The pandemic has disrupted normal life and has pushed people around the globe to work from home. With continued uncertainty related to the COVID-19 crisis, many companies, including Facebook and Google, have extended remote working mandates to mid next year. Amid the new normal, several tech companies are seeing robust demand for their products and services.

In fact, in June, Direxion launched its Direxion Work From Home ETF, which provides investors exposure to companies that enable work-from-home through their products and services in remote communications, cybersecurity, project and document management, and cloud technologies.

We will analyze how DocuSign and Slack Technologies have gained from the work-from-home trend and use the TipRanks Stock Comparison Tool to see which stock offers a more compelling investment opportunity.

DocuSign (DOCU)

DocuSign is a global leader in the e-signature space. As per Datanyze, the company has a 70.4% market share in the e-signature market, with its closest rivals SignNow, RightSignature and Adobe Sign having a much lower market share of 5.6%, 5.5%, and 5.3%, respectively. But, the company is now growing beyond its e-Signature product by automating the entire agreement process through the applications offered under its DocuSign Agreement Cloud.

The company added over 88,000 new customers in 2Q FY21 (ended Jul. 31) alone, bringing its total customer base to about 749,000. Strong sales led by the company’s e-signature solutions drove a 61% rise in billings to $405.7 million. Revenue surged 45% Y/Y to $342 million in 2Q FY21 with subscription revenue growing 47% to about $324 million. The impressive top-line growth helped in delivering adjusted EPS of $0.17 in 2Q FY21 compared to $0.01 in 2Q FY20.

For FY21, DocuSign expects revenue between $1.384 billion to $1.388 billion, which implies over 42% growth. (See DOCU stock analysis on TipRanks)

DocuSign continues to enhance customer experience through various collaborations. The company recently integrated its e-signature tools with Workplace from Facebook to provide customers faster and seamless access to its products.

The company is also making strategic acquisitions to accelerate its growth. In July, it acquired Liveoak Technologies, which has a secure agreement-collaboration platform that enables agreements to be completed remotely via video conferencing. DocuSign expects this acquisition to accelerate the launch of its DocuSign Notary solution for online notarization. DocuSign also acquired Seal Software, a contract analytics and artificial intelligence technology company.

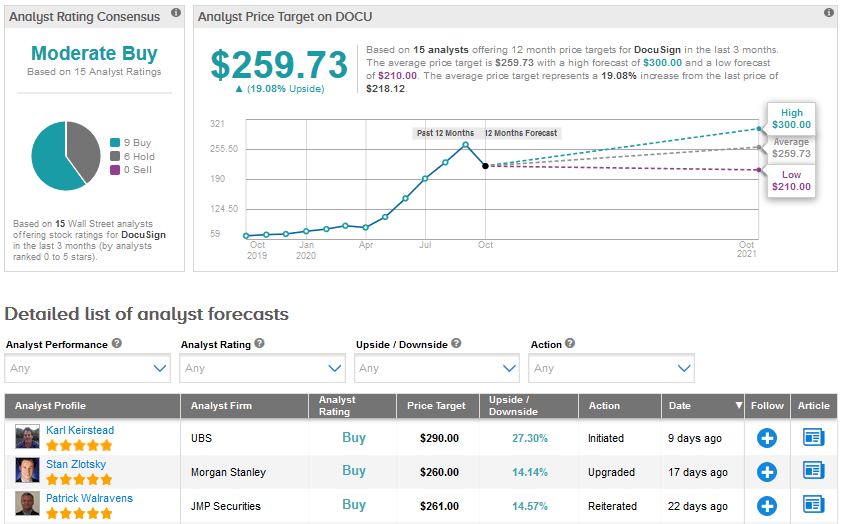

Last week, UBS analyst Karl Keirstead initiated coverage of DocuSign with a Buy rating and a price target of $290. The analyst stated, “While 60% billings growth may not be sustainable, the feedback from our checks about the durability of the move to no-touch contract execution was strong enough that we see upside to Street estimates in 2021.”

Keirstead also feels that the cross-selling opportunity from DocuSign’s Agreement Cloud suite looks under-appreciated.

The Street is cautiously optimistic about DocuSign and a Moderate Buy consensus is based on 9 Buys versus 6 Holds and no Sells. Shares have advanced a whopping 194% year-to-date and the $259.73 average analyst price target indicates that further upside potential of 19% lies ahead.

Slack Technologies (WORK)

Slack’s workplace collaboration platform has seen an increase in demand with remote working becoming a norm during the pandemic. As of the end of 2Q FY21 (ended Jul. 31), the company had 130,000 paid customers, reflecting a 30% Y/Y growth.

On Wednesday, Slack stock plunged 6.3% as Morgan Stanley analyst Keith Weiss downgraded Slack to Sell from Hold while maintaining a price target of $27 citing “a fading positioning versus an intensifying competitive landscape.” The analyst highlighted growing rivalry from Microsoft Teams, Zoom Video and Alphabet’s Google Workspace.

Weiss is increasingly concerned about the company’s ability to convert growing customer interest amid the current environment into stronger billings. (See WORK stock analysis on TipRanks)

There are concerns about a slowdown in Slack’s billings growth rate. Calculated billings were up 25% Y/Y in 2Q FY21 to $218 million, but decelerated compared to the 38% growth in 1Q. Slack blamed $4 million of COVID-related concessions and customers’ preference for shorter contract duration as the reasons for the slower billing growth. The company’s net dollar retention rate, another key metric, was 125% in 2Q compared to 132% in 1Q.

However, Slack’s 2Q revenue and earnings did exceed analysts’ predictions. But the stock fell after the results were announced as investors seemed to have even higher expectations with Zoom Video delivering a staggering 355% revenue growth in 2Q FY21.

Slack’s 2Q FY21 revenue rose 49% Y/Y to about $216 million and the company delivered break-even adjusted EPS compared to an adjusted loss per share of $0.14 in 2Q FY20. The company ended the quarter with 985 paid customers who generate over $100,000 in annual recurring revenue, reflecting a 37% growth. These customers accounted for about 49% of the overall 2Q revenue.

Moreover, customers contributing more than $1 million in annual recurring revenue increased 78% to 87. Also, Slack Connect, a feature enabling inter-company collaboration, experienced a 160% Y/Y growth in paid customers to over 52,000.

Slack is making efforts to attract more customers to its messaging platform and expand its offerings. The company is adding a new asynchronous video feature (which will allow people to collaborate on their own time) and also plans to bring in an audio option that will allow spontaneous interaction on its platform.

Coming to guidance, Slack expects revenue growth of 32% to 33% in 3Q and about 38% to 39% in FY21.

The Street has a Moderate Buy consensus for Slack based on 9 Buys, 6 Holds and 2 Sells. With shares advancing 28.4% so far this year, the average analyst price target of $31.86 indicates an upside potential of 10.4% over the coming months.

Conclusion

With its market leadership position in the e-signature space and a huge customer base, DocuSign is well-positioned to grow further, especially through additional features offered by its Agreement Cloud suite. Moreover, DocuSign stock has considerably outperformed Slack year-to-date and the average analyst price target reflects higher upside potential ahead. Right now, DocuSign looks to be a better work-from-home stock than Slack.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment