Cloudera flipped to a profit in the third quarter as sales beat the Street’s expectations and the enterprise data cloud company saw an increase in paying customers. Shares closed 7.2% higher on Dec. 4.

In the third quarter of fiscal 2021, Cloudera’s (CLDR) total revenue rose 10% to $217.9 million compared to the same period last year, and topped analysts’ expectations of of $209.1 million. Subscription sales in the three months ended October 31, jumped 18% to $197.4 million year-on-year, while Annualized Recurring Revenue (ARR) grew 12% during the same reported period.

Moreover, the company earned an adjusted 15 cents per share after posting a loss of 3 cents per share last year. Analysts had forecast a profit of 9 cents per share. In addition, Cloudera announced that its board has authorized the repurchase of an additional $500 million shares of its common stock.

“In the third quarter, we announced three new upcoming cloud-native services on CDP Public Cloud, and the number of CDP Public Cloud paying customers increased by more than 40%. We are beginning to see an acceleration of migrations by existing customers from legacy Cloudera and Hortonworks platforms to CDP,” said Cloudera CEO Rob Bearden. “We believe that Cloudera has never been better-positioned to capture more of the rapidly growing data management and analytics market opportunity for hybrid multi-cloud solutions.”

Looking ahead, Cloudera expects fourth-quarter adjusted earnings of between 10 cents to 12 cents per share on sales of $219 million to $222 million. Analysts had been looking for 10 cents a share on revenue of $216 million.

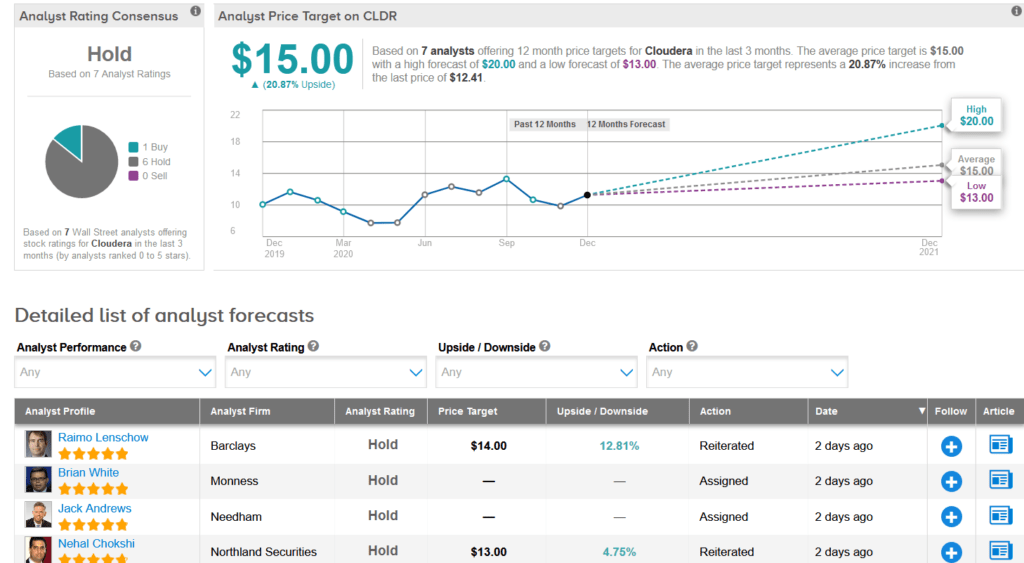

CLDR shares have gained 19% over the past month, taking their year-to-date advance to 6.7%. Meanwhile, Wall Street analysts are sidelined on the stock with a Hold consensus based on 6 Holds versus only 1 Buy. That’s with an average price target of $15, which suggests shares could appreciate another 21% over the coming year.

Commenting on the earnings results, Needham analyst Jack Andrews assigned a Hold a rating on the stock, as although he is encouraged by the adoption of the company’s CDP platform, he believes that sales are still unfolding.

“Although customers embracing CLDR’s hybrid enterprise cloud management vision are expected to expand their accounts over time, CLDR reiterated that it was premature to quantify expansion rates,” Andrews wrote in a note to investors. “While adoption trends of CDP appear favorable, we await greater proof points of product traction, clarity on expansion rates, and improved new logo wins in order to gain confidence that CLDR can participate in high-growth markets.” (See CLDR stock analysis on TipRanks)

Related News:

DocuSign 3Q Sales Soar 53%; Street Sees 12% Upside

Salesforce Crushes 3Q Estimates; Shares Slip 4.8%

Okta Jumps 9% As Cloud Demand Boosts Sales; Analyst Lifts PT