Seattle-headquartered Accolade (ACCD) offers technology-driven healthcare solutions that connect people to the right care, reduce costs, and improve outcomes. Its solutions include mental health support, virtual primary care, and expert medical opinion services.

Accolade’s earnings report shows revenue increased 117% year-over-year to $85.3 million in Fiscal Q3 2022 ended November 30. The loss per share of $0.31 narrowed from $0.32 in the same quarter a year ago.

Accolade now serves more than 10 million members compared to 2 million members only a year ago. The growth has been supported by the acquisitions of PlushCare and 2nd.MD. The company also recently launched new healthcare solutions named Accolade Care and Accolade One, which have boosted its capabilities of offering end-to-end care. For Q4, Accolade anticipates revenue in the band of $90 million to $93 million. It raised its Fiscal 2022 full-year revenue expectation to a range of $306 million to $309 million, from $303 million to $307 million previously.

With this in mind, we used TipRanks to take a look at the risk factors for Accolade.

Risk Factors

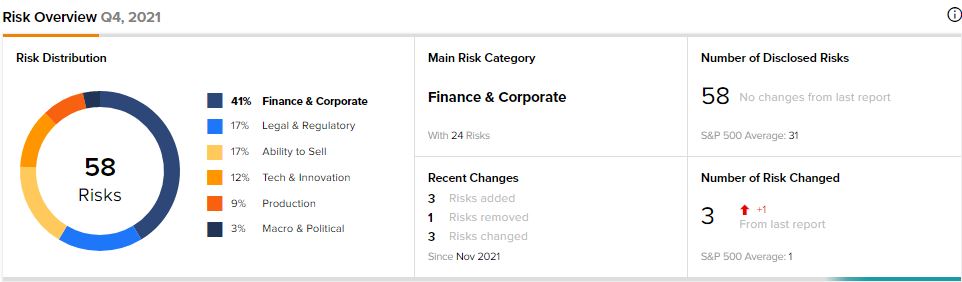

According to the new TipRanks Risk Factors tool, Accolade’s main risk category is Finance and Corporate, representing 41% of the total 58 risks identified for the stock. Legal and Regulatory and Ability to Sell are the next two major risk categories, each accounting for 17% of the total risks. The company has recently adjusted its risk profile, adding new risk factors, removing some, and updating others.

In a newly added Ability to Sell risk factor, Accolade informs investors that it has been sued in California over its automatic subscription fee renewal process. The lawsuit specifically targets its PlushCare unit. The company explains that in cases where subscription fees automatically renew without requiring further action by the subscriber, some state and federal laws require disclosure to subscribers. The California lawsuit seeks damages and restitution for automatically renewed subscription fees. Accolade says it will vigorously defend itself against the lawsuit. But it warns that if it is required to change its automatic subscription fee renewal practice, its business and financial condition could be adversely impacted.

In another newly added risk factor, Accolade tells investors that it is spending significant resources to market its PlushCare services. It works with various marketing partners on these efforts. It cautions that the marketing efforts may become more expensive and adversely impact its overall business and cash flow. Accolade provides virtual primary care and mental health support through PlushCare, which now represents a significant portion of its business.

The company has dropped the risk factor that warned that its financial results could suffer a material adverse effect in relation to the convertible debt securities that it may need to settle in cash.

In an updated Finance and Corporate risk factor, Accolade reminds investors that it has identified a weakness in its internal controls over financial reporting. It warns that this could impair its ability to produce accurate financial statements or comply with regulations.

The Finance and Corporate risk factor’s sector average is 52%, compared to Accolade’s 41%. Accolade’s stock has declined 55% over the past year.

Analysts’ Take

Following Accolade’s Q3 earnings report, Piper Sandler analyst Jeff Garro reiterated a Buy rating on Accolade stock but lowered the price target to $35 from $45. Garro’s reduced price target still suggests 64.86% upside potential. The analyst sees strong fundamental drivers and likes the catalysts for the stock.

Consensus among analysts is a Strong Buy based on 10 Buys. The average Accolade price target of $38 implies 81.12% upside potential to current levels.

Download the TipRanks mobile app now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure.

Related News:

Boeing 737 Max Nearing Return to Service in China – Report

Monster Beverage Acquires CANarchy Craft Brewery for $330M

Taiwan Semiconductor Posts Q4 Beat & Robust Guidance; Shares Pop 5.3%