The COVID-19 pandemic made 2020 quite an eventful year for supermarkets and grocery chains. The likes of Walmart, Costco, Dollar General and Target adapted quickly to changing consumer behavior by offering several contactless delivery options. They also ramped up efforts to ensure adequate supply as Americans stockpiled groceries and essentials amid lockdown fears. What’s more, the retail space saw unprecedented e-commerce sales.

It would be unfair to expect top-line growth rates experienced during the lockdowns to repeat this year. That said, Wall Street experts see continued upside in certain retailers even as the pandemic tailwinds subside. Let’s stack up BJ’s Wholesale against Costco using the TipRanks Stock Comparison tool, and pick the stock that could offer better returns this year.

BJ’s Wholesale Club (BJ)

The demand triggered by the pandemic provided the kind of push BJ’s Wholesale needed after generating lackluster revenue growth of 1.4% in FY19 (ended Feb. 1, 2020). Stock-piling tendencies and shelter-at-home orders drove an 18.2% rise in the warehouse club’s revenue in the first nine months (ended Oct. 31) of FY20 and helped it gain market share.

Notably, BJ’s beat the Street’s expectations, with overall revenue growing 15.6% to $3.73 billion in 3Q. Net sales increased 15.7% to $3.65 billion and membership fee income rose 11% to $85 million. Excluding gasoline, comparable club sales grew 18.5%, with digitally enabled sales exploding 200%. What’s more, adjusted 3Q EPS jumped over 124% year-over-year to $0.92.

The improved business boosted cash flows and helped bring down BJ’s debt levels. Furthermore, the company is gaining new members at a strong rate. Its membership base at the end of 3Q reflected an increase of 630,000 members year-over-year on a net basis, which was way higher than the 200,000-250,000 membership additions experienced historically.

To ensure its growth beyond the pandemic, BJ’s is expanding in underpenetrated categories like fitness equipment, household goods, select consumer electronics categories and indoor furniture. It has also enhanced its food business with more healthy and organic options. (See BJ stock analysis on TipRanks)

Compared to giants like Costco and Walmart’s Sam Club, BJ’s has a smaller geographic presence. It operates 219 warehouse clubs and 149 BJ’s gas locations in 17 states in the Eastern US. With four club additions in FY20, the company intends to expand further.

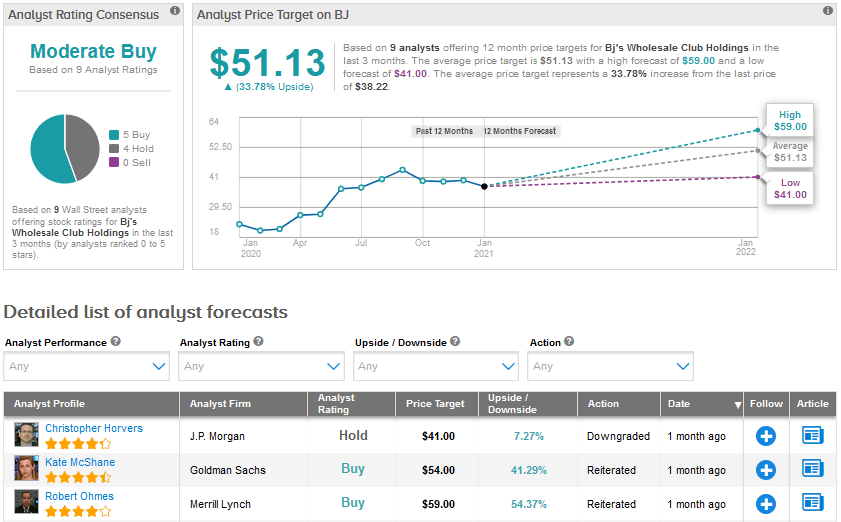

Following a discussion with senior management, Merrill Lynch analyst Robert Ohmes noted that BJ plans to open clubs in both new and existing markets and he expects the retailer to target new markets in Midwest cities with “disproportionate population growth (e.g. Columbus, Indianapolis, Nashville).”

The analyst feels that accelerated store openings will boost growth in both membership fee income and comps over the long-term, as new clubs scale over time.

In line with his optimism, Ohmes reiterated a Buy rating on BJ’s with a price target of $59 and concluded, “While difficult comparisons and a “return to normal” present risks to membership metrics in 2021, we expect increasing higher-tier penetration, improved merchandise offerings, and increased customer frequency / basket sizes to power renewal rates going forward. The membership base and business overall also both remain meaningfully stronger than they were in 2019.”

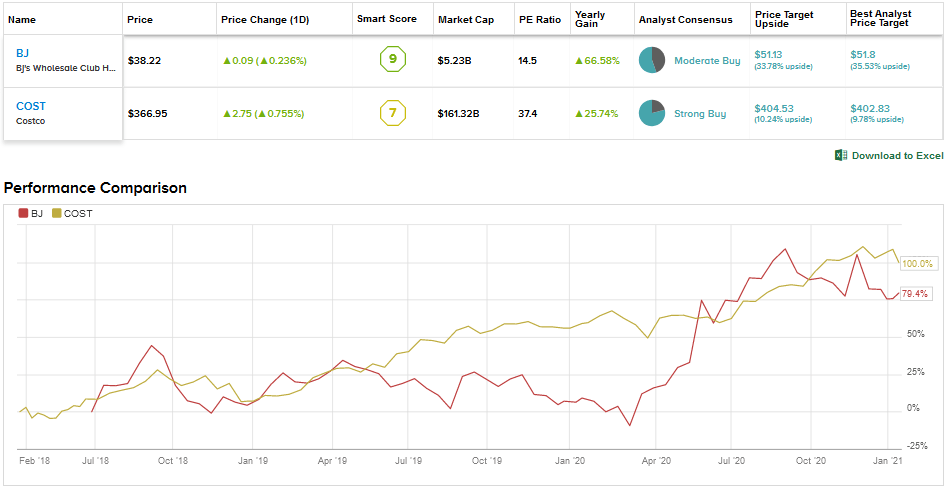

BJ’s scores the Street’s cautiously optimistic Moderate Buy analyst consensus based on 5 Buys and 4 Holds. The average price target stands at $51.13, implying 33.8% upside potential from current levels. Shares have risen by an impressive 67% over the past 52 weeks.

Costco Wholesale (COST)

Pandemic or no pandemic, Costco is considered to be one of the most consistent retail players. It operates 803 warehouses, including 558 in the US and Puerto Rico. From food and sundries to appliances and apparel, the warehouse chain offers a wide range of products at low prices to its members.

Costco’s revenue grew 16.7% to $43.2 billion in 1Q FY21 (ended Nov. 22) as the company continues to experience heightened sales amid the pandemic. Net sales grew about 17% to $42.3 billion, while membership fees increased 7% to $861 million. Comparable sales grew 15.4% in the quarter. Overall, robust revenue and operating margin expansion drove a 38% increase in EPS to $2.62.

Membership growth and retention rates are key metrics for Costco as membership fee has a material impact on its profitability. Renewal rates of 90.9% for US and Canada and 88.4% worldwide in the first quarter are a clear indication of the customer loyalty that the company enjoys. Costco ended 1Q FY21 with 59.1 million paid members, reflecting an 8% rise.

Last week, Costco reported growth of 12.3% and 10.7% in its December net sales and comparable sales, respectively. (See COST stock analysis on TipRanks)

Commenting on the December performance, Robert W. Baird analyst Peter Benedict notes that Costco delivered its 7th consecutive monthly double-digit core comps (excludes gasoline and foreign exchange impact) gain. That said, he pointed out that December core comps of 10.9% reflected a deceleration from November’s 14.6%, mainly due to softer traffic and less robust growth in food and sundries.

Despite the slowdown, Benedict remains optimistic about Costco’s loyal membership base and structural cost advantages. He reiterated a Buy rating on the stock with a $410 price target.

Looking ahead, Costco continues to enhance its e-commerce capabilities given the rapid sales increase since the pandemic (86.4% growth in 1Q FY21 alone). E-commerce sales accounted for just 6% of the FY20 topline. The acquisition of logistics provider Innovel Solutions last year will help in driving further online sales of “big and bulky” items like appliances and furniture.

Costco is also expanding its store footprint and added eight new (net) units in 1Q FY21, with it hoping to open up to 23 units in the full-year.

Shares have gained 22.4% over the past year and the average price target of $404.53 indicates upside potential of 10.2% in the 12 months ahead. The Street is bullish on the stock, with 15 Buys and 4 Holds adding up to a Strong Buy analyst consensus.

Conclusion

Costco’s proven track record over the past several years and its strong business model make it an attractive play for the long-term. That said, right now, the improvement in BJ’s Wholesale’s performance, the possibility of expanding its presence and the attractive upside potential in the stock make it a better retail pick.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment