Shares of Elastic N.V. are advancing more than 9% in Thursday’s pre-market trading after the company reported a smaller-than-expected 2Q loss. Moreover, the enterprise search and security company’s fiscal 2021 guidance also topped the Street’s estimates.

Elastic (ESTC) reported a 2Q loss of $0.03 per share, which was smaller than analysts’ estimates for a loss of $0.20 and compared to a year-ago loss of $0.22. Its 2Q revenue jumped 43% to $144.9 million and topped the Street’s consensus of $130.5 million. The company’s SaaS [Software as a service] sales grew 81% year-over-year to $37.4 million. Its subscription revenue, which represents 93% of total revenues, rose 46.4% to $134.2 million.

Looking ahead to 3Q, the company expects to report a loss in the range of $0.14-$0.16 per share, compared to analysts’ expectations for a loss of $0.28 per share. Elastic forecasts 3Q revenue of $145-147 million, versus the consensus estimates of $139.8 million.

For fiscal 2021, Elastic anticipates a loss per share in the range of $0.32-$0.40, versus the Street’s estimates for a loss of $0.71. The company projects FY21 revenue of $568-572 million, compared to analysts’ expectations of $548.8 million. (See ESTC stock analysis on TipRanks)

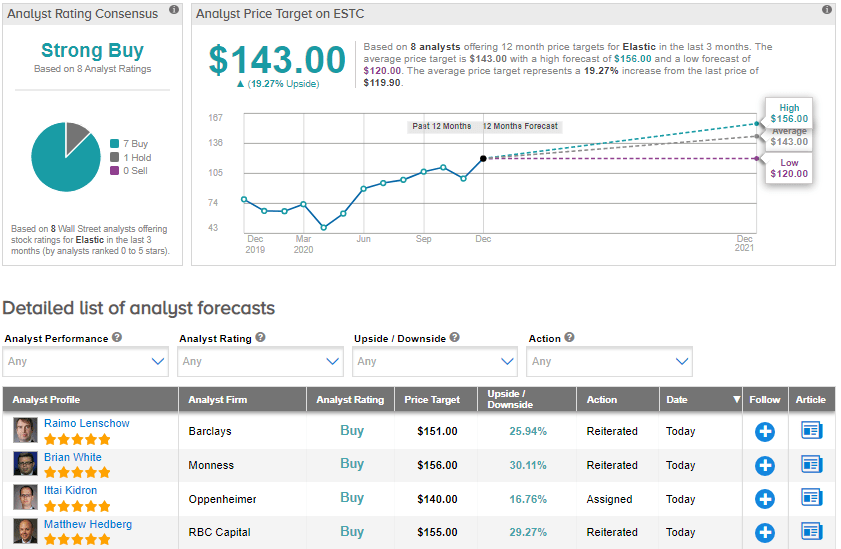

Following the results, Oppenheimer analyst Ittai Kidron assigned a Buy rating and a price target of $140 (16.8% upside potential) on the stock. Kidron noted that the upbeat 2Q results reflect “steady overall execution and broad-based product demand.” The analyst believes that the company’s raised 3Q and FY21 guidance “has room for upside given management’s careful approach for COVID-19/macro headwinds.”

Kidron expects the company to show “a strong long-term growth profile supported by wider use case adoption (APM, SIEM, endpoint security, etc.), low customer penetration, strong Elastic Cloud/SaaS growth (+81.3% in 2Q), and increasing go-to-market/eco-system leverage (salesforce additions, deep cloud partnerships, etc.).”

Like Kidron, most of the Street has a bullish outlook on the stock. The Strong Buy analyst consensus is based on 7 Buys and 1 Hold. The average price target stands at $143 and implies upside potential of about 19.3% to current levels. Shares have gained 86.5% year-to-date.

Related News:

PVH’s 3Q Profit Beats The Street; Guggenheim Lifts PT

Snowflake Posts Wider-Than-Expected 3Q Loss; Shares Slip 4%

Zscaler Lifts FY21 Outlook After Blowout 1Q; Shares Pop 12%