versus 4 Hold ratings. The $115.33 average analyst price target implies 7.3% upside potential in the shares over the coming year.

Related News:

Medtronic’s First-Of-Its Kind Diabetes System For Young Children Approved

AstraZeneca Rises On Report Trump Could Fast-Track Covid-19 Vaccine Candidate

Abbott Expanding Its Covid-19 Test To Asymptomatic People- Report