Advanced Micro Devices (AMD) shares rose about 5% in after-hours trading after the company held its 2025 Analyst Day on Tuesday. The chipmaker shared new growth targets and plans for its AI and data center business, drawing strong interest from Wall Street. Following the event, Mizuho Securities analyst Vijay Rakesh kept a Buy rating on the stock and raised his price target to $285 from $275, citing confidence in AMD’s long-term earnings outlook. The new price target implies 20% upside potential from current levels.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Rakesh is a five-star analyst on TipRanks, ranking #35 out of 10,109 analysts tracked. He has a 66% success rate and an impressive average return per rating of 30.50%.

AMD’s Analyst Day Points to Stronger Growth Path

Rakesh said AMD expects its revenue to grow more than 35% a year and sees gross margins rising to 55–58%, above the current 54%. The company also lifted its forecast for the AI hardware market to over $1 trillion by 2030, up from $500 billion previously.

AMD now expects data center revenue to grow by more than 60% a year, with AI-related sales climbing over 80% annually for the next few years. Management also set new goals for EPS above $20 by 2030, operating margins above 35%, and free cash flow margins around 25%.

Data Center and AI Products Lead the Way

The analyst said AMD’s next wave of data center chips should drive major growth. The company plans to launch its Helios servers with MI450 and Venice CPUs in 2026 and follow up with Verano CPUs and MI500X GPUs in 2027.

Rakesh believes these launches will boost AMD’s position in AI and help the company expand its x86 server share to over 50%, up from about 40% now.

He added that AMD’s guidance points to stronger EPYC CPU revenue, which could reach $27 billion by 2028, well ahead of market estimates.

PC and Embedded Segments Add Support

Rakesh also noted that AMD aims to gain a bigger share in PCs and embedded markets. The company is targeting over 40% of the x86 PC market by 2030, up from around 28% today. In its embedded segment, AMD has secured $36 billion in design wins since 2022, including $15 billion from auto, aerospace, and wireless clients.

He said AMD expects its embedded business to grow at twice the pace of the market, helped by steady gains in FPGA (Field-Programmable Gate Array) products, where it already holds more than half the market share.

Notably, FPGAs are special computer chips that can be reprogrammed after manufacturing to perform different tasks.

On the valuation front, AMD trades at about 42 times 2026 earnings, slightly higher than peers like Nvidia (NVDA) and Broadcom (AVGO). He said the premium is fair, given AMD’s faster profit growth and rising AI data center revenue.

Is AMD a Buy or Sell Now?

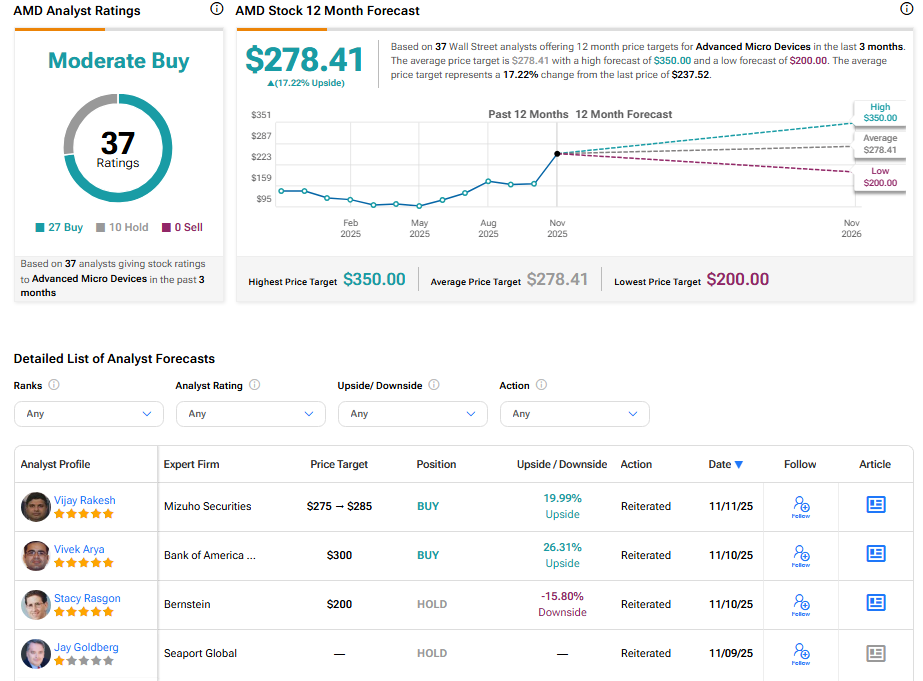

Turning to Wall Street, AMD stock has a Moderate Buy consensus rating based on 27 Buys and 10 Holds assigned in the last three months. At $278.41, the average AMD price target implies a 17.22% upside potential.