There’s a new wrinkle today in the drama triangle between ironSource (IS), Unity Software (U), and AppLovin (APP). Reportedly, Unity turned down a high-dollar buyout bid from AppLovin. This might be disappointing for AppLovin’s shareholders, but Wall Street is evidently bullish today on ironSource in the wake of the AppLovin bid rejection. I am neutral on all three of these stocks.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

As you might expect from the foregoing developments, AppLovin stock declined today while ironSource stock moved higher. IS stock is currently up 14%.

Unity Software provides a 3D content platform that’s often used to design video games and virtual reality experiences. Meanwhile, AppLovin’s business is to help mobile app developers market and monetize their apps. Israel-based ironSource has a similar business to AppLovin, as ironSource also offers a platform to help developers commercialize their apps.

All of this might sound like a soap opera, but it’s business as usual in the financial markets. At least for today, traders have chosen the winners and the losers among these three tech-focused names – and perhaps, there might be prime investment opportunities amid the ongoing drama.

AppLovin’s Unity Software Bid Makes the Headlines

Even highly successful businesses will inevitably face rejection from time to time. A case in point would be AppLovin. This company is an absolute monster in the mobile app industry. Just recently, AppLovin revealed that its second-quarter 2022 revenue grew 16% year-over-year to $776 million, driven to a large extent by a whopping 118% increase in Software Platform revenue.

So, AppLovin is doing fine financially and seems to envision rapid growth. AppLovin is currently “expanding the reach and use case of our Software Platform” and claims to own “the total mobile marketing experience.”

Yet, AppLovin’s business isn’t completely end-to-end in the app development life cycle. Surely, AppLovin would be glad to avail itself of Unity Software’s robust and popular 3D content platform. A business combination between AppLovin and Unity would create a redoubtable force in the broader mobile app market.

Thus, AppLovin took a big risk but undoubtedly envisioned high potential rewards when the company submitted a compelling, non-binding proposal to combine with Unity Software. This bid, while unsolicited, was a real headline grabber, as it would have had an estimated enterprise value of $20 billion.

The monetization potential could have been enormous. According to AppLovin’s estimates, the combined business could have targeted run-rate revenue exceeding $7 billion and run-rate adjusted EBITDA of greater than $3 billion by the end of 2024. Furthermore, AppLovin envisioned synergies of over $700 million in adjusted EBITDA in 2025 (estimated), with a minimum of $500 million in 2024.

Consider what a game changer it would have been if Unity’s board of directors had approved the proposed merger with AppLovin. Unity Software’s shareholders would still probably have had to approve the business combination as well, but chances are, they would have voted “yes.”

Unity Software Announces Its Rejection of AppLovin’s Buyout Proposal

Just imagine the shock and the disappointment for AppLovin’s investors if the company’s buyout bid for Unity Software didn’t even get to the shareholder approval stage. This is what actually just happened, though, and it’s having an immediate impact on the share prices of all three businesses mentioned here.

In a fresh press release that just came out this morning, Unity Software disclosed that its board of directors “completed a thorough financial and strategic evaluation of the unsolicited proposal from AppLovin.” Notice that Unity took the time to mention that the takeover bid was unsolicited. You can probably almost feel the rejection coming by this point.

Thus, Unity Software’s board determined that AppLovin’s proposal wouldn’t be “in the best interests of Unity shareholders and would not reasonably be expected to result in a Superior Proposal.” Superior to what? The answer is: Unity’s management is clearly convinced that AppLovin’s takeover bid isn’t superior to what ironSource would bring to the table in a potential business combination.

In a move that might stun some onlookers, Unity’s board recommended against AppLovin’s proposal while reaffirming its recommendation to Unity Software’s shareholders to vote in favor of a previously announced potential deal with ironSource. Unity Software President and CEO John Riccitiello made no bones about his company’s intentions, declaring that Unity’s board “continues to believe that the ironSource transaction is compelling.”

While AppLovin envisioned monumental monetization possibilities for a deal with Unity Software, Unity came up with its own estimates for a would-be business combination with ironSource. In particular, Unity Software expects that a combined business with ironSource would generate a run rate of $1 billion in adjusted EBITDA by the end of 2024, along with $300 million in annual EBITDA synergies by year three.

How does ironSource’s management feel about all of this, though? It appears that for now, at least, the positive feelings are mutual between Unity Software and ironSource. It almost seemed as if ironSource reveled in the AppLovin rejection, with ironSource asserting, “Unity’s rejection of AppLovin’s unilateral bid confirms the superior strategic value of the merger with ironSource.”

Actually, ironSource even disclosed a possible timeline for a deal with Unity. ironSource, according to a press release, “remains committed to completing this strategically and financially compelling combination in the fourth quarter of this year.” So, keep your eyes peeled for further developments in this ongoing story.

Is ironSource Stock a Buy?

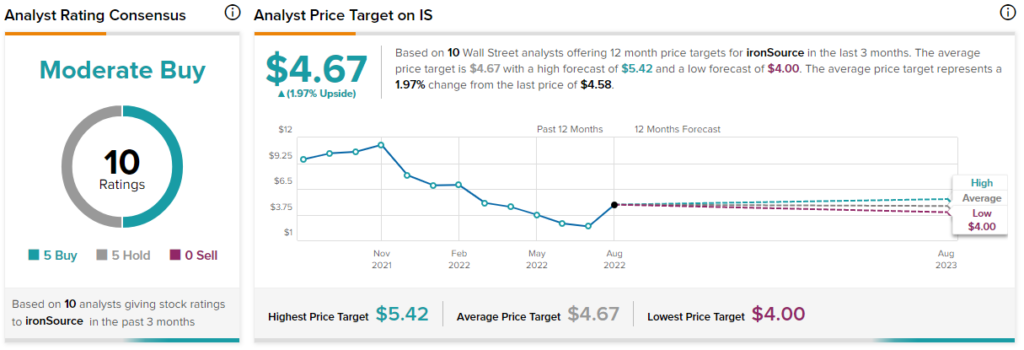

Turning to Wall Street, ironSource stock is a Moderate Buy based on five Buys and five Hold ratings. The average ironSource price target is $4.67, implying 2% upside potential.

Conclusion: Should You Consider ironSource Stock?

We can’t say that an agreement between Unity Software and ironSource is guaranteed to happen. Yet, the signs are definitely there, as both businesses have expressed interest while AppLovin is apparently out of the picture. Therefore, traders might consider taking a position in ironSource stock if they’re bullish on the prospect of a merger with Unity and on the fiscal synergy that could result if this business combination takes place.