Dollar Tree delivered robust sales growth across both of its banners – Family Dollar and Dollar Tree, in 3Q FY20 (ended Oct. 31) as value deals continued to attract customers. The discount retailer delivered sales of $6.18 billion, which exceeded analysts’ estimate of $6.13 billion. Shares rose 14.1% on Tuesday in reaction to the results, bringing the year-to-date rise to 18.5%.

The 3Q sales grew 7.5% year-over-year, driven by same-store sales growth of 5.1%. Same-store sales for the Family Dollar banner grew 6.4% while the growth rate for the Dollar Tree banner was 4%. Dollar Tree’s (DLTR) 3Q EPS increased 28.7% year-over-year to $1.39, beating the Street’s expectation of $1.15. Significant expansion in gross margin and operating margin fueled the earnings growth.

The company’s efforts over the past few years to optimize its stores, especially Family Dollar stores, and enhance its merchandise offerings are driving its performance in the current crisis. Last year, Dollar Tree began testing a multi-price concept referred to as Dollar Tree Plus! in over 100 stores in southwestern markets in the U.S. It now plans to expand this initiative into 500 stores beginning in the spring of 2021. (See DLTR stock analysis on TipRanks)

Looking ahead, CEO Mike Witynski commented, “It’s an exciting time at Dollar Tree. We are just over three weeks into our important fourth quarter and we are off to a very good start, with same-store sales at both banners currently tracking above reported third quarter levels. Our focus will continue to be on opening new stores, refining our store formats and upgrading our assortments to drive improved store productivity, increasing operating efficiencies, generating free cash flow and buying back shares.”

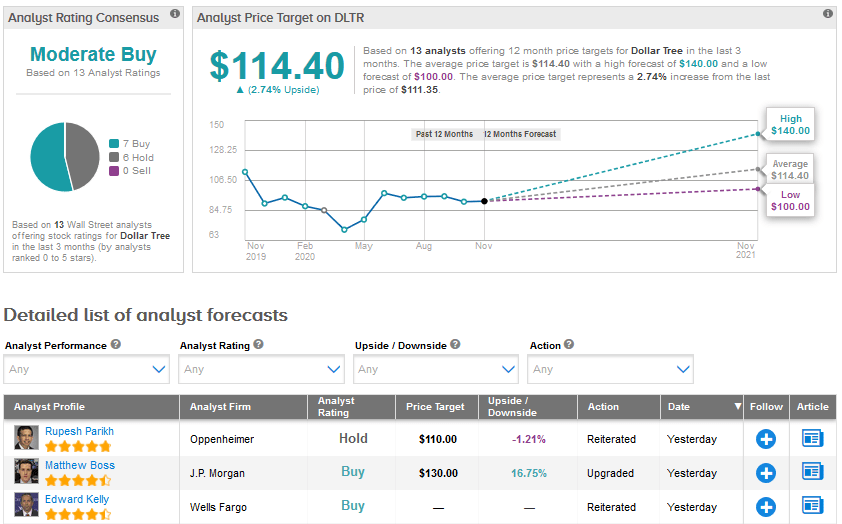

Meanwhile, 7 Buys and 6 Holds add up to a Moderate Buy analyst consensus for Dollar Tree. The average price target of $114.40 indicates a modest upside potential of 2.7% from current levels.

Like many of its peers, the company did not provide any outlook for the current quarter, citing continued volatility and uncertainty associated with the pandemic.

Following the results, J.P. Morgan analyst Matthew Boss upgraded Dollar Tree to Buy from Hold and upped the price target to $130 from $111. Over the next few years, the analyst sees Dollar Tree returning to a double-digit EPS “compounder,” with top- and bottom-line drivers in place at the core Dollar Tree banner and stabilization at the Family Dollar brand. With shares underperforming value and discount peers by about 40% so far, Boss sees a favorable risk-reward setup.

Related News:

McCormick Snaps Up Hot-Sauce Maker Cholula For $800M

Urban Outfitters Tops 3Q Estimates; Analysts Raise PT

Hormel Foods Hikes Dividend; Shares Sink On Dismal 4Q Results